- Momentum has picked up in Japan and is expected to persist in 2Q24 on the back of BOJ’s policy shifts

- BOJ has embarked on policy normalisation and indicated that financial conditions will remain accommodative

- We maintain our neutral stance on Japan amid ongoing uncertainties; focus on sectors bolstered by government stimulus

- Gain exposure to Japan banks on rising fee and commission income as well as on going support from resilient business structures

- Seek opportunities in Japan’s semiconductor sector given the country’s status as the largest semiconductor material manufacturer and active government support

Related insights_tr

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024

Momentum picking up. In the first quarter of 2024, Japan’s TOPIX index resumed its upward trajectory as global risk appetite increased, buoying Japanese stocks. The BOJ’s decision in December 2023 to delay policy normalisation and the yen’s depreciation provided a sense of relief to equity investors who had been concerned about the potential repercussions of a shift in monetary policy. Despite economic challenges, Prime Minister Fumio Kishida’s structural reform initiatives garnered positive attention from investors, overshadowing concerns about the country’s economic weakening. Foreign investors re-engaged with Japanese equities, particularly as uncertainties persisted in the outlook for Chinese equities. Additionally, a global rally in semiconductor stocks boosted related technology, industrial, and chemical sectors in Japan. Notably, Japan’s TOPIX emerged as the top-performing index in the first quarter, delivering a robust 18.9% return in local currency terms and 10.7% in USD.

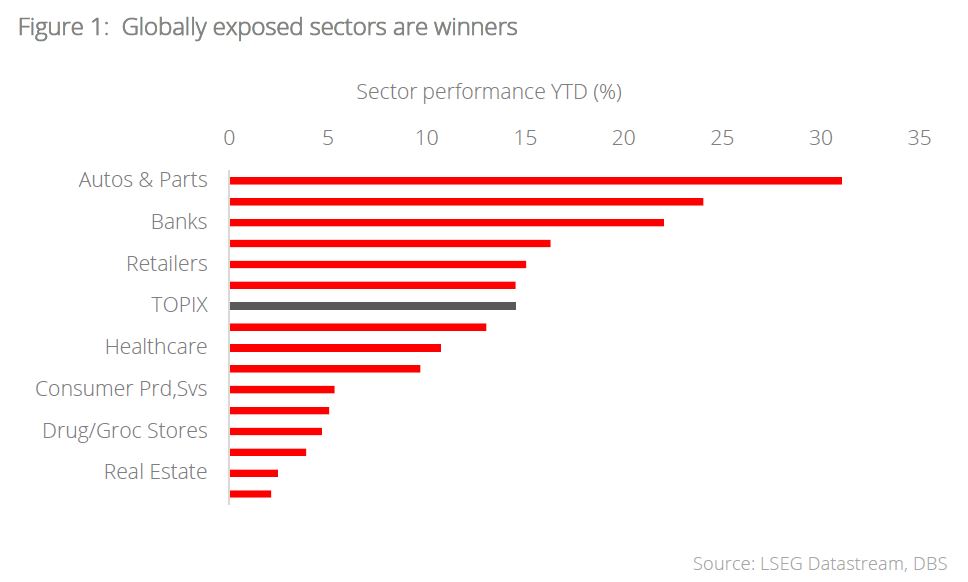

Stocks with global exposure benefiting. In terms of individual sectors, those with significant exposure to global earnings exhibited stronger performance compared to domestically oriented sectors. Notably, sectors such as Automobiles, Electronics and Electricals, and Machinery, which are pivotal to Japan’s economy, outshone others. While financials are anticipated to benefit from the shifting interest rate regime, major banks are currently reaping substantial profits from fee income amid buoyant financial markets. However, companies must adeptly navigate challenges, including rising material and labour costs, as well as subdued domestic and Chinese consumption, before demonstrating robust profitability to bolster share prices.

