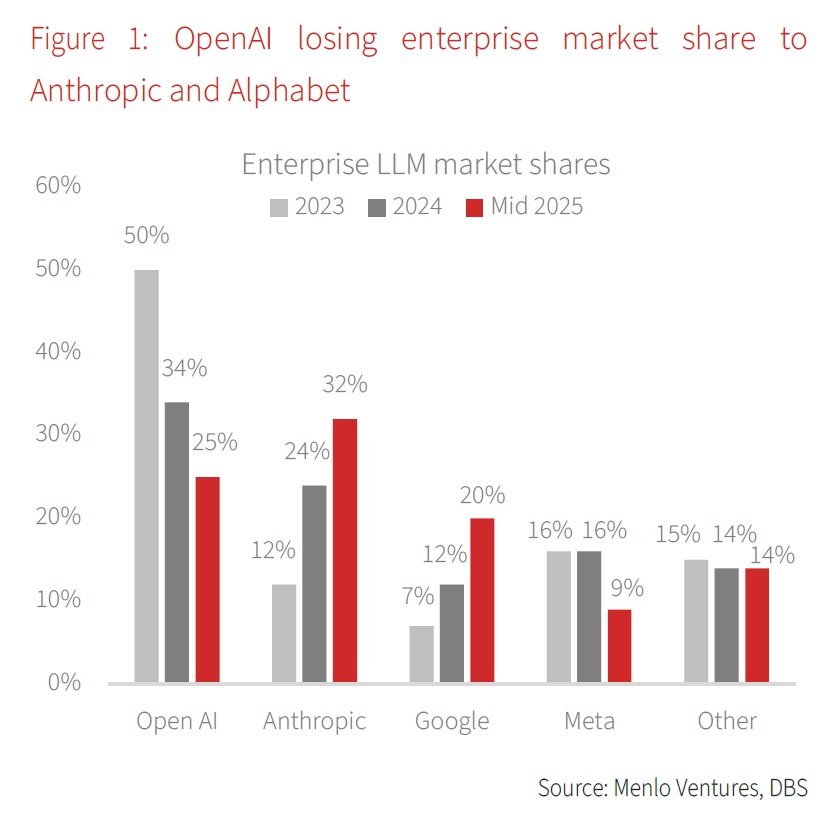

- OpenAI is ceding enterprise share to Anthropic/Alphabet, raising funding risk that could delay fulfilment of >USD1.4tn infrastructure commitments

- US data-centre growth is constrained by grid congestion where some key hubs reported 2–5-year of wait time, unlike China’s remote, power-abundant hyperscalers’ bases

- While DRAM suppliers’ shift toward high margin HBM is driving memory price inflation and weighing on PCs and smartphones, the impact on AI players remains limited

- China’s domestic AI chips are moving from inference to training – supporting a multi-year substitution away from US AI chips

- We prefer full-stack AI plays in China as their vertical integration support cost-performance for clients

Related insights

- Research Library04 Mar 2026

- Caution as DXY approaches 100 04 Mar 2026

- GDP Nowcast: India’s GDP growth likely to moderate in 1Q 04 Mar 2026

We see two challenges in the AI space specific to the US. First, the world’s biggest large language model (LLM) player, OpenAI, has been losing market share in the enterprise space to Anthropic and Alphabet. This casts doubt on OpenAI’s ability to raise funds. Meanwhile, OpenAI has made several significant deals with a total estimated value of over USD1.4tn in future commitments for GPUs and cloud infrastructure. If OpenAI continues to lose market share and is unable to raise funds, there is a risk of it not being able to fulfil orders with Oracle, Broadcom etc. On the other hand, key LLM players in China such as Alibaba, TikTok, and Baidu are not reliant on external funding to fulfill their capex commitments. Second, we see challenges in the US data-centre space where power crunch is causing significant delays for new DC projects. Northern Virginia – the largest DC market in the US – is facing severe grid congestion while cities like Phoenix, Dallas, and Atlanta are reporting 2–5 year wait times for new capacity. Meanwhile, we don’t see any power crunch in China as many hyperscalers’ DCs are already operating in remote regions with abundant cheap power. The third challenge is the recent surge in memory prices due to manufacturers diverting their production towards high-margin high bandwidth memory (HBM) for AI. This has caused a memory supply shortage for consumer electronics (PCs, smartphones) which are forced to pass down the costs to consumers.

China is also accelerating the build-out of a domestic AI chip ecosystem. There were four AI chip IPOs completed across China onshore and in Hong Kong since 4Q25, boosting sentiment. Meanwhile, Baidu has proposed a spin-off to separately list its AI chip arm Kunlunxin, and Alibaba is reportedly preparing an IPO for its chip unit T-Head. Equally important, domestic accelerators are being paired with maturing software stacks that reduce developer switching costs. This is done either via CUDA alternatives (e.g., Moore Threads’ MUSA) or other CUDA compatibility architecture for model training. Domestic stacks are progressing from inference to training-grade workloads and are gradually reducing reliance on imported chips especially from Nvidia over time. As such, we see China’s domestic chip developers are pushing for a multi-year substitution cycle rather than a short-term policy trade.

We prefer full-stack AI players such as Alibaba, Baidu in China, and Alphabet in the US. These companies span the AI value chain from chips and cloud to LLM and end-user applications. This matters because vertical integration offers immediate monetisation via chips and cloud in the near term, and applications in the medium term, while other carve-outs (Kunlunxin; T-Head) can act as valuation catalysts. Alibaba’s open-source LLM Qwen has surpassed 700mn cumulative downloads on Hugging Face, while Baidu’s overseas cloud app TeraBox (c.400mn global users), and other Chinese AI applications, such as Kuaishou’s Kling with 60mn+ creators worldwide, are increasingly signing up global users. Among the US players, we prefer Alphabet for its ability to break the monopoly of OpenAI in LLM and Nvidia in GPUs for training.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Research Library04 Mar 2026

- Caution as DXY approaches 100 04 Mar 2026

- GDP Nowcast: India’s GDP growth likely to moderate in 1Q 04 Mar 2026

Related insights

- Research Library04 Mar 2026

- Caution as DXY approaches 100 04 Mar 2026

- GDP Nowcast: India’s GDP growth likely to moderate in 1Q 04 Mar 2026