Related insights_tr

The market is well-positioned for a hawkish message at today’s FOMC meeting. The Fed is widely anticipated to deliver a third 75 bps hike to 3.25%, into restrictive territory above the estimated 2-3% neutral range. However, the US Treasury (UST) 10Y yield, at 3.56%, is prepared for a surprise 100 bps move. The UST 2Y yield, at 3.97%, is ready to discount a peak in the Fed Funds Rate (FFR) above 4% next year. Hence, the Summary of Economic Projections and post-FOMC press conference will be important. Look for Fed Chair Jerome Powell to reinforce the message that the battle against inflation is far from won.

On the other hand, Powell may temper calls for a rise in the FFR to 5% resulting in a hard landing. At Jackson Hole, Powell did push back against rate cut bets in favour of a pause in 2023. Futures see a peak at 4.50% in 1Q23. With the market divided between those looking for more hikes and those who see the Fed nearing a pause, expect volatility at today’s FOMC. If Powell finds the right balance in his messaging, we cannot rule out the FOMC becoming a “buy the rumour, sell the fact” event.

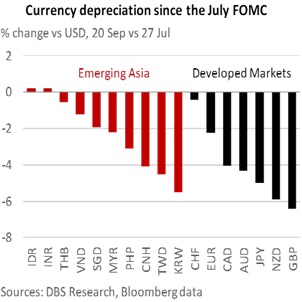

Most currencies depreciated after the July FOMC. For many, most of the losses were incurred after the Fed’s hawkish message at the Jackson Hole. DXY has appreciated 3.5% since 27 July to 110.18, near the year’s high earlier this month. GBP suffered the heaviest losses, plunging to its lowest level since 1985. The Bank of England’s 50 bps hike expected tomorrow will be less than today’s Fed hike. Conversely, EUR has been relatively stable around parity after Jackson Hole. The European Central Bank is closer to the Fed’s commitment to inflation in narrative and action; ECB delivered a 75 bps hike last Thursday and signalled that several more hikes are needed to bring rates to neutral.

Commodity currencies were pressured by fears that concerted jumbo rate hikes would hurt global demand for commodities. NZD is below 0.60 and closest to its 0.57 Covid low. AUD has been extending its fall below the 50% Fibonacci retracement level (0.6855), on its way to the 61.8% retracement level at 0.6590. CAD broke its 50% retracement level at 1.3273 this week; the 61.8% level is at 1.3565.

In Emerging Asia, the Northeast Asian currencies – KRW, TWD, and CNH – suffered most from the Fed’s readiness to sacrifice growth to control inflation. KRW was hurt by its rate differential turning negative against the US and the CNH from rate cuts in China. PHP and VND also hit new all-time lows after the previous FOMC. Record trade deficits also made KRW the weakest currency in Northeast Asia and the PHP in Southeast Asia. THB and MYR hit their weakest levels in 2006 and 1998 respectively. Although USD/SGD is above 1.40, its losses are well below the average of the currencies in its trade partners, making SGD one of the most resilient currency this year. Interestingly, IDR and INR were remarkably stable, supported at their psychological levels at 15000 and 80 respectively. Indonesia’s growth came in stronger-than-expected in 2Q22; consensus did not downgrade this year’s outlook. Consensus lifted India’s outlook after its solid double-digit growth in the June quarter.

Quote of the day

“If history repeats itself, and the unexpected always happens, how incapable must Man be of learning from experience.”

George Bernard Shaw

21 September in history

Singapore joined the United Nations in 1965.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.