- While high interest rate volatility and shifting policy communication cloud the outlook for bonds, investors should not miss the obvious fact that present IG yields of >5% bodes very well for future returns in the asset class

- Such high yields represent a tiny window of opportunity since the post-GFC low-yielding environment to obtain inflation-beating returns

- Under various scenarios of Fed rate projections – including historical analogues – we anticipate positive excess returns of holding a 3-5Y IG credit portfolio to maturity vs holding cash over the same horizon

- The high rates on cash could dissipate sooner than thought once the cutting cycle is under way. To mitigate reinvestment risk, investors should take this golden opportunity to switch from cash to credit to lock in today’s yields for the years to come

Related insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025

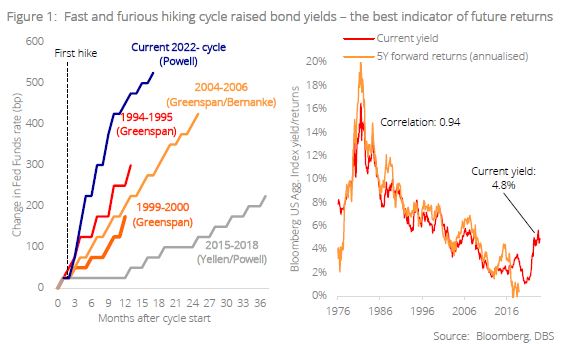

The great Fed-given opportunity for fixed income. While much has already been said about the latest Fed hiking cycle and its far-reaching impact on both financial markets and the real economy, we believe that complexity can sometimes blind investors to the opportunities hiding in plain sight. Bond yields today are the highest they have been in decades, boding very well for future returns in the asset class.

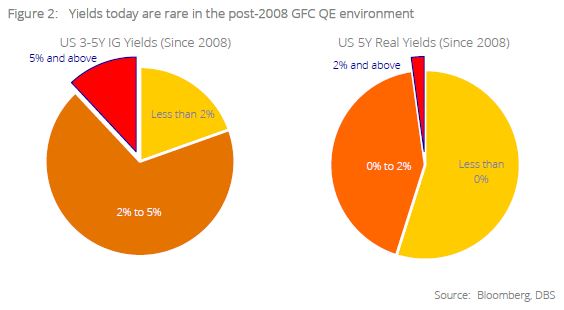

A narrow window in history. This stepwise shift in rates over a short period has propelled yields on investment grade (IG) credit (with historically low default rates) to altitudes of rarefied air (>5% in nominal terms and >2% in real terms). Since the advent of quantitative easing (QE) following the 2008 Global Financial Crisis (GFC), in only 12% of the time did yields on high quality credit exceed the 5%-handle, attesting to how limited this window of opportunity is. Furthermore, if you consider this from a real (inflation-adjusted) yield perspective, the window looks even tinier. Real yields have surpassed the 2%-handle in only 2% of time over the same period, where much of it was in fact spent in negative territory. While the world debates whether inflation would eventually settle at 2% or 3% over the next decade, let’s not miss the fact that IG credit yields at present would beat inflation in either scenario.

Higher for longer, but not higher forever. Yet it is not the narrowness of the window alone that underpins this golden opportunity; it is the fact that the Fed – as well as other central banks around the world – have indicated that the monetary policy cycle is about to turn. The debate around a lower yield environment is therefore not a matter of if, but when. The Fed in particular, has clearly illustrated through its dot plot that they expect a declining yield environment over the next three years.

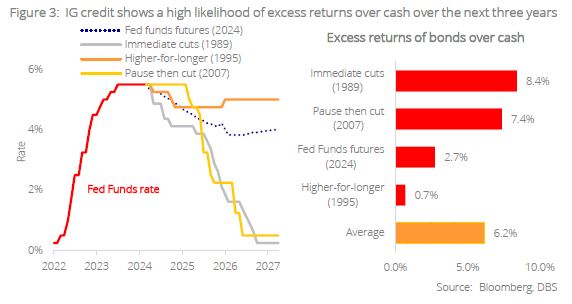

Don’t fight the Fed. While we would not know precisely when rate cuts would take place, we thankfully have several analogues to guide us – specifically four different pathways including the historical precedents of (a) immediate cuts – following the 1989 pause, (b) higher-for longer rates – mimicking the 1995 pathway, (c) pause then cut – such as in 2007, as well as (d) using the current Fed Funds futures projections. Using these pathways of the Fed Funds rate, we compared the expected excess returns of (i) holding a 3–5Y credit portfolio to maturity vs (ii) cash over the next three years.

Credit wins in every circumstance. Regardless of pathway, credit outperforms cash in every scenario – including the much feared “higher-for-longer” analogue. This suggests that we need not wait for rate cuts to happen before switching from cash to bonds – the time is now.

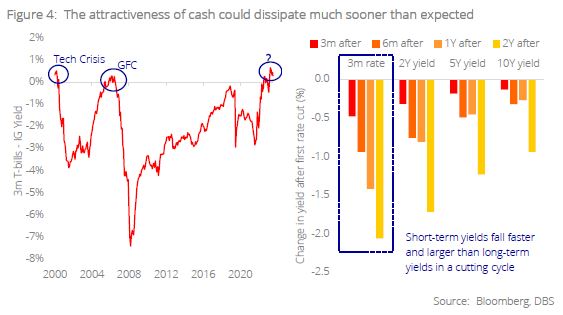

Today’s yields tomorrow. We believe that the main hinderance in the bonds vs cash argument is the fact that cash yields are high at present; limiting the pickup in yield one would get switching into bonds. Yet history suggests that these are precisely the periods that cash returns are at their most perilous (Figure 4). Over more than two decades of data, we see that high cash yields normally preceded some form of unexpected crisis, resulting in central banks having to intervene and slash interest rates quite drastically. When central banks do cut rates, we also note that short-term yields would fall faster than longer-term yields as the cutting cycle progresses. This speaks to the large reinvestment risk that holders of cash are prone to as monetary policy reaches an inflection point. With this narrowing window for higher fixed income yields, investors would do best to trade cash for credit to lock in such abnormally high yields for the years to come. Got bonds?

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025

Related insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025