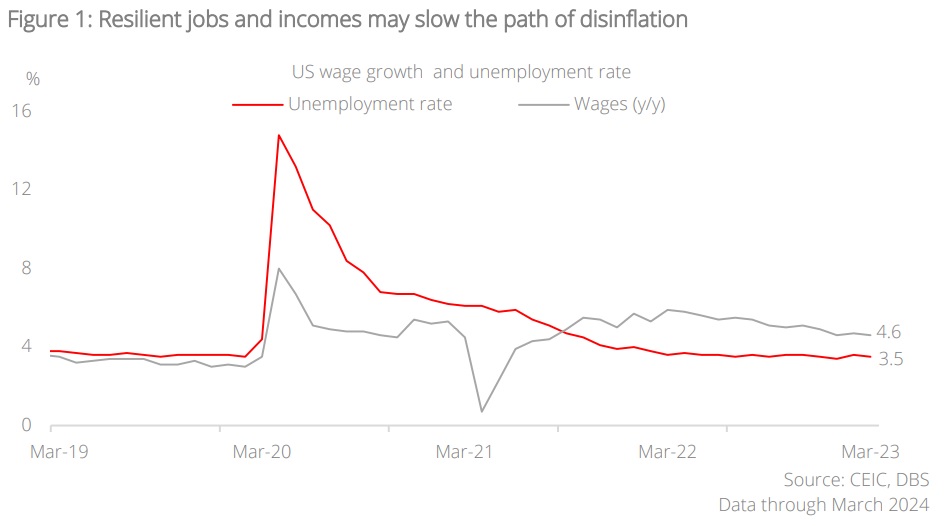

- US: March inflation data shows persistent price pressures; strong labour market may slow disinflation but sharp rebound in inflation is unlikely given spate of supply side reforms underway

- China: Official PMI returns to expansionary territory for the first time in six months amid weaker-than-expected March inflation data

- Taiwan: Economic recovery in Taiwan prompts considerations for policy tightening; cyclical upturn in the global semiconductor sector should continue to drive exports growth this quarter

- Thailand: BOT keeps policy rate unchanged, maintaining patience over current soft economic conditions; updated 2024 growth forecast of 2.6% at lower end of its previous range

Related insights

- India chartbook: Higher gear30 Apr 2024

- Bumrungrad Hospital30 Apr 2024

- DBS Stock Pulse: DHLT – Weighed down by the weak yen30 Apr 2024

US: Sticky inflation taking hold. The March inflation print marked the third month in a row that prices pressures surprised on the upside, triggering a spike in US yields across the curve. Headline and core CPI both came in at 0.4% m/m (higher than consensus of 0.3%). Shelter and gas prices were the two main culprits behind the elevated inflation print. Notably, categories including apparel, medical care, and transportation services also saw meaningful price increases, indicating that inflation is broad-based.

Implications of the strong labour market. Withstanding two years of monetary policy tightening, the US economy continues to chug away at above-trend growth rate, pulling up the labour market with it. The statistics are impressive across a wide range of measures. Unemployment is below 4%, weekly initial claims for unemployment insurance has been near historical lows for over two years, and the labour force participation rate is on the rise after a few years of pandemic-driven dip. Labour market would have been even tighter had it not been for the fact that immigration has picked up, boosting the supply of workers.

Sharp rebound in inflation unlikely. The difference with prevailing inflation and what was seen in 2022 is that it is taking place under favourable supply side conditions, ensuring a cap on potential upside risks going forward. However, clear signs of a high-pressure economy, characterised by strong growth and sticky inflation, is going to make it rather difficult for the Fed to (i) express comfort with the inflation trend and (ii) embark on a rate cut cycle any time soon. Our longstanding call has been rate cuts only in 2H24. That call remains intact, although the type of rate cuts plausible under the prevailing macro scenario is now mired in uncertainty.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- India chartbook: Higher gear30 Apr 2024

- Bumrungrad Hospital30 Apr 2024

- DBS Stock Pulse: DHLT – Weighed down by the weak yen30 Apr 2024

Related insights

- India chartbook: Higher gear30 Apr 2024

- Bumrungrad Hospital30 Apr 2024

- DBS Stock Pulse: DHLT – Weighed down by the weak yen30 Apr 2024