Related insights_tr

Fed Chair Jerome Powell’s semi-annual congressional testimonies on monetary policy sank the US Treasury 10Y yield to 3.087%, its lowest close since 9 June. Powell’s unconditional commitment to restore price stability were eclipsed by his comment that a recession cannot be totally ruled out. Today, St Louis Fed President James Bullard should reiterate his view for the US labour market to stay robust and for the US economy to expand this year. Nonetheless, Fed officials were united in the goal to expeditiously return the Fed Funds Rate, currently at 1.75% after last week’s 75 bps hike, to the 2.5% neutral rate. Fed Governors Michelle Bowman and Christopher Waller favour achieving this with another 75 bps hike at the next FOMC meeting on 27 July. Today, let’s see if Bullard and St Francisco Fed President Mary Daly lean towards their position too.

Otherwise, US lawmakers were positioning for the US midterm election on 8 November. During Powell’s testimony, the Democrats were on the defensive from Republican rivals pushing to pin the blame of inflation on President Joe Biden’s massive stimulus. If a US recession materializes after the Democrats lose control of at least one house of Congress, the politicisation of inflation could hinder the fiscal responses to support the US economy before the US presidential election in 2024. The risk of US growth underperforming its peers again will harm the USD against its DXY components. US consumers could become more frustrated if they add jobs and owning a home to their frustration with elevated inflation.

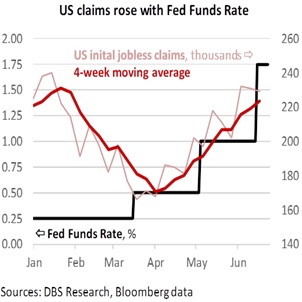

The focus is also on employment, the Fed’s other mandate. US initial jobless claims have risen after the Fed hike cycle started on 16 March. On a 4-week moving average basis, claims rose to 224k for the week ending 17 June after bottoming at 171k on 1 April. Consensus expects nonfarm payrolls (on 8 July) to drop to 303k in June from 390k in May. The Fed has already pencilled in a higher 3.7% unemployment rate of 3.7% in 4Q22 in last week’s Summary of Economic Projections. US Treasury Secretary Lawrence Summers reckons the jobless rate needs to rise above 5% for five years to contain inflation.

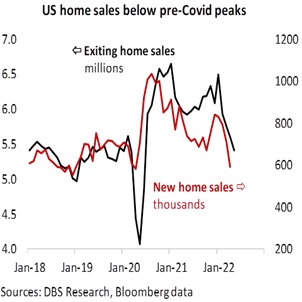

Today, US new home sales might also disappoint. After the whopping annualized 16.6% MoM drop in April, consensus reckoned new home sales would drop marginally to 590k in May from 591k in April. However, existing home sales fell for the consecutive month to 5.41 million units, its lowest level since July 2020. Americans are finding it harder to own homes because of the run-up in mortgage rates amidst record home prices. Worries will emerge if new home sales come in beneath the Covid low of 582k in April 2020.

Quote of the day

“I was the future once.”

David Cameron

24 June in history

British Prime Minister David Cameron resigned after the UK voted to the leave EU in the Brexit Referendum in 2016.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.