- “America First” regardless of which candidate takes the helm

- Duration fear is likely to be more acute if Trump gets re-elected

- Trade restrictions to rise; reordering of supply chains will be needed

- We discuss credit themes that could resonate in this environment

Related insights

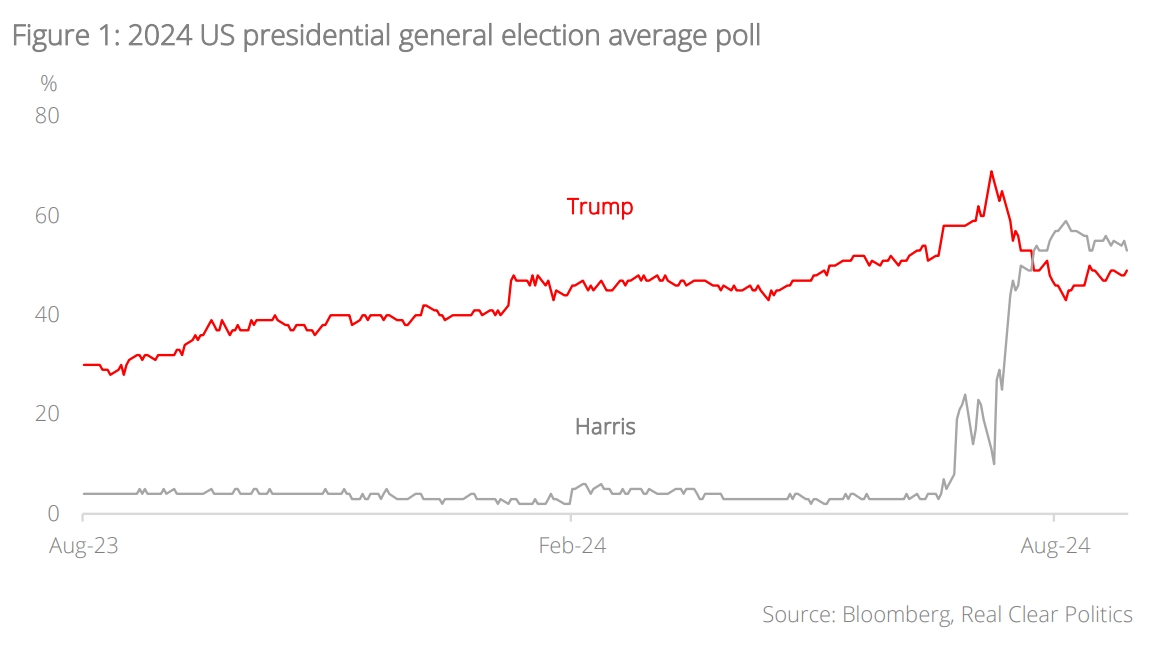

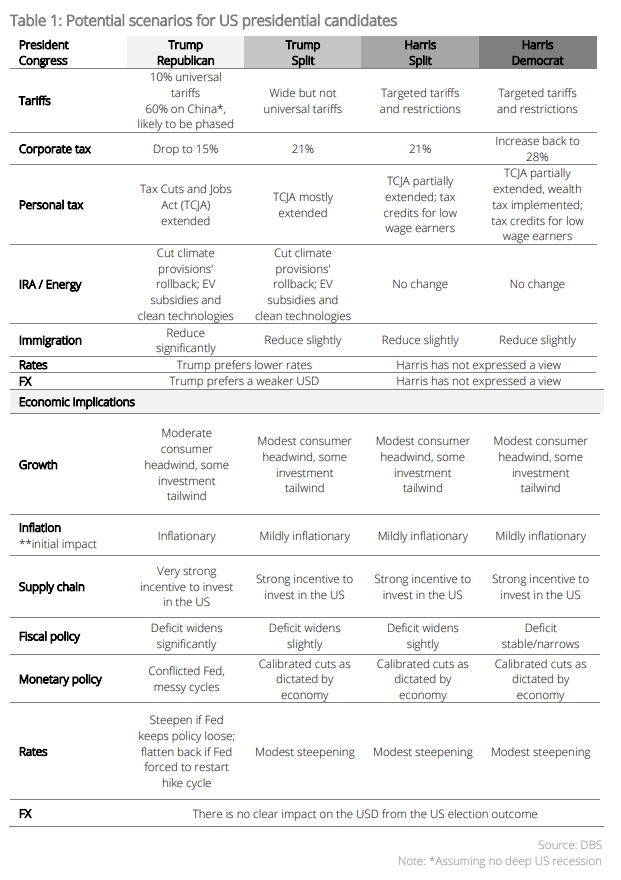

The upcoming US elections on 5 Nov will be closely scrutinised for key trends that could define the next four years. While the Trump campaign is associated with broader and higher tariffs, wider fiscal deficit, and duration risks, the Harris campaign represents an extension of what we have seen under the Biden administration. Notably, the Biden administration has not shied away from using tariffs and is planning substantial increases across selected Chinese imports over the coming few quarters. Therefore, Harris is likely to stay the course with more targeted restrictions on trade.

Regardless of which candidate takes the helm, the environment is likely to be challenging for the rest of the world. “America First” would probably be the essence even if the policies taken differ. Offhand, there are several lenses to view areas where the US could clamp down on. These include firms that sell a lot to the US, firms that produce in China, and lastly, China-linked entities. This does not even account for the second or third order impact as other economies/entities react. Substantial reordering of supply chains may be needed.

All these should be viewed in context of a cooling US economy and likely calibrated Fed cuts ahead. From a portfolio perspective, with rate cuts likely, we continue to favour a duration barbell that overweighs investment grade (IG) credit in the short end (1-3Y) and longer end (7-10Y). Asia corporates in general can stand to benefit from short supply, strong ownership, and decent 1H24 results. This is evident from Asia spreads tightening to within the spreads of the US and Europe. However, for ultra-long tenors (>10Y), we are wary of a rise in term premium as investors require more compensation for inflation and issuance worries.