During the 4Q reporting season, absolute earnings declined by 12.2% y/y but overall results surpassed consensus earnings estimates by 3.9%. However, there is considerable variation among sectors. Technology and financials exhibited positive earnings growth and surpassed expectations, whereas communications and consumer staples experienced both negative growth and surprise. More companies witnessed downgrades rather than upgrades to their earnings forecasts, reflecting a lack of confidence for a sustained recovery. Consensus estimates 3% earnings growth in 2024, dragged down by the IT and energy sectors, which we believe could have upside surprise judging by the orderbook and stable oil price.

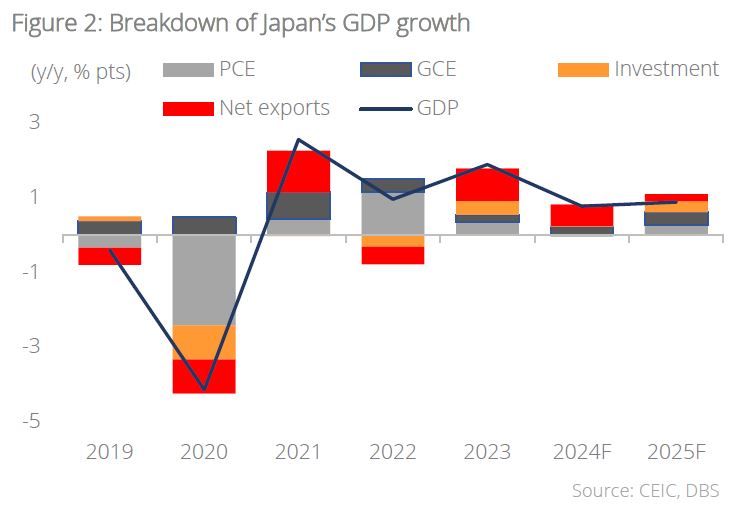

Technical recession in 4Q23, slower growth in 2024. In the October-December period, Japan’s GDP unexpectedly fell by an annualised 0.4%, following a 3.3% decline in the previous quarter, pushing the country into recession and causing it to lose its position as the world’s third-largest economy. Although the number was subsequently revised upwards and a technical recession narrowly avoided, private consumption, which accounts for over half of economic activity, contracted for two consecutive quarters. This decline in real wages, driven by higher inflation outpacing wage growth, has limited consumers’ purchasing power and dampened overall consumption. Furthermore, Japan’s ageing population presents long-term challenges to consumption patterns. Population decline worsened in 2023, with 759,000 new births compared to 1.59 million deaths, exacerbating Japan’s demographic woes.

Signs of export recovery. Looking ahead, Japan’s GDP growth is expected to remain subdued this year as the temporary benefits of tourism, derived from its borders reopening, fade. However, there are signs of potential export recovery, driven by increasing demand for AI-related technologies, particularly in electronic chips, components, and equipment. The weakening yen is anticipated to continue supporting export revenues, encompassing both goods and services. While the full impact of the establishment of the TSMC semiconductor plant may not be felt until the end of 2024, private investments are expected to pick up in anticipation of future growth opportunities.

We anticipate that the Japanese market will confront several challenges in the coming months, including:

1. A new dawn for BOJ policy

The BOJ has embarked on policy normalisation, ending its NIRP and abolishing YCC. The BOJ will also limit its maximum bond purchases across different yield tenors and end the buying of TOPIX ETFs and Japan REITs. We believe this serves as a stamp of confidence by the BOJ to mark the end of Japan’s deflationary era, accompanied by the return of stable growth and inflation. Nonetheless, BOJ governors indicate that financial conditions will remain accommodative, and that this is not the beginning of a tightening cycle given a still fragile economic recovery.

