We have little control over market conditions and the economic landscape; what we do have is the choice to stay invested. What do news headlines such as “Fed expected to stick with hawkish rate hikes” or “HKD falls as central bank remains dovish” really mean to you, or your investments?

“Hawkish” and “dovish” describe two approaches – amongst many others - used by policymakers to manage the economy. Hawks focus on controlling price increases or inflation by raising interest rates and doves prefer to lower interest rates. Low interest rates encourage consumers to spend, and discourage them from saving, due to unattractive low deposit rates. Low interest rates also mean more are willing to borrow, for example, individuals buying a car, or a house and businesses borrowing to build new factories and buy new equipment.

The effect is reversed when interest rates rise: individuals are more careful with spending and borrowing, and more prepared to deposit their money in the bank. Likewise, businesses may suspend or cut development plans. As market demand for various goods and services fall, so does the inflation rate. It is important to know that a hawkish or dovish situation is neither good nor bad, as either serves different purposes during different economic cycles.

Investing in a rising interest rate environment

Your money should work hard for you regardless of market and economic conditions. In this article, we explore instruments that let you capitalise a rising interest rate environment for your investments.

1. Bonds

Bonds are loan contracts issued by the borrower, which can be a government or a company, to the lender, who buys the bond or subscribes to the issue. The loan quantum is the bond’s face value, the fixed interest payable is the coupon rate, and the loan period is called the tenor or duration.

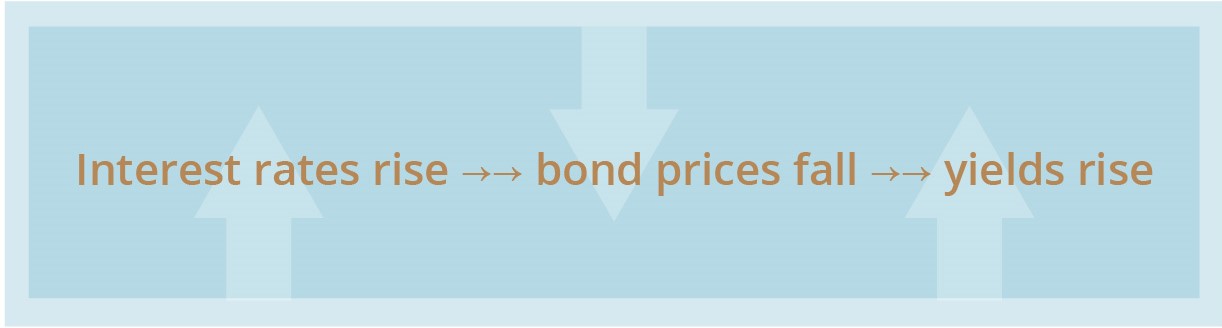

In other words, bonds are described as a fixed income product (some bonds do pay a floating rate) that allows lenders, or issue holders, to receive a fixed amount of interest (income) over a specified time frame, without change. Given the above explanation, bonds that pay a fixed interest rate, or coupon, become unattractive investments when interest rates rise. Consequently, the bond prices in the secondary market will fall, to reflect falling demand. However, even as the bond prices fall, its yield, calculated relative to the bond price, will naturally rise, to attract potential buyers.

The relationship between bond yields and interest rates are governed by many factors but the relative dynamic between bond yields and bond prices does show why it is potentially good to accumulate bonds in a rising interest rate environment.

Here is a simple illustration:

Bond A has a face value of HKD 1,000,000 and pays a yearly coupon of 5%, or HKD 50,000 (1,000,000 x 0.05).

If you buy Bond A when its face value drops from HKD 1,000,000 to HKD 800,000, the coupon you get is still HKD 50,000, but the yield has increased to 6.25% (50,000 divided by 800,000)

As can be seen from the above example, accumulating bonds in a rising interest rate environment can potentially be a good investment move.

2. Structured Products

The performances of Structured Products (SPs) are linked to that of an underlying asset, such as market indices, individual or baskets of stocks, bonds, interest rates or a combination.

Two unique features of structured products are that they can be designed to benefit from a particular market outlook, e.g., when interest rates are rising, and can be customised to meet an investor’s specific needs.

In a rising interest rate situation, potential investors can consider buying into structured products, especially those with an underlying pegged to interest rate movements. Such products can be potentially attractive, as they come with full or partial principal protection, i.e., the investor gets back his full principal sum regardless of market conditions, or the investor is exposed only to the losses incurred after the protection level is breached, and not for to all the losses suffered.

On the flipside, structured products have a fixed investment period and may not be able to sell prematurely; they face market risks, low liquidity, and issuer default risk.