Against this backdrop, we highlight our top themes for Asia credit.

Mulling “America First“

Sidestepping the worst of the fallout in the lead-up to the US elections on 5 Nov may be the most practical way to approach markets as political rhetoric heats up. At the point of writing, odds for both Trump and Harris are even. While focus is on what Trump might do if re-elected, we should note that bi-partisan support from the Democrats remains firm towards China. Policies taken by either a Republican or Democrat President may differ, but the essence (of protecting America) might very well be similar. First and foremost, the “America First” agenda would undoubtedly include even more intervention into domestic financial markets which is credit positive for US companies. Below, we discuss some nuances from an Asian perspective, considering duration and credit risks.

Duration a larger headwind under Trump. The Congressional Budget Office projects the US on a fiscal deficit path of 5-6% of the GDP for an extended period, assuming moderate economic growth. As plans to reduce foreign military and healthcare spending might not be easily achieved, concerns over US’s fiscal position are unlikely to be easily dispelled even if Harris takes helm. Moreover, under Trump, odds of further tax cuts and extension of existing Trump era tax cuts (expires end-2025) would be much higher. Curve steepening over concerns on longer-term issuances has become the de-facto Trump trade. That said, impact would be more muted vs late 2016 when rates were low (more scope for increases).

However, the longer-term shift is not clear as we consider second and third order impacts. It depends on structural fiscal issues and sentiment, how tariffs/restrictions are implemented, as well as how growth/inflation gets impacted. We suspect the market will focus on different concerns at different points in time. Calling the sequence of shifts is difficult but we lean towards steepening, putting greater weight on Fed easing amid lingering fiscal concerns.

