- 4Q25 results were broadly constructive, with engine OEMs highlighting strong aftermarket activity driven by higher shop visits, robust spare-parts demand, and installed-base growth, leading the majors to guide 2026 earnings above consensus expectations

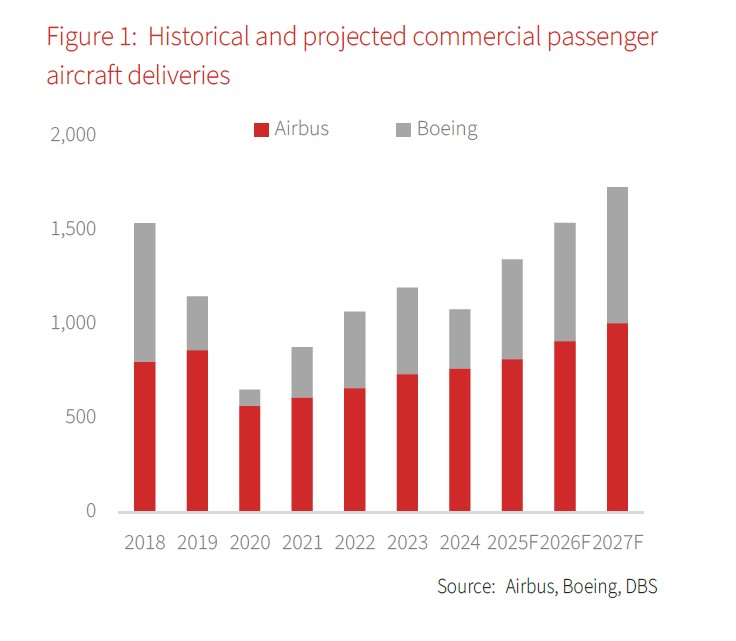

- Aircraft OEM updates were more mixed, as Airbus guided to around 870 deliveries in 2026, below expectations due to ongoing P&W GTF shortages, while Boeing pointed to a material uplift in deliveries as production stabilises

- Middle East conflict has limited spillover to commercial aerospace, with the sector’s core drivers largely intact. Aircraft utilisation may dip temporarily due to airspace closures and rerouting, but higher fuel prices should drive fleet renewal. Meanwhile, aftermarket remains supported by a large installed base and shop visits booked well in advance

- We remain constructive on the sector but see more favourable risk-reward in aircraft OEMs, where delivery ramp-ups and operating leverage to production normalisation offer greater upside relative to engine makers trading at stretched valuations

Related insights

Commercial aerospace offers relative calm in the storm amid the Middle East conflict, as the disruption is hitting airline economics far more directly than the sector’s underlying demand drivers. Airspace closures and rerouting are raising flight times and fuel costs, which should weigh on airlines and cause a temporary dip in aircraft utilisation in 2Q26. For commercial aerospace, however, the read-across is more manageable: while some fear that disruption at airlines could lead to aircraft deferrals, higher fuel prices strengthen the case for fleet renewal and increase the incentive to take delivery of newer, more fuel-efficient aircraft. The aftermarket should also remain resilient, supported by a large installed base and shop visits booked well in advance, while the Middle East is not a critical supply-chain node in the way Russia was. Taken together, the conflict is more of a near-term earnings headwind for airlines than a thesis-changing shock for commercial aerospace, unless the disruption becomes prolonged.

Recent 4Q25 results reinforced the widening performance gap between engine OEMs and airframe manufacturers, with aftermarket demand continuing to drive earnings momentum across the sector. GE Aerospace, RTX, and Rolls-Royce all highlighted strong services activity, supported by higher shop visits, robust spare-parts demand and continued installed-base growth, leading all three to guide 2026 earnings above consensus expectations, with Rolls-Royce also announcing an outsized GBP7-9bn multi-year share buyback programme. Airbus reported a solid 4Q25 result, but its 2026 delivery guidance of around 870 aircraft came in below expectations as ongoing P&W GTF engine shortages continue to constrain the production ramp. Boeing’s update was more constructive, with management guiding for a material uplift in aircraft deliveries as 737 and 787 production stabilise. Overall, 4Q25 reinforced the same sector dynamic: engine OEMs continue to benefit from strong aftermarket growth, while airframe OEMs remain more exposed to engine shortages and production execution risk.

Remain constructive on the sector given limited spillover from the Middle East conflict; risk-reward for aircraft OEMs are more favourable versus engine makers. Aftermarket demand should stay steady despite near-term travel demand fluctuations, but we believe there could be some downside risk if airlines accelerate retirements of older aircraft. Much of this strength already appears reflected in valuations, as the key engine OEMs are trading at stretched multiples in the 30s to 40s on a P/E basis. In contrast, aircraft OEMs still trade at attractive valuations given lingering execution and supply-chain concerns. Given their high operating leverage to production normalisation, mix and pricing, we see greater upside if delivery bottlenecks ease and confidence in rate ramp-ups improves.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.