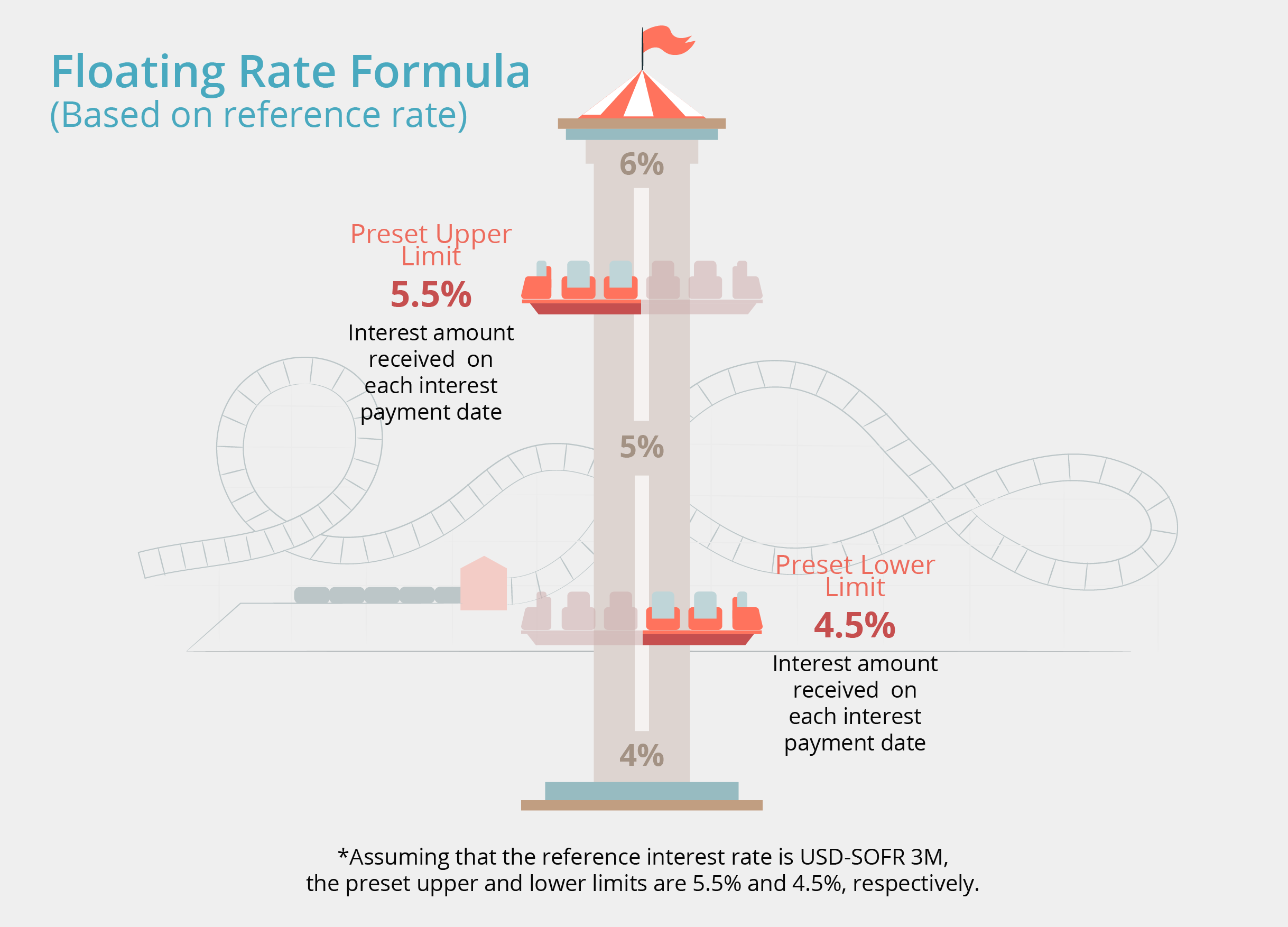

One example of a structured product (SP) is the interest rate-linked structured product, which links its returns to a fixed or floating interest rate. A fixed rate SP pays the pre-determined return throughout the investment period, regardless of how its underlying asset has performed. The payout of a floating rate SP usually has a cap (it cannot pay higher than this rate) and a floor (the payout cannot be lower than this rate), calculated based on a formula.

If the floating rate SP is linked to the US Dollar Secured Overnight Financing Rate 3-Month (USD-SOFR 3M), then the payout on each payment date is calculated based on the USD-SOFR rate at the point of payout.

For example, if the floor and cap of the payout are 4.5% and 5.5%, respectively,

then...

Scenario 1 - USD-SOFR 3M is 4.7% at payout, then the interest payable is 4.7%.

Scenario 2 - USD-SOFR 3M is 5.8%, payout is 5.5%, because there is a cap of 5.5%.

Scenario 3 - USD-SOFR 3M is 3.8%, payout is 4.5%, because there is a floor of 4.5%.

*The example has been provided for illustrative purposes only.

3. Equities

When interest rates rise, borrowing becomes more expensive for individuals and companies, and this can hamper spending and business growth. Companies that produce goods for consumers, e.g., electronics or food, will suffer, as the cost of production goes up on the back of higher borrowing costs. However, financial institutions such as banks become attractive, as they benefit from the higher interest rates that they charge on loans.

Making informed investment decisions

To reiterate, a hawkish or dovish economic environment is neither a good nor bad time to invest. If you wish to make your money work harder for you, then you must remain invested, regardless of the market or economic climate at any time.

But please remember that all investments are exposed to general economic and market risks and specific product and solutions risks. The only way to mitigate such risks is to make informed investment decisions based on sound market insights, expert advice, and having a good grasp of your risk appetite and your investment objectives.

Read on to find out more…

Inflation, interest rates and monetary policy

Investing in a rising interest rate environment