Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024

Investors are looking for today’s softer US CPI data to provide a relief rally. Consensus expects headline inflation to ease to 0.2% MoM in July from 1.3% in June and core inflation to slow to 0.5% from 0.7%. According to a New York Fed survey, falling gas, food and home prices drove consumer inflation expectations lower to 6.2% in July from 6.8% in June for the next year, and to 3.2% from 3.6% for the next three years. Brent crude oil prices have fallen below USD100 per barrel this month to levels at the start of the Russian-Ukraine crisis.

Lower US inflation expectations capped the US Treasury 10Y yield at 2.84% (100d MA). On the other hand, the 2Y yield is holding near 3.25% after last Friday’s stronger-than-expected US nonfarm payrolls and Fed Governor Michelle Bowman keeping the door open for a third 75 bps hike at the FOMC meeting on 21 September. Since March, the Fed has hiked 225 bps to 2.50% over four meetings. Our chief economist expects another 100 bps over the remaining three meetings this year and sees rates peaking at 3.50%, i.e., a 50 bps hike in September and a 25 bps hikes each in November and December.

Fears of a hard landing in the US economy have not gone away. The US yield curve, as per the 10Y-2Y differential, deepened to almost -50 bps, its worst since the tech recession in 2000. Poor guidance from chipmakers Micron Technology and Nvidia drove the Philadelphia Semiconductor Index or SOX down by 4.6% to below its 100-day moving average. However, the three major indices – Dow, S&P 500 and Nasdaq Composite – were still supported at their 100-day moving averages, hoping for a relief rally from the softer US CPI expected today.

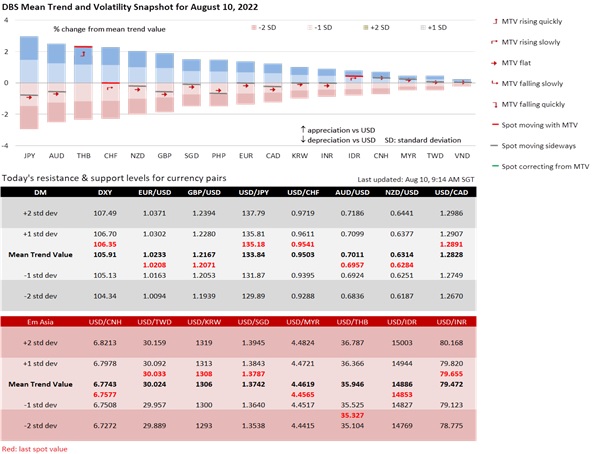

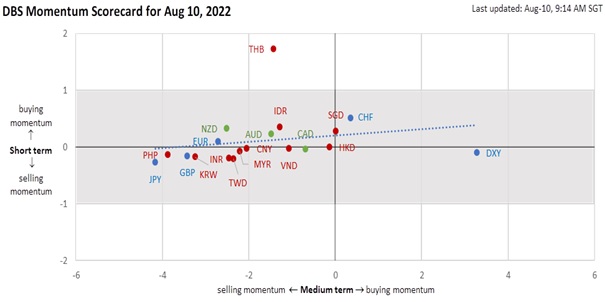

Not surprisingly, our model showed that momentum has flattened for many currencies. Most currencies bottomed after the US technical recession pulled back bets for outsized Fed hikes. Monetary policy has become more of convergence than divergence story after most central banks except Japan became as serious as the Fed in dealing with inflation. USD/JPY peaked at 139.40 and traded below 136 in August. After testing parity in mid-July, EUR/USD has recovered into a 1.01-1.03 range. Similarly, GBP/USD bottomed at 1.1760 and recovered to 1.20-1.23 this month. Commodity currencies are caught between risk appetite and weaker commodity prices. In August, AUD/USD fluctuated between 0.6870 and 0.7050, NZD/USD between 0.6210 and 0.6350, and USD/CAD between 1.2760 and 1.2810.

In Emerging Asia, the USD also peaked and consolidated. As fears of more outsized Fed hikes eased, hopes emerged for a soft landing. Over the past month, the Philippines, South Korea and India stepped up rate hikes to address inflation. Let’s see if Thailand delivers its first hike today. USD/SGD is trading between 1.3750 and 1.3850 this month after falling from 1.41 in the second half of July. USD/PHP peaked at 56.6 on 18 July and returned to a lower 55-56 range in late July. Similarly, USD/IDR fell to 14800-14950 this month after hovering around 15000 last month. After trading near 37 in late July, USD/THB fell below 36, with potential support around 34.8 (100d MA). Since mid-July, USD/MYR has been trading between 4.4470 and 4.4630, USD/CNY mostly between 6.73 and 6.77.

Quote of the day

“The EU is more resilient than we give it credit for. We always muddle through.”

Kersti Kaljulaid

10 August in history

The French monarchy was overthrown in 1972 with the imprisonment of King Louis XVI and his wife, Marie Antoinette.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024

Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024