- Oil prices up close to 60% in the aftermath of the US-Iran war

- Further spikes possible in case of a protracted conflict

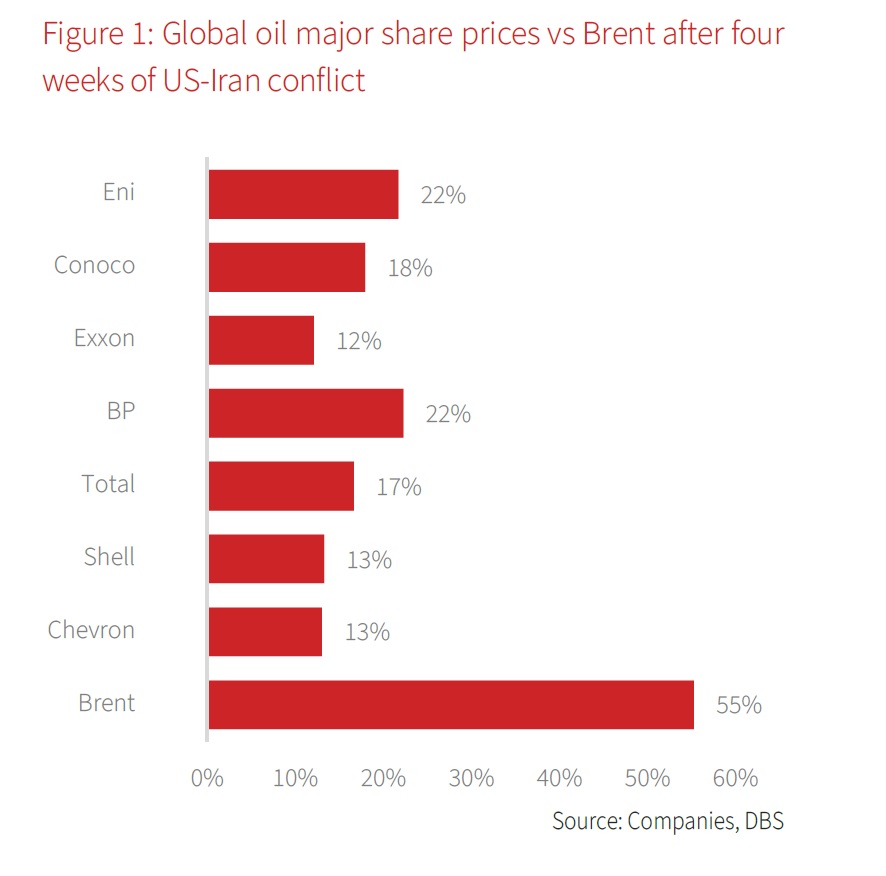

- Oil majors’ share prices have reacted conservatively so far

- Downside protection stems from “higher-for-longer” oil price outlook

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026

Oil price forecasts revised upwards due to disruptions from US-Iran war. While Donald Trump has indicated that the US may exit Iran in as soon as two weeks, the situation on the ground in the Middle East remains uncertain. Post exit comments from Trump, Iran launched overnight attacks at Israel, Bahrain, Kuwait and an oil tanker off Qatar and United Arab Emirates. Traffic in the Strait of Hormuz remains largely closed at this point. Additionally, direct attacks on critical energy infrastructure means that, even in the event of a cease-fire, oil production in the Middle East will not return to pre-war levels for a while. Under these circumstances, we have recently raised our average annual oil price forecasts for 2026/27 and we now project Brent crude oil prices to average between USD77-82/bbl for 2026 (up from USD62-67/bbl earlier). While our base case forecast for oil price assumes a 4–6-week severe disruption followed by normalisation, a longer conflict could lead to sustained oil prices well above USD100/bbl, potentially reaching USD150/bbl or higher in the next two quarters under upside risk scenarios.

Increasing odds of higher-for-longer oil prices. What began as a logistics problem in the Gulf, with tankers unable to load and storage filling rapidly, has quickly turned into a production crisis, as Gulf countries were forced to “shut-in” production. Ultimately, the pace at which Gulf export routes normalise will be crucial for the trajectory of oil prices. As will the pace at which shut-in wells can ramp up once trade routes are back to normal. Suffice to say the “oil glut” fears prevailing since late last year is a distant memory now, and even if we reach a ceasefire in the conflict, oil prices will remain at elevated levels compared to pre-crisis levels. While a record IEA reserves release of 400mn barrels aims to provide some short-term relief, it is viewed as a temporary bridge rather than a concrete solution.

Oil majors’ share prices are slowly starting to factor this in. The energy sector is the only major S&P sector trading in the green after four weeks of conflict, but oil majors have had a relatively muted early reaction to the Iran crisis, especially in the first two weeks. Once it has become clearer that the conflict is not a short-lived one and oil price impact will be more than a fleeting one, upstream and integrated names are factoring in more optimism now. On average, the global oil majors are up around 17% since the start of the conflict, compared to 55% rise in oil prices (and 20-25% revision in average forecasts). Thus, we believe downside risks are low even if we see de-escalation anytime soon. Oil majors’ earnings are expected to benefit not just from oil price uplift, but also refined fuel spreads, spot LNG prices, and trading profits arising from high market volatility. Further share price upside cannot be ruled out if the crisis is a prolonged one, which is very much on the cards.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026