- BOJ ends regime of negative interest rates; world’s last central bank to unwind ultra-loose monetary policy after signs of lasting end to decades of deflation

- Financial conditions to stay accommodative given weak macroeconomic backdrop; structural issues remain with reforms needing years to yield results

- Stay constructive on Japan equities as negative rates benefits Japan corporates given their low debt and high cash levels; bond trading activity should pick up going forward

- Japan’s semiconductor sector, megabanks, and consumer stocks with global exposure remain our preference

Related insights_tr

The end of an era. The Bank of Japan (BOJ) has embarked on policy normalisation, ending its negative interest rate policy (NIRP) and abolishing its yield curve control (YCC). The BOJ will also limit its maximum bond purchases across different yield tenors and end the buying of TOPIX exchange-traded funds and Japan REITS. We believe this serves as a stem of confidence by the BOJ to mark the end of Japan’s deflationary era, accompanied by the return of stable growth and inflation. Nonetheless, BOJ governors indicate that financial conditions will remain accommodative, and that this is not the beginning of a tightening cycle given a still fragile economic recovery.

With the removal of the policy normalisation overhang, we are constructive on Japan equities. We believe the end of negative rates is a positive for Japanese corporates given their low debt and high cash levels. Having cash is no longer a drag on their income. Besides, banks should benefit from BOJ normalisation and reflation on the back of higher loan growth, fee income, and net interest margins. As the BOJ turns to market determination on yields, bond trading activity should pick up once again. As it stands, banks still trade at around 0.8x P/B on average, with ROE of 8.5%. We expect the rally on Japan’s megabanks to continue.

The semiconductor sector remains our convicted sector as the government focus on rejuvenating the sector with the aim of elevating Japan’s worldwide semiconductor manufacturing share to 3% by 2027. We anticipate a ripple effect on Japan’s already robust chip infrastructure. Japan boasts exceptional capabilities in the tools and materials essential for cutting-edge chip production, with its suppliers often leading the industry in their specialised domains.

Japan is actively fostering the growth of its semiconductor sector, revitalising hubs in Kyushu, Tohoku, and establishing a new one in Hokkaido. TSMC has established its first Japanese plant in Kyushu in February this year, with the mutual benefit of having big Japanese corporate customers such as Sony, Renesas and Toyota, amongst others.

We note that Japan’s economic growth remains subdued with long term potential GDP growth of around 1%. This is due to an ageing population with a shrinking labour force and consumption base. Structural reforms implemented by current PM Kishida will take years before seeing fruits. We focus on big caps quality stocks in Japan which lead in innovation and global presence. These are in economic heavy weight industries such as autos, automation, electronics and electricals. We prefer consumer stocks where earnings are exposed to global consumers.

Figure 1: “Kishidanomics” vs “Abenomics” – more way to go for TOPIX

Source: Bloomberg, DBS

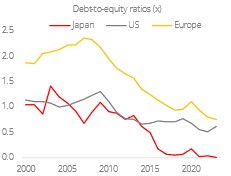

Figure 2: Low debt levels among Japan corporates

Source: LSEG Datastream, DBS

Figure 3: End of negative rates is positive for Japan corporates

Source: Bloomberg, DBS

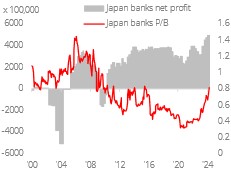

Figure 4: Rally on Japan banks to continue

Source: LSEG Datastream, DBS

Figure 5: Profits are rising

Source: Bloomberg, DBS

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.