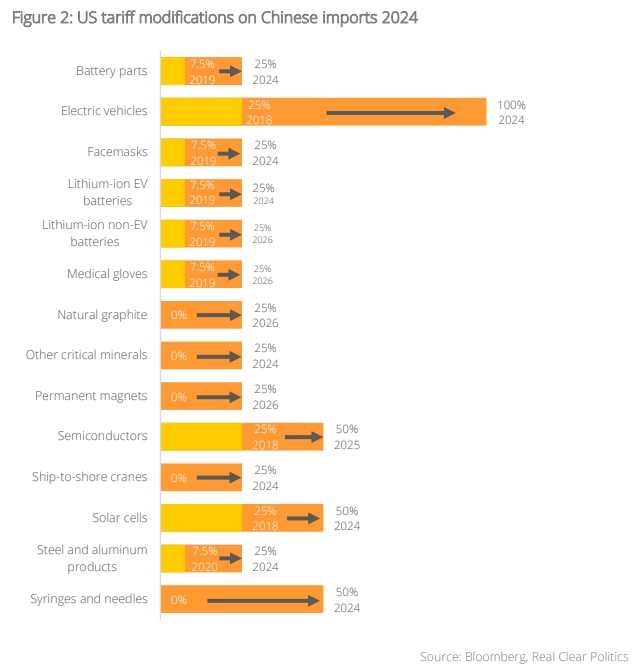

Other factors impacting Asia credit can be distilled into two factors – the level of protectionism (i.e. tariffs) and national security restrictions. Trump prefers tariffs (evident from his first term) while Democrats (under Biden) favours restrictions. Both strategies are punitive. Trump’s potential 10% tariff on all US imports is arguably the mildest measure with some effects defrayed across the FX space. A more targeted tariff of 60% on China could stall imports from the Chinese as trade becomes unfeasible, bringing about trade diversion much like the first round of Trump trade wars.

The final step would be to police the import of Chinese goods – via rules of origin and measured by value-add, even if rerouted – by restricting imports of products from several economies altogether. This would be a gamechanger as rerouting would no longer be viable, unlike the workaround in 2019. Among the most impacted are firms that sell a lot to the US, those with production in China, and China-linked entities. We note that the Biden administration has not shied away from tariffs. Regardless of who takes helm, the end effect would be to encourage businesses to invest in the US and to sell to the US.

Restrictions on firms selling (currently mulled by the Biden administration) can be punitive. Imposing a Foreign Direct Product Rule (FDPR) allows the US to restrict sale of goods containing American technology. When applied on chips and chipmaking, it would have substantial implications on firms with significant sales to China. In practice, this should only hit the tech sectors which are arguably the most sensitive for national security.

Lastly, we consider second order impact as these restrictions come into play. Would Chinese companies need to pivot to other markets if sales to US is not feasible? This may impact economies and firms with similar manufacturing capabilities as China. Retaliatory measures and tariffs should also be considered though large economies will probably have more clout and success in defending their own industries, if required. From the US’s perspective, these restrictions will inevitably translate into higher prices for selected goods. Considerations include how far the tariffs go (i.e. whether they cover a wide swarth of goods), the capacity of US firms to pick up the slack, and whether US consumers can tolerate higher prices. Regardless, manufacturing supply chains look set to be reordered with significant pains as the process runs through.

In this environment, the logical beneficiaries would likely be US-based firms. Accordingly, risk appetite, especially outside of the US, is likely dicey as hawkish rhetoric persists in the US elections. Considerations on assets would probably take a broad framework on where vulnerabilities lie and more importantly, where to hide.

Credit Considerations

Against a backdrop of (i) lower supply of USD/ SGD issuances from Asian corporates, (ii) flight to safety, and (iii) tailwind of likely interest rate cuts, we consider potential themes and sectors that could be affected below. The only long-tail event is that of a rate hike.

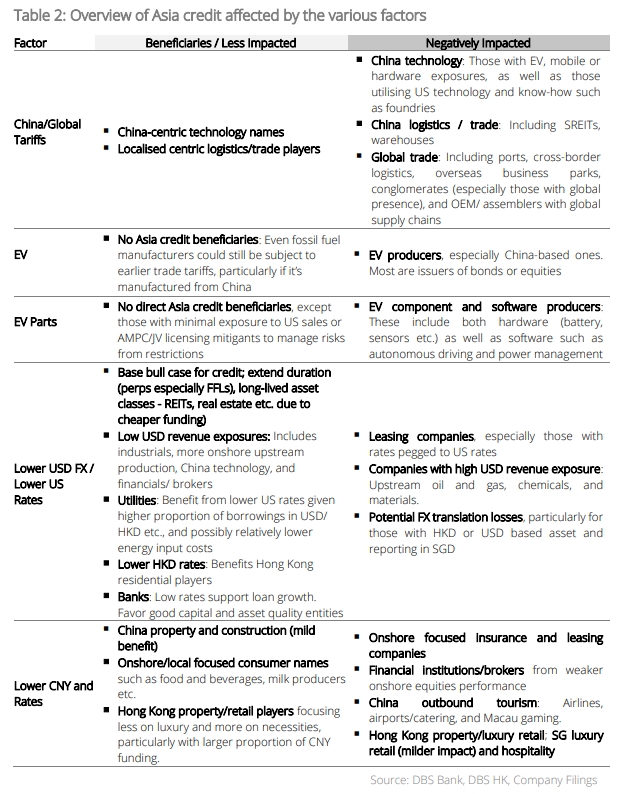

A. China and global tariffs/trade restrictions the key issue

A dominantly negative impact is most likely to occur regardless of which candidate gets elected. However, companies with less global presence and involvement with sensitive technology such as semiconductor, military, and defence (especially US-owned tech) are less affected. Conversely, those with a more global presence and significant sales to the US are at risk, particularly hardware/OEM suppliers, given lower margins and likely production in China. Asia technology companies, especially those that are China-centric, would be less affected.

