Related insights_tr

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- UOB23 Apr 2024

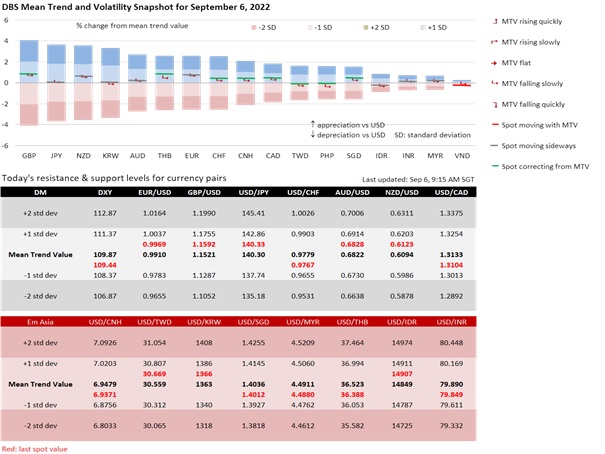

AUD depreciated 0.2% to 0.6797 ahead of today’s Reserve Bank of Australia meeting. We expect the RBA to lift the cash rate target a fourth time by 50 bps to 2.35%, close to its 2.50% neutral rate. However, markets are assessing if the RBA will slow the pace of hikes to 25 bps in October. The Greens, which control the balance of power in the Senate, want the RBA to pause ahead of the second Federal Budget announcement on 25 October. Although the Melbourne Institute’s inflation fell to 4.9% YoY in August from 5.4% in July, it has been underperforming CPI inflation.

RBA expects CPI inflation to keep rising from 6.1% YoY in 2Q22 to 7.75% YoY in December and returning to the top of the 2-3% target only in 2024. Starting 26 October, the Australian Bureau of Statistics will stop reporting inflation quarterly in favour of monthly releases. Taming inflation is a top priority of the Albanese government. In July, the Treasury launched a wide-ranging review of the RBA which was criticized for pushing out rate hikes to 2024 earlier. Like the Fed at Jackson Hole, the RBA will likely look past the housing market worries and focus on curbing demand to control inflation.

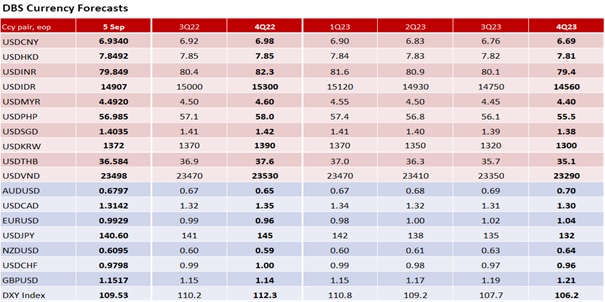

We have lowered our end-2022 forecast for AUD to 0.65 from 0.71. For the rest of this year, the Fed’s unapologetic readiness to control inflation at the expense of growth should keep the USD strong against the currencies of East Asia, Australia’s largest export destination. China, the country’s largest trading partner, is experiencing weaknesses in its economy and currency. Like other commodity-led currencies such as the CAD and NZD, AUD will not be immune to risk aversion.

DXY was flat at 109.5 during the US Labor Day holiday on Monday. Today, Bloomberg consensus expects the US ISM Services PMI to slow to 55.4 in August from 56.7. Pay attention to the prices paid sub-index – which dipped to a 17-month low of 72.3 in July – as a preview of the CPI inflation on 13 September. However, the Fed has already indicated that it will look past a second CPI slowdown and hike rates by 50-75 bps at the FOMC meeting on 21 September. On Wednesday, the Fed’s Beige Book and Fed Vice Chair Lael Brainard’s speech should reinforce the Fed’s hawkish message at the Jackson Hole Symposium. Expect a 75 bps Fed hike this month if the Bank of Canada hikes by 75 bps tomorrow. The BOC is known to parallel the Fed and will not want to be caught wrong-footed again. In June, BOC hiked 50 bps but Fed surprised with a 75 bps move. BOC compensated with a 100 bps increase in July vs the 75 bps Fed hike. Hence, we will not read much into this morning’s currency appreciation.

Quote of the day

“The hardest tumble a man can make is to fall over his own bluff.”

Ambrose Bierce

6 September in history

The first true supermarket, Piggly Wiggly, opened in Memphis, Tennessee in 1916.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- UOB23 Apr 2024

Related insights_tr

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- UOB23 Apr 2024