- Recent pullback in Korea equities appears to be driven by profit-taking and temporary risk aversion instead of weakening fundamentals

- Higher oil prices are a near-term headwind, but policy support and a “look-through” stance from the Bank of Korea should help limit growth damage

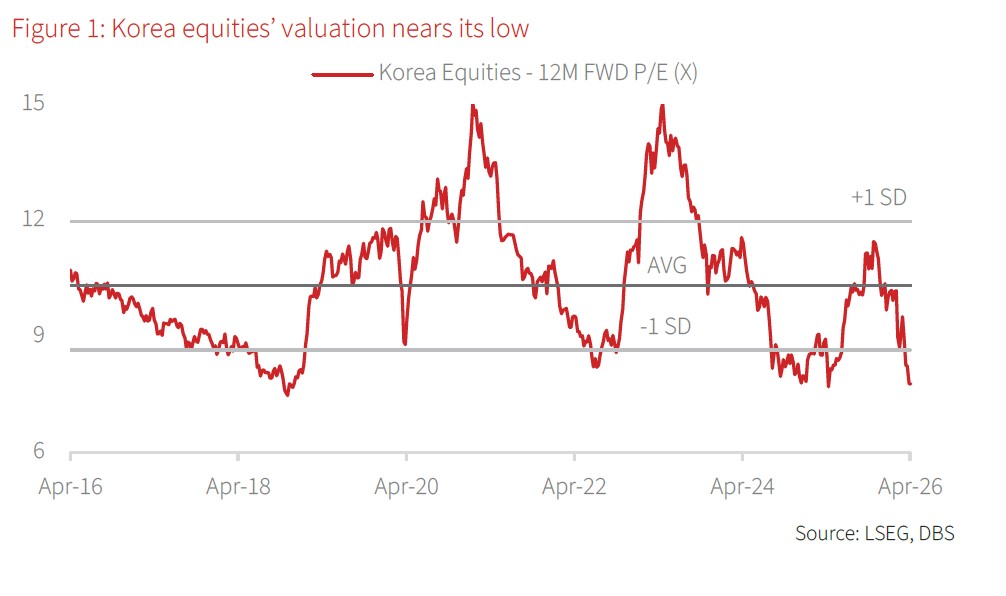

- Earnings outlook remains strong and valuations more attractive; growth is led by semiconductors with momentum broadening to industrials such as defence and shipbuilding

- Korea’s semiconductor sector (c.44% of KOSPI’s market cap) is well-positioned for the next leg of AI-led demand, supported by tight HBM supply, improving memory ASPs, and potential 2026 EPS upgrades

- Exposure to Korea stocks can be gained through Korea ETFs, Korea/Asia ex-Japan funds, or ADRs/GDRS

Related insights

- Singapore Equity Picks29 May 2026

- FX Tactical Ideas: A More Supported USD29 May 2026

- CIO Industry Guide: May 202629 May 2026

The recent dip in Korean equities, following an impressive rally that outperformed global peers, presents an opportune moment for investors to re-engage with Korea’s compelling growing narrative. The pullback appears to be a consequence of profit-taking and temporary risk aversion from Middle East tensions rather than the deterioration of underlying fundamentals. While sentiment was weighed down by AI angst as investors reassessed monetisation timelines & capex spending, strong US dollar tightening liquidity & pressuring flows, and concerns over Korea’s high oil dependency amid elevated oil prices, we believe these factors are largely cyclical while Korea’s robust secular growth trends remain intact.

Navigating higher oil price. South Korea has one of the highest fuel import dependencies in Asia. Net fuel imports amounted to around 6% of nominal GDP in 2025. The country sources roughly 70% of its crude oil from the Middle East and about 20% of its LNG from Qatar.

The government has responded with a broad set of stabilisation measures, including fuel price caps and expanded fuel tax cuts. It has also released strategic petroleum reserves to support supply and also, introduced demand-side controls, such as vehicle-use restrictions for the public sector and campaigns encouraging households & firms to reduce fuel consumption. In addition, a supplementary budget of KRW26.2tn has been announced to cushion the economic impact of higher energy prices.

For the Bank of Korea, the key challenge is balancing inflation control against growth risks. The governor has indicated that a supply-driven and potentially temporary oil shock should generally be “looked through.” This implies that rate hikes are not the base case and would likely require more persistent oil price increases, a rise in inflation expectations, and clear second-round effects in wages and prices.

Earnings fundamentals remain strong with attractive valuations. Despite the tension, Korea’s superior earnings growth story remains strong and is now offering more compelling valuations. The market consensus expects Korea equities to achieve more than 100% earnings growth in 2026, propelled by semiconductor earnings upgrade on a prolonged supply deficit and surging AI demand. Its earnings momentum is also broadening to other sectors such as industrials, particularly defence and shipbuilding, benefitting from structural global demand and strong competitiveness.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Singapore Equity Picks29 May 2026

- FX Tactical Ideas: A More Supported USD29 May 2026

- CIO Industry Guide: May 202629 May 2026

Related insights

- Singapore Equity Picks29 May 2026

- FX Tactical Ideas: A More Supported USD29 May 2026

- CIO Industry Guide: May 202629 May 2026