- Recent high-profile episodes of bankruptcies and restructuring are masked by an otherwise sanguine credit spread environment in HY bonds.

- With spreads at all-time tights, and risks on the horizon, the years of HY outperformance may be reaching its limits.

- Rising maturity walls and liability management exercises could be catalysts for a tightening of liquidity down the road.

- Investors should maintain an up-in-quality stance in both public and private credit. We continue to favour A/BBB credit in the public markets, with preference for government+ securities (agency MBS, TIPS) over nominal treasuries.

- We see benefits in including diversified strategies in private markets such as distressed debt or opportunistic credit strategies that have the toolkit to capitalise on dislocations.

Related insights

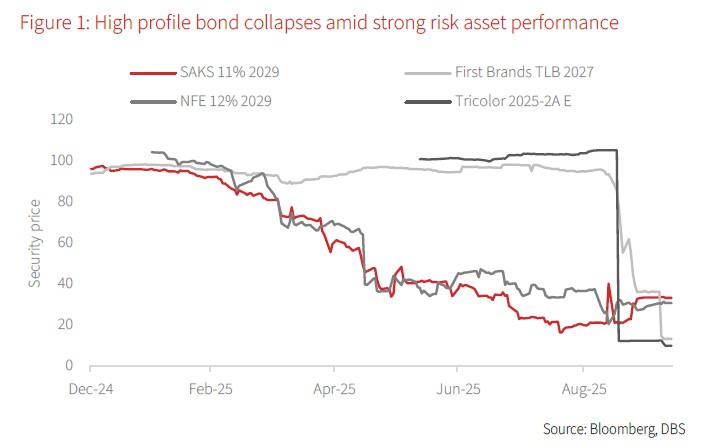

It was not easy to lose money in 2025. If one merely studied aggregates, the post-April “Liberation Day” market performances across a broad swathe of risk assets would suggest that there was nothing amiss under the hood. One could literally have bought anything from commercial paper to cryptocurrency and felt like they acquired Buffett-like investment acumen in 2025. Yet in the realm of credit, a recent spate of high-profile collapses has jolted an otherwise sanguine High Yield market with fresh doubt. It began in early 2025 with Saks Global – a luxury retailer – restructuring bonds after just a single interest payment on their SAGLEN 11% 2029 issue. Days later, natural-gas company New Fortress Energy followed suit. More recently, subprime auto lender Tricolor Holdings filed suddenly for bankruptcy, followed by the collapse of an auto-parts supplier, First Brands Group. The prices of their debt instruments have been wiped to cents on the dollar.

Spreads do not tell the whole story. The recent signs of stress run in sharp contrast to what aggregate HY spreads are telling us – with various markets at their 0th percentile in the last 10 years – implying that they have not been more expensive than current levels in the last decade. While we believe spreads in general have reason to stay tight given the supportive environment of stable growth and lower policy rates, we think that risk-reward imbalances are now much more pronounced for HY investors given the mix of emerging stress and tight valuations; that 6% yield may not seem so enticing when faced with the prospect of a 60% capital loss in an unexpected credit event.

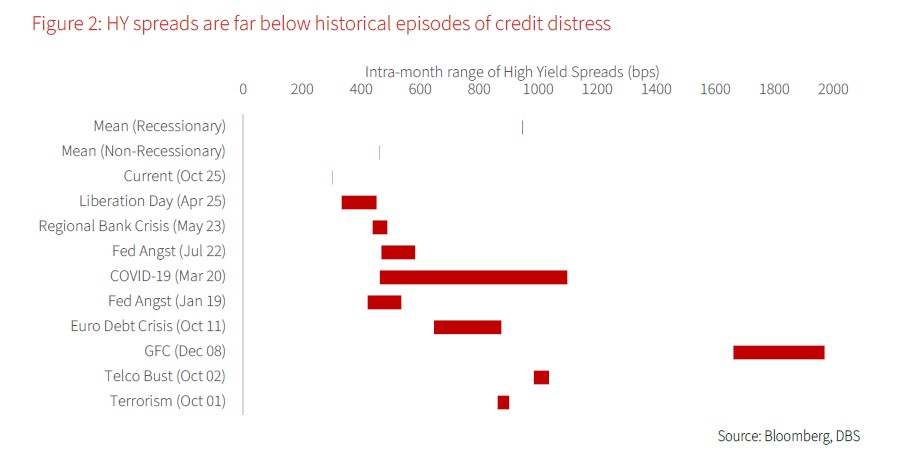

HY priced to perfection. To illustrate how tight HY spreads currently are, we juxtaposed current spreads against their intra-month ranges over historical episodes of distress. Present levels of c.304 bp remain far outside the levels observed during market strain, far below even the norms under non-recessionary conditions. This implies that HY credit is already priced for perfection, with risk of underperformance should we enter another period of uncertainty; plenty of opportunity for that under an era of seemingly erratic policymaking.

