- Remain positive on global payments industry in 2024 with long-term growth drivers intact

- Payments players diversifying revenue mix towards value-added services, which is expected to grow at a faster pace

- Market leaders rising the bar through better payments infrastructure and lower costs

- Prefer selective names with a global presence, healthy revenue mix, and less sensitivity to the global economic cycle

Related insights_tr

Riding on the cashless and digitalisation trends. Following robust growth of the global payments industry in 2023, we remain positive on this space amid long-term drivers like 1) Ongoing conversion from cash to non-cash transactions, 2) Rising adoption of e-commerce, and 3) Expanding partnerships worldwide and tapping into new payment categories.

The growth in cross-border volume is expected to outpace domestic payment volume, and this is primarily driven by resilience in travel and tourism, as well as booming e-commerce transactions. Payment players are diversifying their revenue mix towards value-added services (VAS), which is expected to grow at a faster pace compared to payment services. We expect companies with higher VAS mix to deliver low-teens y/y growth in revenue for FY24F and outperform peers with high single-digit revenue growth.

Digitalisation reshaping the competitive landscape. Market leaders of the payments network are raising the bar for digital payments through (1) Faster expansion of partnerships and (2) Entry to new payment categories worldwide. They are tapping on to new flows between individuals, businesses, and governments which provide potential access to more than 10 times the cash and check opportunities seen in traditional payments market.

Leading payment players continue to invest in innovative AI-driven solutions (such as fraud prevention products) to enrich VAS offerings. On the consumer side, new payments and credit rails are growing (this includes digital wallets and buy-now-pay-later (BNPL)) and capturing market share from traditional credit cards. Following years of unrestrained growth, BNPL players are facing mounting headwinds such as regulatory scrutiny, interest rate pressure and intense competition. This may have negative impact on their business.

Prefer names with global presence, healthy revenue mix, and less sensitivity to economic downcycles. We expect payments players to advance through 1) Secular growth in payment services with rising volume and stable take rate, 2) Expansion of partnerships and entry into new payment categories, 3) Scaling up of VAS revenue, and 4) Active support of innovative payment and credit sources, such as digital wallets and BNPL.

Leading payments companies are expected to maintain robust growth momentum. However, companies cutting contracts that previously offered high incentives will face short-term revenue pressure. Moreover, BNPL players are also facing pressure amid regulatory and economic headwinds.

We prefer payments names that possess 1) Global presence which enables them to ride on the digitalisation and e-commerce trends, 2) Higher revenue mix towards VAS, and 3) Lower sensitivity to economic downcycles, and thus, less impacted by consumption weakness and rising credit costs.

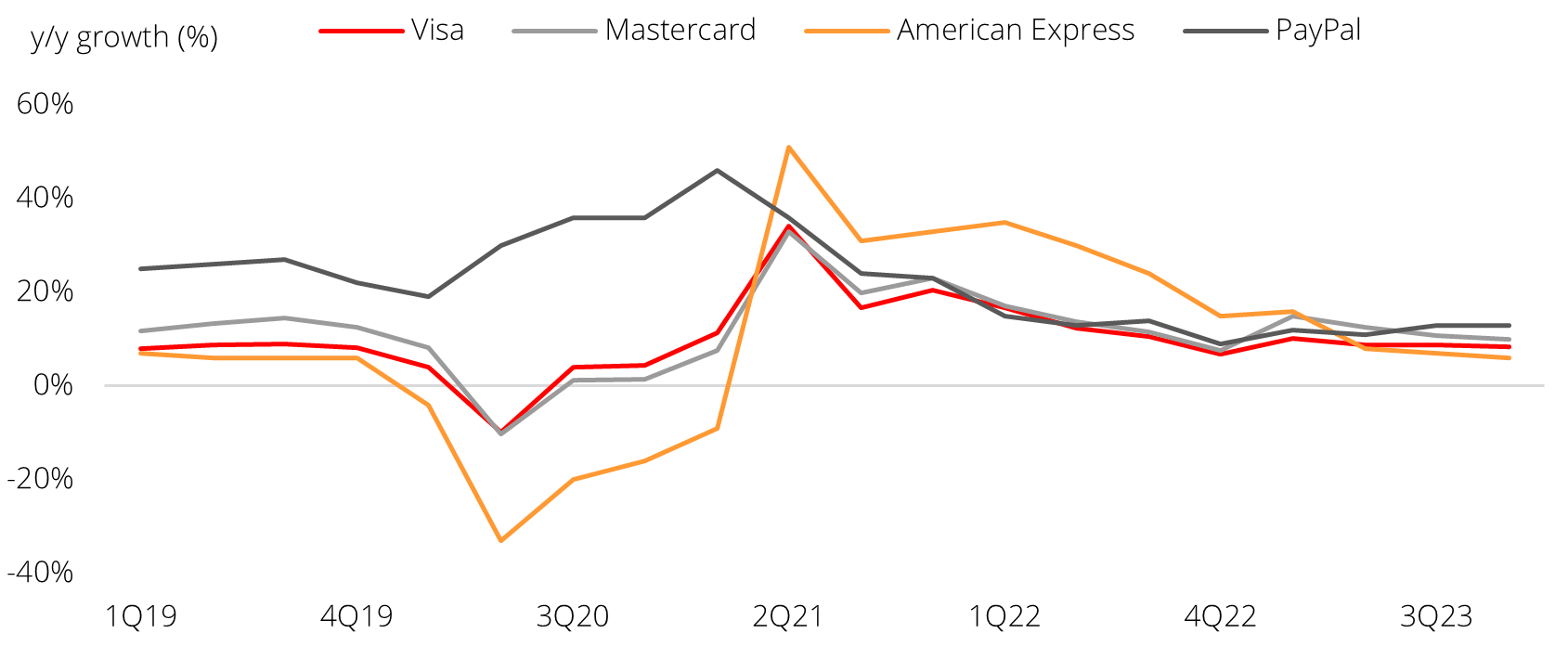

Figure 1: Global payment players’ payment volume, y/y growth (foreign exchange neutral)

Source: Company Data, DBS

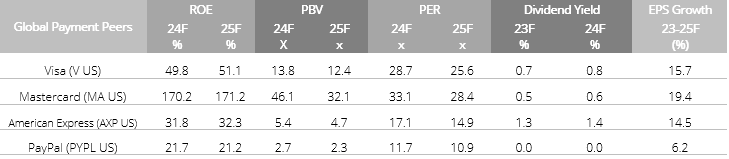

Table 2: Peer Comparison Table

Source: Bloomberg,

DBS Data as at 1 March 2024

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.