- Equities: US and Europe stock marketscontinue to make record highs onpositive technology earnings. China andHong Kong rise on interest rate cuts andincrease in travel consumption spending

- Credit: Corporate credit spreadtightening despite elevated Treasuryyields underscores strength of high-quality corporates in higher-for-longerrates. Avoid duration risks givenunresolved US debt sustainabilityconcerns

- FX: DXY's downtrend not confirmed;EUR/USD could slip below 1.08 again asinterest rate futures see the ECB loweringrates by the same 75-100 bps as the Fed

- Rates: While the 2Y/10Y looks like it wants to retest -50 bps, we maintain our view ofcyclical curve steepening for the year

- The Week Ahead: Keep a lookout for USChange in Initial Jobless Claims; JapanIndustrial Production Number

Related insights_tr

Global equity markets powered higher. The Dow Jones, S&P 500, and NASDAQ rose 1.3%, 1.7%, and 1.4%, respectively for the week (ended 23 February). Stellar earnings from Nvidia propelled US markets higher as the outlook for the technology sector improved. Europe’s stock markets similarly cheered Nvidia’s results as well as the performance of its semiconductor, pharmaceutical, and software sectors, powering the market to record highs. The Stoxx 600 rose 1.2% for the week.

In Asia, Japan’s Nikkei 225 continued to rally 1.6% last week, hitting new highs. China and Hong Kong markets jumped as the People’s Bank of China cut its benchmark 5Y loan rate by a larger-than-expected 25 bps to 3.95%. As most mortgages are pegged to this rate, the cut is beneficial for the property sector. Increased travel spending during the Lunar New Year holiday also boosted market sentiment. The Shanghai Composite Index jumped 4.8% while the HSCEI and HSI climbed 3.7% and 2.4% respectively for the week.

Topic in focus: AxJ Equities – Favourable prospects lie ahead. AxJ equities are poised for a recovery in 2024, fuelled by forecasted earnings growth exceeding 20% for AxJ corporates, which is significantly higher than global markets. This positive earnings momentum is underpinned by the stable economic growth across the region, and we expect further policy support and implementation of fiscal stimulus in China to bolster growth prospects.

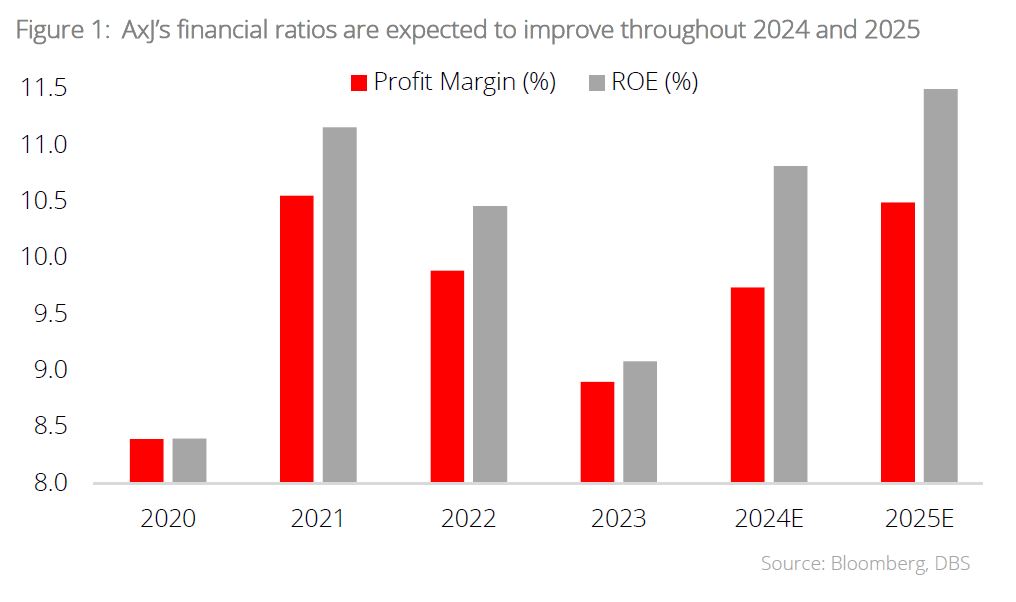

Despite improving fundamentals, AxJ equities are trading at a significant discount on a P/B basis compared to global peers. We believe this discount is largely sentiment-driven and should narrow as confidence in the region's growth prospects and fundamentals improve. According to market forecasts, key financial ratios, including profit margin and ROE, are expected to rebound from the trough observed in 2023 and continue on an upward trajectory throughout 2024 and 2025. Our constructive stance on AxJ remains intact, supported by attractive valuations, the peaking of US interest rates, and robust earnings growth. We recommend staying selective and thematic-driven, focusing on industries that stand to benefit from government expenditure and stimulus.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.