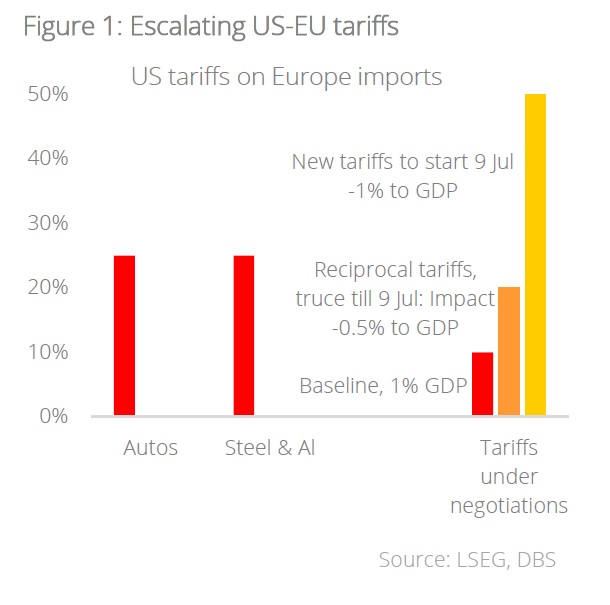

- Pending negotiations, the US may impose 50% tariff on select European imports, thus escalating trade tensions

- Germany is the most exposed EU country, with significant exports to the US

- A EUR1tn fiscal stimulus will help Germany counter tariff impacts

- European equities are undervalued, with room for investor inflows

- Overweight Europe: Defensive sectors, attractive dividends, and favourable currency outlook provide resilience

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

What happened

Pending negotiations, there is the risk of US imposing 50% tariff on imports from Europe beginning 9 Jul. This shift in trade policy marks a notable escalation in tensions across the Atlantic and is anticipated to have significant economic consequences for the Eurozone. The EU has offered EUR50bn in a trade deal which includes LNG purchases and soybeans, and is also proposing low/0% tariffs on cars/industrial goods. At this point it is unclear what the US government is seeking for a successful outcome, though the rhetoric is harsher than that towards China.

What it means

- Prior to this policy change, the Eurozone's growth was projected at 1%. With these new tariffs however, Eurozone GDP is expected to decline against the baseline by roughly 60 bps, leading to stagnant growth and increased risks of further downturns. The combination of a global surplus of supply and domestic repercussions stemming from growth weaknesses and potential retaliatory measures will likely keep inflationary trends subdued.

- Germany, which constitutes the largest share of EU exports to the US, is particularly vulnerable to the tariff increase. With the US as Germany's most significant export market (c.10% of its total exports), key sectors affected include: i) Automobiles, with 23% of German car exports destined for the US; ii) Pharmaceuticals and medical products; and iii) Machinery and electrical equipment.

- Furthermore, Germany's ambitious fiscal stimulus plan – projecting EUR1tn for infrastructure and defense over a span of 12 years – serves as a critical counterbalance to the impending external trade shock. The potential effectiveness of this domestic policy response illustrates how fiscal tools can be employed to mitigate external challenges and uphold macroeconomic stability.

How to invest

Maintain Overweight Europe: Planning for Resilience Amid Uncertainty

- While the macroeconomic outlook for the Eurozone remains fraught with uncertainty, Europe’s defensive sector positioning, enticing valuations, and Germany’s robust fiscal support reinforce our confidence in the region. These elements collectively offer a buffer against global market fluctuations and establish Europe as a safe haven within the current investment climate.

- Furthermore, we maintain overweight in Europe, underpinned by a combination of attractive relative valuations, supportive policy dynamics, and sector composition that offers resilience amid macroeconomic uncertainty. We continue to favour high dividend-yielding equities within defensive sectors such as consumer staples, utilities, and industrials, which are well-positioned to weather near-term volatility. While structural cyclical sectors like healthcare and IT may face short-term headwinds from the evolving trade environment, they remain core to our medium- to long-term strategy, supported by enduring themes such as digital transformation and demographic shifts linked to an ageing population.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025