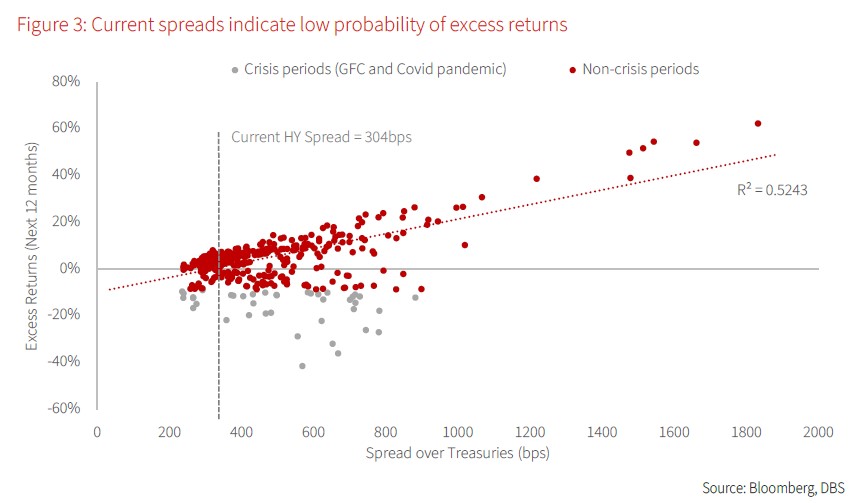

Foreboding forecasts. The historical regression of current spreads against 12M forward excess returns also paints a daunting picture. Stripping out crisis-era distortions, current spread levels would potentially produce no excess returns in the coming one-year period – meaning that investors would likely see little difference between investing in HY credit and risk-free treasuries on average. If taking on more risk is not commensurate with more returns, why should we?

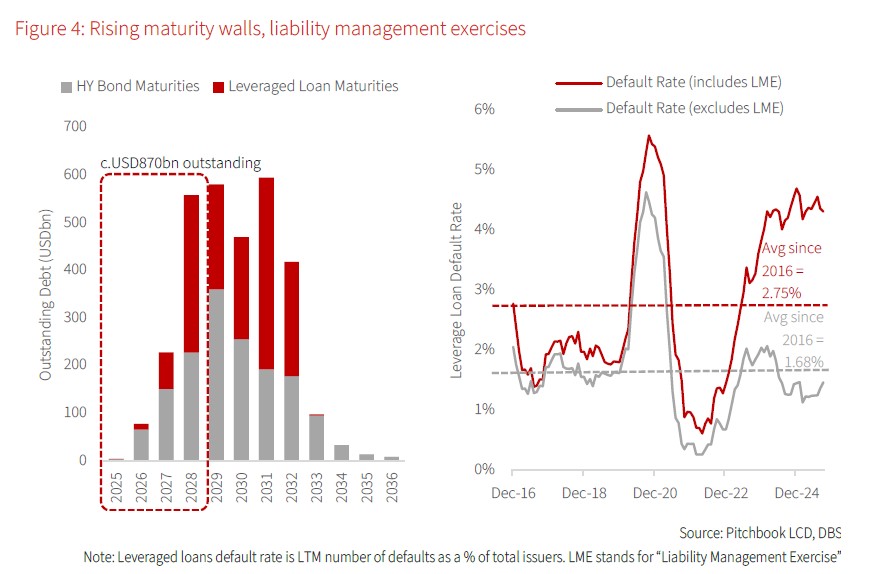

Clouds on the horizon. Unfortunately for risky credit, the above tight spreads seem to be ignoring certain realities, that (a) there is a coming maturity wall requiring c.USD870bn in refinancing over the next three years, and that (b) although absolute levels of leverage loan defaults remain low, if one includes Liability Management Exercises (e.g. distressed exchanges) in the mix, such delinquencies reveal a higher level of distressed activity under the hood. This presents a somewhat circular disequilibrium: Investors buy risky credit because of low default rates → Larger positions at risk of loss under credit distress → Investors more willing to tolerate LME to prevent outright defaults → Default rates remain low → Investors buy more risky credit. One can see that it would only take a tightening of liquidity in the market to put an immediate halt to this flow, possibly taking it in reverse.

Quality matters. For credit investors, one must feel like caution has not been rewarded in a good three-year period where HY, leveraged loans and middle market lending has outperformed more conservative strategies like Investment Grade bonds. However, now is not the time to throw in the towel with excessive risk-taking to catch up. We propose the following:

- For public credit, we continue to favour an up in quality stance with IG credit in the A/BBB bucket. We like “government+” allocations like agency MBS (for additional spread premium) and TIPS (for inflation protection) over nominal treasuries. Such high-quality allocations will provide downside protection should the markets unexpectedly turn risk-off.

- For private credit, we turn more neutral on direct lending strategies, preferring to add when spread valuations offer better premiums. Investors should remain with the best-in-class managers who have financial flexibility to navigate more opaque lending strategies. We see benefits in including diversified strategies such as distressed debt or opportunistic credit strategies that have the toolkit to capitalise on dislocations in the markets.

No reason to panic. We wish to reiterate that it is not our base case expectation for widespread insolvencies at this juncture. Rather, investors could take this opportunity to improve the quality of their credit portfolio while spreads are still painting a sanguine picture, knowing the penchant of credit markets to freeze up suddenly when one most needs liquidity. When credit quality starts to matter, it is often a matter of being too late to start.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.