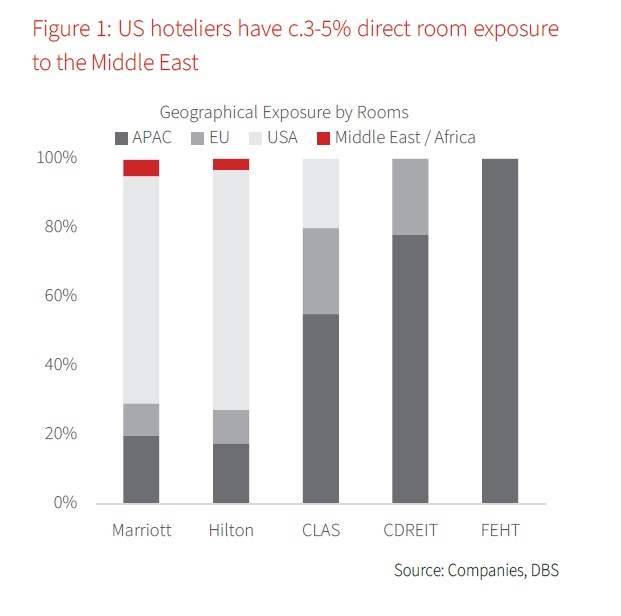

- Major US hoteliers have limited direct exposure to the Middle East; the region contributes 3-5% of total fee income and global room inventory

- Second order impact from higher oil prices, including elevated travel and utility costs, warrants monitoring as it can dampen long-haul demand and add margin pressure to hotel operators

- Luxury and higher chain-scale segments should remain relatively resilient compared to midscale and lower-tier segments given stronger pricing power and customer stickiness

- We prefer Singapore players with undemanding valuations and exposure to resilient long stay lodging over US hotels

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026

US hotels face geopolitical crosswinds. US hoteliers are facing souring sentiments in the face of escalating geopolitical conflict, although impact thus far appears more sentiment-driven than fundamental. Latest RevPAR (revenue per available room) guidance for Marriott and Hilton remains unchanged at 1.5 - 2.5% and 1-2% respectively, and has yet to fully reflect travel caution to the Middle East region. That said, direct exposure to the region remains limited as the region contributes 3-5% of total fee income and global room inventory for both companies. However, we believe that the second order impact to the broader travel ecosystem warrants monitoring, including the effect of higher oil prices.

Second order impact to watch through higher air fares and lower willingness to travel. Higher oil prices are likely to feed through into elevated airfares and other travel costs, potentially dampening long-haul demand while adding to margin pressures for hotel operators. We also see lowered willingness to travel amongst consumers over safety concerns, especially to markets close to the centre of the political war, and potential cancellations or delays at conferences and events. Like prior periods of macro softness, midscale and lower-tier segments are likely to bear the brunt of any demand pullback, while luxury and higher chain-scale segments should remain relatively more resilient given stronger pricing power and customer stickiness.

Position for domestic travel, long-stay lodging to neutralise a weakened global travel outlook. The World Travel & Tourism Council (WTTC) estimates that the Middle East accounts for 5% of global international arrivals and 14% of global international transit traffic. Potential route disruptions and higher air fares could reduce global travel guidance this year, with domestic demand likely more resilient to fill the gap. Both Marriott and Hilton have meaningful global diversification, with fee-income led growth through higher room inventory. Within Asia, we see Singapore/Hong Kong benefitting as interim transit hubs in place of the Middle East. Potential demand spillover to these two markets will benefit S-REITs (c.60% exposure to Singapore). We prefer Singapore players with undemanding valuations and exposure to resilient long-stay lodging over US hotels.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026