Tariffs on net basis lower global trade volumes, especially for the US-China leg. However, universal tariffs could depress other trade links compounded by pullout from trade partnerships with other nations.

B. EV and EV components industries

Under the US Inflation Reduction Act (IRA) passed during the Biden administration, consumers can claim USD7,500 tax credits for EV purchases. Trump and Vance were vocal about abolishing such tax credits and incentivising US-made fossil-fuel vehicles. A reduction or repeal could cut demand. US EV sales already slowed to +21% y/y as of 22 Apr 2024 (vs FY23: 40%; FY22: 67%) due to the higher cost of auto loans and demand fatigue.

A reduction of IRA benefits (EVs) and/or higher tariffs to batteries made outside of US more likely than IRA repeal.

Under IRA, some EV battery manufacturers benefit through the Advanced Manufacturing Production Credit (AMPC). Under this scheme, entities can claim tax credits for battery modules produced in the US. On the other hand, an IRA repeal must cross both chambers of Congress to pass which is a significantly higher hurdle. Moreover, a repeal would contradict the aim of raising US-based production, particularly for Trump’s agenda.

There could be other noises such as being added into the entity list for “forced labour” by Republican lawmakers, as with a recent case for a leading China-based battery manufacturer. Overall, impact depends on the proportion of US sales which in this case is <10% of revenue. We note that there are ways to get around this; in this case, the company operates joint battery production facilities with US carmakers through tech licensing deals where the US entity pays capex, while the Chinese co-receive royalties for LFP tech. This company is also in talks with GM and Tesla for further of such deals.

C. Lower US interest rates and USD FX

Lower rates provide a positive uplift for asset classes, especially those with longer duration like fixed income and perpetuals. That said, it could be negative for rates-dependent or US FX revenues like leasing companies, banks, upstream oil, and resources. A translation into lower HKD rates could support Hong Kong residential players with lighter mortgage burdens, a reversal of value depreciation, and negative equity situations. This tailwind is predicated on the economy slowing down and less so on the US elections outcome which could have further implications on how rates could evolve.

D. Weaker CNY against USD, SGD

The CNY may face depreciatory pressures in a period where the PBoC needs to keep rates low to support the economy, especially if more trade restrictions get implemented. This is despite not much action during July’s Politburo meetings and the Third Plenum meeting. Accordingly, consumer demand by onshore Chinese would be dampened. It would affect tourism/spending outside of China and gaming revenues. First order impact would be to luxury retail landlords in Hong Kong and to Singapore’s retail REITs, albeit to a lesser extent. Necessities consumption would be far less impacted.

E. Increased US oil and gas production, mostly noise

Oil production hit a record high of 13mn bblpd during Biden’s tenure. Any surge in production from current levels would be pyrrhic, crashing average selling prices. A more feasible option for upcoming candidates is to ease oil leases and drill permits, meaning any further increase in production is likely limited. Moreover, oil price crashes in 2020 and 2021 have not lowered prices with lasting effects until now. This is partly also due to shut supply chains back then. Overall, lower oil prices benefit power generation and utilities but negatively impact upstream players.

F. Financials, a mixed bag

Low rates support loans growth which has been lacklustre, except for Indonesia (FY23: +12% y/y). With a focus on capitalisation and asset quality amid the flight to quality, we favour South-East Asian banks that are better capitalised with good asset quality. Firstly, on asset quality, banks have been ramping up provisions to build reserves, and credit costs could see room to decrease with lower rates, easing the strain on borrowers. Secondly, South-East Asian banks are better capitalised vs regional and global peers, providing more buffers in times of potential stresses. On average, South-East Asian banks’ Tier 1 capital ratio are Thai banks (16.4%), Indonesian banks (26.1%), and Filipino banks (15.3%). This compares to Hong Kong/China’s 13.9% (H-shares) and North America’s 11.7%, as of end-2023.

G. “America First” positive to US companies and beyond?

The US government’s intervention likely extends to domestic financial markets which is credit positive to US companies and possibly foreign companies or regions that are part of its supply chain.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.