Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

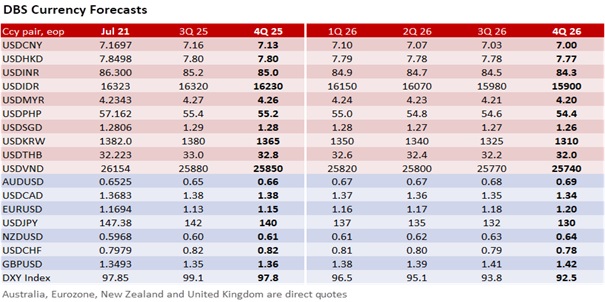

The DXY Index depreciated by 0.6% to 97.85 overnight. US Treasury Secretary Scott Bessent urged a “comprehensive institutional review” of the Federal Reserve, casting doubt on the Fed’s credibility and intensifying market expectations for interest rate cuts. The US Treasury 30Y yield fell for a fourth session by 4.4 bps to 4.944% while gold prices rose 1.4% – its largest jump in six weeks – on haven demand. Viewed against his earlier push for the Treasury Department to play a greater role in banking regulation, Bessent is seen aligning Fed policy to US President Donald Trump’s fiscal and tariff agenda to advance the MAGA platform. If so, markets will find it more difficult to shake off concerns over the Fed’s independence, given what appears to be a unified strategy to bring monetary and financial governance under stronger executive oversight.

However, pushing for another steep decline in the DXY faces headwinds from Japan’s post-election uncertainty and anxiety over US-EU trade negotiations.

The JPY’s post-election rebound of 1% on Monday was seen as profit-taking on a widely anticipated outcome – the Ishiba government’s loss of its Upper House majority, which had already been priced in. While Prime Minister Shigeru Ishiba’s pledge to remain in office offered temporary reassurance about stability ahead of critical trade talks with the US, it does not ease worries about internal pressure within the Liberal Democratic Party to eventually replace a leader who has lost the majority in both houses of parliament. While the 10Y JGB yield has backed down from 1.60%, the market remains wary of more fiscal measures to address the opposition-led public discontent over inflation.

The EUR’s 0.6% appreciation to almost 1.17 was largely driven by broad USD weakness, triggered by Bessent’s call for a Fed review. However, the Trump administration has also been vigilant against a further rapid decline in the USD, which would undermine credibility and investor confidence in US financial markets. Some European Central Bank officials have also warned that further euro strength beyond 1.20 could suppress inflation below the 2% target and pressure exports. US-EU trade talks are at a critical juncture ahead of the August 1 tariff deadline. While both sides have emphasized the preference for a diplomatic resolution, the high stakes and aggressive posturing also mean that failure to find common ground could trigger a real tariff war, which would elevate economic risks and market disruptions.

Quote of the Day

”However difficult life may seem, there is always something you can do and succeed at”

Stephen Hawking

July 22 in history

Sarawak achieved independence from British colonial rule in 1963.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025