We believe the end of negative rates is a positive for Japanese corporates given their low debt and high cash levels, since having cash will no longer be a drag on their income. However, with rising inflation and wages, corporates may have to work the cash harder. Two-fifths of companies polled in a Reuters Tankan survey said they are looking to boost capital spending in the financial year and they expect further rate hikes. In conjunction with wage hikes and government efforts to boost corporate ROEs, a virtuous reflation cycle may kick in, benefiting the banks as whole. Before that, however, non-financial corporates will have to grapple with rising costs amid dwindling domestic demand.

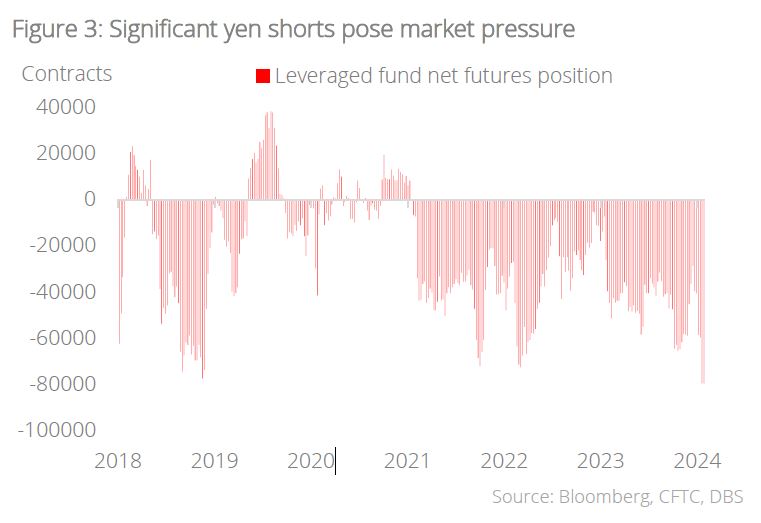

2. Strong positioning in yen carry trades

Investors in Japanese equities should closely monitor the potential impact of a strengthening yen, particularly considering the prevalence of yen carry trades — a popular strategy involving borrowing yen to invest for higher returns. The unwinding of these trades could be particularly volatile due to significant market positioning.

USD/JPY had stayed buoyant around 150 as few expect another rate hike from the BOJ following its decision on NIRP reversal during its policy meeting on 19 Mar. We see a risk for market assumptions of a dovish BOJ rate outlook to be challenged given sharp wage gains, equity market strength, rising productivity growth, and a multi-decade high in loan growth. If the BOJ delivers a less dovish outlook following its rate hike, expect a bump up in JGB yields and a rebound in the JPY.

Meanwhile, the Nikkei index has surpassed its previous peak from the 1989 bubble era, primarily driven by foreign investor inflows. The sudden exit of investors from their yen short positions could amplify market volatility during the unwinding process, especially in sectors that have benefitted from a weaker yen.

3. US Fed policies

The policies of the US Federal Reserve will undoubtedly influence movements in the yen, primarily due to the interest rate differential between US and Japanese bonds, which has historically bolstered the dollar and weakened the yen. Market expectations currently suggest the pricing in of 4-6 Fed rate cuts, which could potentially lead to yen fluctuations driven by a general anticipation of USD weakness resulting from the Fed’s rate cuts. However, uncertainties surrounding BOJ policies, coupled with data indicating a resilient US economy contrasted with a weaker outlook for Japan, further complicate the situation. Despite these factors, it is essential to note that assuming a weak dollar and a strong yen as the base case may not be prudent.

4. US presidential election

The upcoming US presidential election in November is anticipated to be a closely contested rematch between the Democratic incumbent, Joe Biden, and the former Republican president, Donald Trump, who is currently favoured to win, according to polls.

In the event of Biden’s re-election, we anticipate a continuation of broad policy consistency, with a focus on strengthening alliances and addressing global challenges through collaborative efforts.

Both Japan and the US are renowned leaders in technology and innovation. Increased collaboration between the two nations in areas such as AI, 5G technology, cybersecurity, and space exploration holds significant potential to drive innovation, spur economic growth, and bolster the competitiveness of Japanese firms in global markets.

