- US: Trump’s sweeping tariffs (125% on China, 145% on US) are shaking global trade and investor confidence with the IMF cutting US GDP growth forecasts and raising recession risk to 37%

- Japan: BOJ downgraded its GDP and inflation forecasts and delayed its target for 2% inflation to FY2027, signalling a slower pace of rate hikes

- South Korea: South Korea’s GDP growth forecast was cut sharply after a weak first quarter and the impact of US tariffs with the central bank expected to cut rates further while the government plans a fiscal stimulus

- Thailand: BOT cuts its policy rate to 1.75%—the lowest in two years—and is expected to ease further due to the risks from escalating US-led global tariffs

Related insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025

US: Pushing limits. US President Donald Trump’s “Make America Great Again” or MAGA agenda, especially his tariff proposals on Liberation Day (2 Apr), have shaken investor confidence in the foundational pillars—US economic strength, institutional trust, and geopolitical influence—that upheld the USD’s pre-eminence as the world’s dominant currency after World War II.

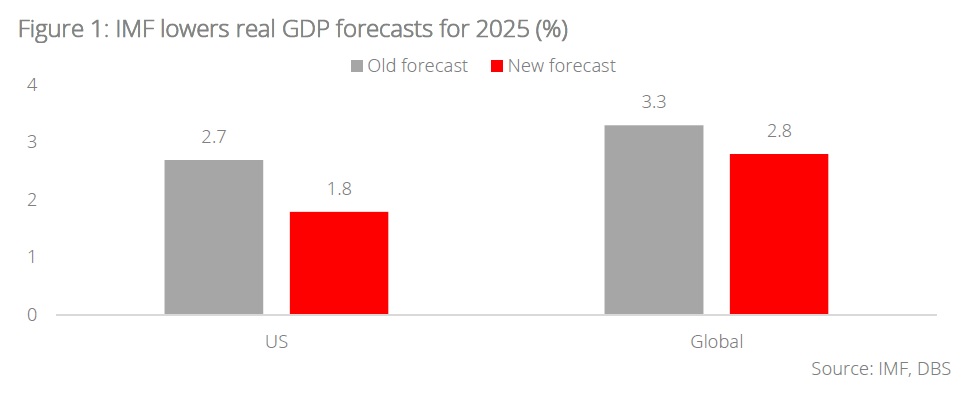

The first risk is a less exceptional and less stable US economy. The IMF expects Trump’s tariffs to lower US GDP growth to 1.8% in 2025 from 2.8% in 2024, adding that US recession risks have increased to 37% from 25%. The sweeping tariffs have disrupted established trade patterns which major US retailers warn could empty supermarket shelves. Grappling with heightened uncertainty, US businesses will likely delay investment and hiring decisions. US consumers face higher prices, increased job uncertainty, and acute market volatility that directly impact their retirement accounts, such as 401(k)s and IRAs, which are heavily invested in equities.

The high tariffs that the US and China—the world’s two largest economies—imposed on each other (145% on China and 125% on the US) have been likened to a trade embargo that threatens global trade and the world economy. The IMF now sees global growth lower at 2.8% in 2025 vs its previous 3.3% forecast in January, below the historical average of 3.7% from 2000-2019.

The second risk is financial market stability. Trump’s protectionism and unpredictable policy decisions have started to erode the confidence in the US as a prime destination for foreign investment which was painstakingly renewed after the Global Financial Crisis. Trump risks transforming the US from the investment magnet he seeks into a risk international investors may hesitate to take. Furthermore, his approach (i.e. to fix global imbalances through tariffs and pressure so that countries buy more US goods, thereby converting them from USD earners into USD spenders) risks undermining the recycling system that financed America’s deficits. Surging gold prices to lifetime highs reflect the disincentive for countries to add more to their US holdings. The 26.5% rise in gold prices this year looks poised to overtake the 27.2% increase for all of 2024.

The third risk is institutional trust. Since taking office, Trump’s actions saw the US steering towards a new international order. The world is questioning America’s political leadership (which established the post-war global order based on rules, free trade, open markets, and collective security that was grounded in trustworthiness). They raise hard questions for foreign governments that rely on the USD to anchor foreign reserves, global institutions that hold Treasuries as risk-free benchmarks, and private investors who anchor portfolios around US assets and trust the USD as a haven in volatile times.

Overall, the Trump administration is trying to achieve too much too fast, and markets are taking notice. Each initiative carries risks which collectively amplify market concerns about high tariffs and trade negotiations, rising inflation and job insecurity, the Fed’s independence, fiscal discipline, financial sector stability, and the USD’s status.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025

Related insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025