- China’s healthcare sector is evolving from a generic-focused, low-cost distributor towards an innovator of biopharmaceutical medicine, driven by strategic government policies

- The country’s R&D capabilities are gaining international recognition, evidenced by record-high licensing-out deals and rising collaborations with MNC pharmaceutical giants

- Policy landscape is expected to remain conducive as China continues to pursue high-quality economic growth in its 15th Five Year Plan; overseas regulatory uncertainties seem to have peaked

- Ageing demographics, combined with lengthening life expectancy, is fuelling the emergence of a “Silver Economy” and expansion of healthcare demand—particularly for age-related conditions

- Confluence of supportive policies, global recognition of R&D, and favourable demographics creates co

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026

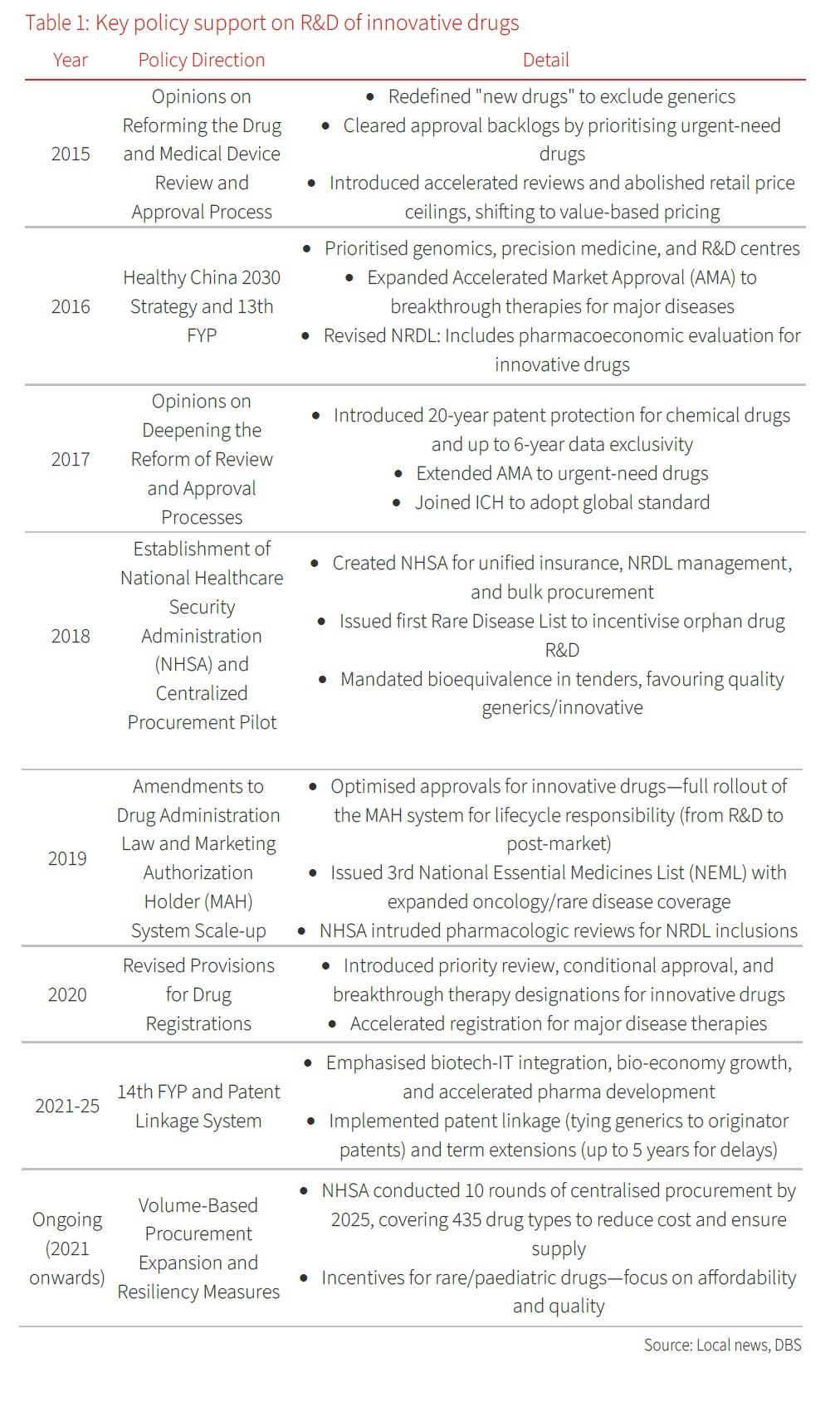

Undergoing profound transformation. The China healthcare sector, once a sprawling landscape dominated by generic drug manufacturing and low-cost distribution, is undergoing a profound metamorphosis. From its erstwhile role as a mere derivative and contract manufacturer, China has rapidly ascended the value chain, emerging as a significant innovator in the biopharmaceutical realm. This transformation is not accidental, but rather, the deliberate outcome of a series of insightful government policies, including ongoing reforms to the Basic Medical Insurance (BMI) system, vigorous promotion of drug R&D, and streamlined drug approval processes. China’s burgeoning R&D capabilities are now earning global recognition, evidenced by a surge in overseas revenue in domestically developed drugs, a flurry of record-high licensing-out deals, and escalating collaborations with MNC pharmaceutical companies.

Coupled with an ageing demographic, rising disposable income, and an extended retirement age, the total addressable market (TAM) for China’s healthcare sector is expanding considerably, presenting investors with compelling opportunities.

Tailwind #1: Policy as a palliative for innovation. In the past decade, China’s role in the global innovative drug market has seen a notable uptick. The 2015 pharmaceutical regulation reforms and China’s membership in the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) have been pivotal. These have enabled China’s innovative drug R&D, regulation, and commercialisation to converge with the highest global standards. This convergence, amplified by China’s vast population, favourable cost dynamics (labour and R&D costs are 30-50% of global levels per data from East Capital, contributing to more affordable and efficient trials), and explicit regulatory backing, has dramatically improved the R&D environment for innovative drugs.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026