Conversely, Trump’s approach towards China is expected to be more unilateral and transactional, with less emphasis on garnering international support. This stance could adversely affect companies with exposure to China under his administration, as policies may lean towards a more confrontational approach.

5. China’s economic recovery

Japan maintains robust economic ties with China, yet the prevailing sentiment among the majority of Japanese firms regarding China’s outlook remains pessimistic. The primary concern revolves around the prospects of China’s prolonged economic slowdown. In recent years, China has transitioned from a phase of rapid growth to a more tempered pace of expansion, prompting apprehension among Japanese firms. This deceleration poses challenges as it impacts the demand for Japanese products and services in the Chinese market.

In response to these challenges, Japanese businesses are changing their strategies to navigate the slowdown in China’s economy. They are diversifying their markets, prioritising innovation, optimising supply chains, forging strategic partnerships, and leveraging government support. These measures collectively aim to mitigate risks and capitalise on opportunities for growth amid an evolving economic landscape.

Strategy

Maintaining a neutral stance. Amid ongoing uncertainties, we continue to maintain our neutral stance on Japan, recognising that these factors are likely to continue weighing on risk appetite and corporate investment decisions, thereby dampening any upside surprise in Japan’s growth outlook.

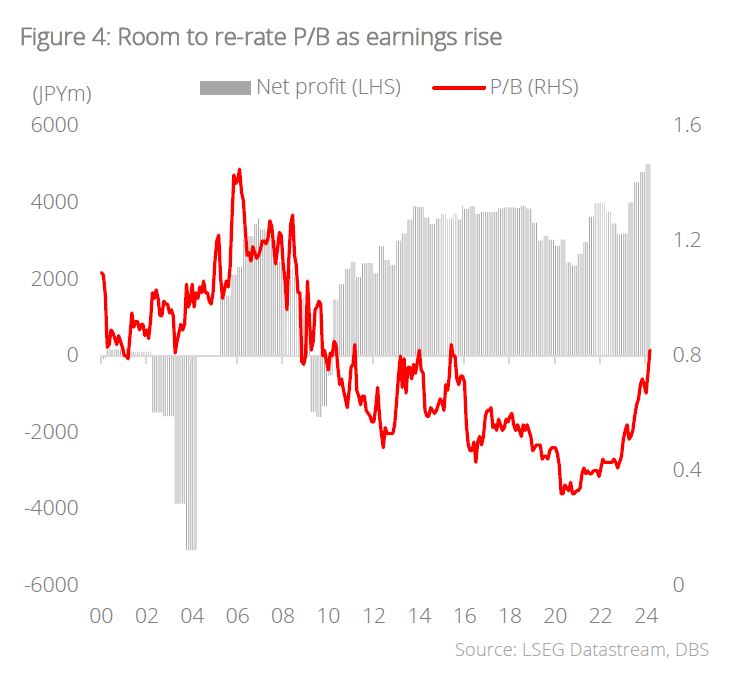

While we acknowledge the challenge posed by potential BOJ policy change and a stronger yen, we do not anticipate it derailing the positive trend. However, given the heightened valuations, our attention is directed towards sectors bolstered by government stimulus and the long-term trend in AI. Notably, banks appear undervalued based on P/B ratios, and the semiconductor industry’s resurgence benefits from robust government support.

Favourable outlook for major banks. We maintain a favourable outlook on Japan’s major banking sector. The three leading megabanks continue to exhibit undervaluation, trading at P/B ratios ranging from 0.7 to 0.9x. Combined net business profits before provisioning across the five major banks saw a robust 14% y/y increase. Fee and commission income continue to ascend, driven by transactions with large corporations both domestically and internationally.

Moreover, evidence of profit growth in fee income has emerged within the banking sector, even prior to any potential adjustment of the BOJ’s NIRP. We anticipate ongoing support for banks’ share prices stemming from the resilient business structures they have cultivated. These structures are poised to capitalise on positive shifts in the macroeconomic landscape, including potential increases in interest rates following BOJ actions.

