- Gold has sold off sharply in response to the Iran war, defying its usual safe-haven role due to inflation and rate concerns

- The sell-off is partly liquidity-driven, with gold used to meet margin calls amid broad risk-off conditions

- Futures positioning and ETF outflows also suggest profit-taking and technical pressure rather than structural bearishness

- Rising energy prices from Middle East disruptions have lifted inflation expectations, yields, and the US dollar, weighing on gold

- Near-term volatility is expected, but the long-term bullish case for gold remains intact, with scope

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026

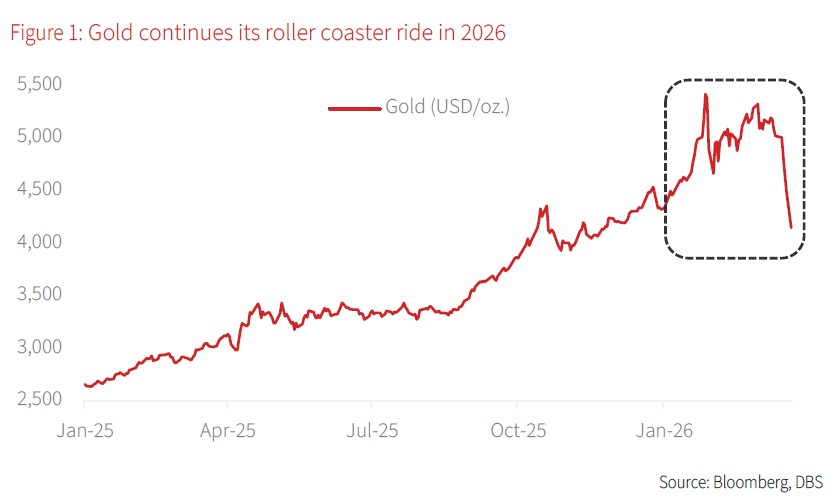

An atypical response to geopolitical risk. Gold has not reacted to the US-Iran war as it typically would in other conflicts. The expectation was for increased hedging demand and more durable risk premiums for gold, but the opposite has unfolded; aside from a momentary spike in the immediate aftermath of the opening strikes, gold has been on a sharp downward trajectory. As at 24 Mar, gold is hovering just above the USD4,300/oz. mark, and is roughly flat on a YTD basis. So why has gold made such unprecedented moves (again) and defied its role as a traditional safe haven amid the chaos of war? The short answer is inflation; markets are pricing in the probability of a protracted conflict, higher-for-longer energy prices, and eventually higher inflation and rates. The immediate selling pressure that we are witnessing is also liquidity-related to some extent, where gold is being used as a funding source for margin calls as the war continues to drive a volatile risk-off market. In short, there are both technical as well as fundamental factors that are worth noting for this sell-off.

Correlations lining up suggest liquidity-driven selling. Several datapoints suggest the current sell-off is at least partially liquidity-driven. Firstly, gold is falling in tandem with other asset classes, including equities, bonds, and even cryptocurrencies. The sharp moves amid a broad risk-off market environment suggest gold is being used as a funding source to meet margin calls for other assets. We compared the correlation between gold and other major asset classes pre-war and post-war and found that gold became significantly more correlated with all other major asset classes, sans crude oil, in the latter period. This is a sign of liquidity-driven selling and is similar to what happened during the Covid-19 pandemic, when gold dropped c.12.5% despite massive uncertainty due to funding needs elsewhere.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026

Related insights

- Morgan Stanley24 Apr 2026

- Research Library24 Apr 2026

- USD two-way risks amid US-Iran tensions 24 Apr 2026