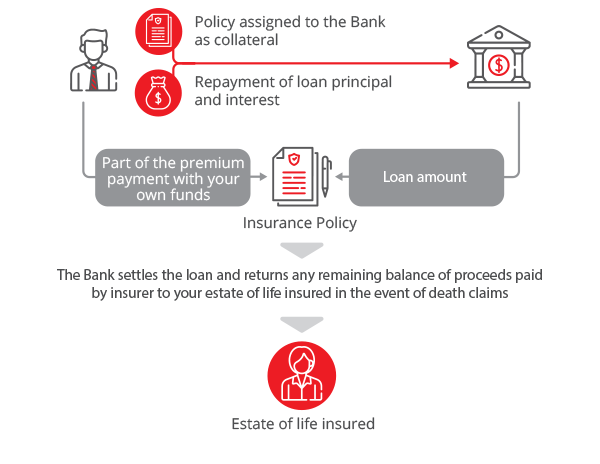

Potential Risks – Things to consider before choosing Premium Financing

As with any lending facility, Premium Financing involves potential risks. Please read and understand the following potential risks in order to make a smart, informed decision about using Premium Financing.

Consequence of late repayment and default of loan facility

By choosing Premium Financing, you agree to repay the loan amount and interest payments according to a repayment schedule and relevant terms and conditions. Late payments or default may be grounds for the bank to demand immediate full repayment and to surrender the policy, causing loss of coverage for the insured and other rights under the policy. You will still be liable for any outstanding amount that is not covered by the value of the surrendered policy. The bank can choose to offset any outstanding amount against any obligations owed to you by the bank (e.g. balances in your accounts with the bank). Furthermore, it may not be possible for you to obtain similar coverage due to changes in health conditions, etc.

Risk of collateral top-up and repayment on demand

The bank reserves the right to review the Premium Financing facility, and restructure or terminate the facility at any time. Under certain circumstances (as stated in the loan facility contract), you may be asked to provide additional collateral, or partially/fully repay the outstanding loan. Failure to meet the requests may trigger the bank to restructure/terminate the loan or surrender the policy. Please read the terms and conditions of the contract, and be sure you fully understand the sections regarding frequency of review, circumstances that may trigger requests and any arrangements related to such requests. Before proceeding, ensure you can financially meet these circumstances before opting to use Premium Financing to finance life insurance.

Impact of early termination/surrender/withdrawal

Please be aware that, should the bank exercise its right to terminate/surrender the policy or withdraw cash before the end of policy term, the following situations may arise:

- The benefits receivable may be substantially less than the total of premiums, interest and early repayment penalty (if applicable), especially in the early years of the policy

- The insured may lose some or all insurance coverage, and may not be able to obtain the same insurance coverage again

- You may no longer be entitled to dividends, bonuses and other revenue from the policy

- The bank may apply all or part of the benefits receivable against the outstanding amounts (whether or not the outstanding amounts are under the loan facility)

- The termination of the policy may lead to further defaults (for example, if the policy is required as a condition of your business, etc.)

Exposure to risk of non-guaranteed benefits

Please remember that the benefits shown in the Benefits Illustration are for illustration only and are not guaranteed. Your actual benefits receivable may be lower, may even be lower than the interest payable for the loan facility, and may even be zero. If the total return from the policy is lower than the interest payable, you will suffer a financial loss.

Exposure to exchange rate fluctuation

If the loan currency differs from the policy currency, you may be exposed to exchange rate fluctuations. With Premium Financing, you may be required to convert the proceeds received under your policy to the loan currency under the prevailing exchange rate in order to settle loan repayments. If the proceeds received from the policy are lower than the outstanding loan amount due to adverse exchange rate fluctuations, you will suffer a financial loss.

Exposure to credit risk

Should the Insurer default on its obligations or suffer an adverse change to its credit rating, the bank reserves the right to request additional collateral from you, adjust your credit limit, or restructure/terminate the loan facility. In case of termination, you will be obligated to immediately repay the loan, all interest and administrative fees accrued, and you will be liable for any shortfall between the amounts of the proceeds of the policy and the outstanding amount of the loan.

Release and access of information

The bank may access your policy information and obtain information relating to your life insurance policy from the Insurer (e.g. surrender value, cash value, and any loans/advances on the policy).

Reminders about Responsible Borrowing

- Before applying for a loan, You should have a clear understanding of your financial condition, daily expenses, and actual borrowing needs.

- To borrow or not to borrow? Borrow only if you can repay!

Disclaimer

The information contained in this article is for general reference only and is subject to the policy terms of different types of insurance plan. This article does not constitute an offer for the purchase or sale of any banking or insurance products or services. Products and services are subject to individual needs. Customers should not solely rely on the information on this webpage alone to make any investment and/or insurance decisions. Premium financing is generally considered to be a payment option for customer which involves borrowing, incurring interest payment (the rate is not fixed), and losing your rights under the insurance policy and other risks. Please contact your Relationship Manager to assess your financial needs and understand the risks involved in Premium Financing before making any financial decision. The specific details, terms and conditions of Premium Financing should refer to relevant Premium Financing loan documents. Customers should read in details for ensuring understanding of risks involved.

DBS Bank (Hong Kong) Limited (“The Bank”) and its officers, agents, representatives and employees accept no responsibility for any reliance on the calculations or conclusions reached by the customer. The Bank accepts no liability and will not be liable for any loss or damage arising directly or indirectly (including special, incidental or consequential loss or damage) from the customer’s use of the information sheet, howsoever arising, and including any loss, damage or expense arising from, but not limited to, any defect, error, imperfection, fault, mistake or inaccuracy with these calculations.

Copyright in all materials, text, articles and information contained herein is the property of, and may only be reproduced, redistributed or forwarded with permission of an authorised signatory of, the Bank. Copyright in materials created by third parties and the rights under copyright of such parties are hereby acknowledged. Copyright in all other materials not belonging to third parties and copyright in these materials as compilation vests and shall remain at all times copyright of the Bank and should not be reproduced or used except for business purposes on behalf of the Bank or save with the express prior written consent of an authorised signatory of the Bank.