Related insights_tr

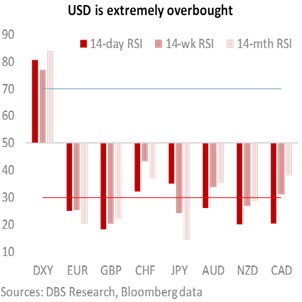

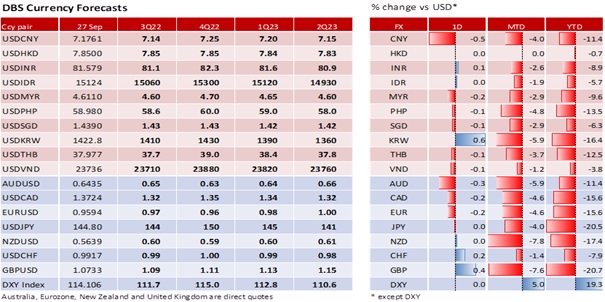

DXY was barely changed at a two-decades high of 114. DXY initially fell to a low of 113.33 during the Asian session. It turned positive after US consumer confidence came in stronger-than-expected at 108 in September vs the 104.6 consensus; August was also revised up to 103.6 from 103.2. The present situation and expectations sub-indices improved on job security and lower gas prices. Echoing the latest projections announced at last week’s FOMC meeting, Fed officials were committed to keep hiking rates to 4.4-4.6% to bring inflation down to its 2% target. Chicago Fed President Charles Evans reckoned the Fed could pause after rates peaked in March. The Fed’s projection to deliver some 125 bps of hikes over the next four meetings suggests smaller hikes are also near, especially if it follows through with a fourth 75 bps hike in November. Despite the positive sentiment, the USD is overbought and struggling to make significant further headway against other oversold currencies.

EUR depreciated 0.2% to 0.9594, its first close below 0.96. The European Central Bank’s top priority is controlling inflation and delivering on its mandate of price stability over the medium-term. To prevent inflation expectations from becoming unhinged, it has signalled several more hikes to return rates to neutral (a level it has yet to define) before deciding if more is needed. ECB President Christine Lagarde noted the weak euro and wide fiscal measures have added to the build-up in inflationary pressures. She added that the strong demand for services from the reopening of economies was losing steam and expects economic activities to slow substantially in the coming quarters. UK’s credibility crisis over its tax cut plans could spill over into Eurozone and the EUR. Even so, EUR is oversold and digesting Monday’s shock GBP sell-off.

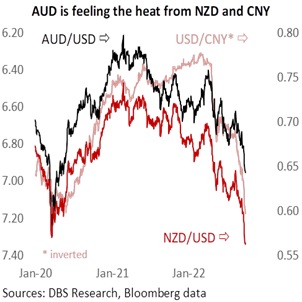

AUD is under pressure to fall towards the Covid-lows of 0.57 (daily close) and 0.5510 (intra-day low) seen in March 2020. NZD held below 0.57, its Covid-low in March 2020, for a second day on risk aversion. The kiwi is setting its sights on 0.5470, the intra-day low on 19 March 2020. Another significant development was the CNY’s 0.5% depreciation to 7.1761 per USD, past the Covid-low of 7.1671 in May 2020. China is Australia’s largest trading partner. The currencies of Australia’s other top trading partners – Japan, South Korea, and India — are also significantly weaker than their pandemic bottoms. All said, AUD and NZD are oversold and may need to consolidate before resuming their slide

Quote of the day

“For every credibility gap there is a gullibility gap.”

Richard Cobden

28 September in history

The Singapore Grand Prix was held as Formula One’s inaugural night race in 2008.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

Explore more

E & S Macro StrategyThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.