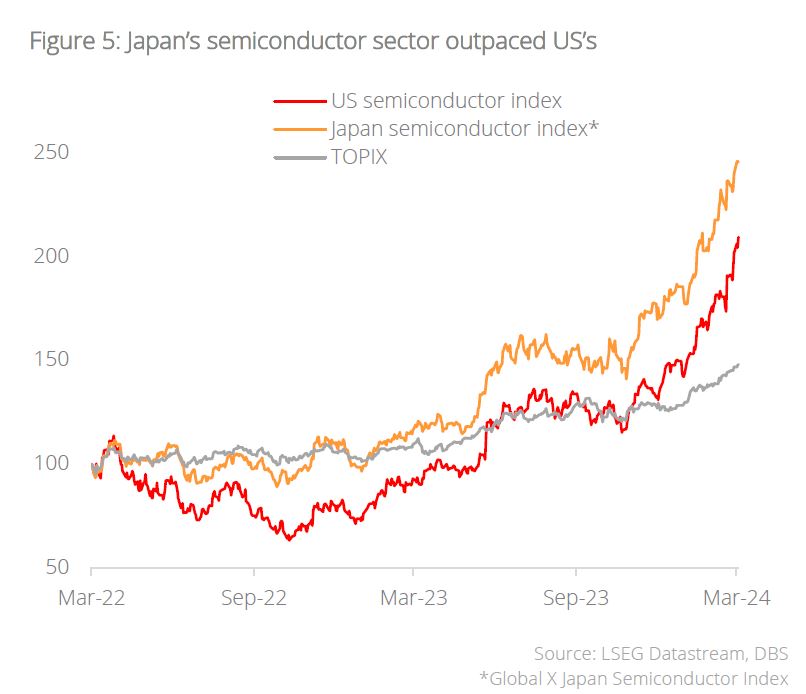

Renewed dynamism in Japan semiconductor sector. The establishment of TSMC’s inaugural Japanese plant in Kyushu signifies a pivotal moment in Japan’s endeavour to rejuvenate its semiconductor manufacturing industry and assert itself as a significant global player in the field. TSMC’s entry into Japan has catalysed investments across the sector, with expectations that it will elevate Japan’s worldwide semiconductor manufacturing share to 3% by 2027. Collaborations between TSMC and Japanese giants like Sony and Toyota aim to fortify Japan’s access to vital chips crucial for various sectors, including electronics, automotive, and defence.

Largest semiconductor material manufacturer. We anticipate a ripple effect on Japan’s already robust chip infrastructure. Japan boasts exceptional capabilities in the tools and materials essential for cutting-edge chip production, with its suppliers often leading the industry in their specialised domains. Notably, Tokyo Electron (TEL) dominates the market for EUV lithography equipment, while Japanese firms JEOL and NuFlare command a significant share in mask-making globally. Japan stands as the world’s largest semiconductor material manufacturer, with over 50% share in critical materials such as photomasks, photoresist, and silicon wafers.

Nurturing domestic leadership in semiconductors. Japan is actively fostering the growth of its semiconductor sector, revitalising hubs in Kyushu, Tohoku, and establishing a new one in Hokkaido. Kyushu, often dubbed “Silicon Island,” hosts major Japanese semiconductor manufacturing facilities. Tohoku, encompassing areas around Sendai and Fukushima, accommodates key vendors such as SUMCO and Shin-Etsu, along with Tohoku University, which is renowned for its semiconductor materials research and engineering prowess. Japan’s broader vision includes nurturing domestic leadership through initiatives like Rapidus, led by industry veterans and in collaboration with global leaders like IBM and Europe’s IMEC. This initiative aims to achieve large-scale production of cutting-edge chips on Hokkaido, commencing in 2027.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights_tr

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024

Related insights_tr

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024