- .

- The RBI delivered a third consecutive 50bp hike, taking the repo rate to 5.9%

- GDP growth projection was trimmed to account for 2Q22 miss, inflation held unchanged

- We raise the end-year repo rate forecast

- Bond index inclusion plan might be delayed

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

A third consecutive 50bp rate hike

Decision

The Reserve Bank of India monetary policy committee (MPC) raised the repo rate by 50bp to 5.9%. This takes cumulative hikes in this cycle to 190bp and back to mid-2019 levels. The standing deposit facility (SDF) rate stands adjusted to 5.65% and the marginal standing facility (MSF) rate and the Bank Rate to 6.15%. The overall tone was balanced, as policy guidance remaining unchanged at ‘withdrawal of accommodation’, defying a minority expecting a shift to ‘neutral’ and suggesting that the hike cycle has some more room to go. The vote was a 5:1 split on the quantum of hike as well as on the stance.

Economic assessment

Reflecting the MPC’s views, Governor Das highlighted spillover risks from global developments, including geopolitics, aggressive rate hikes and financial market volatility. Domestically, the committee is more confident about growth than inflation, underpinning the hawkish bent.

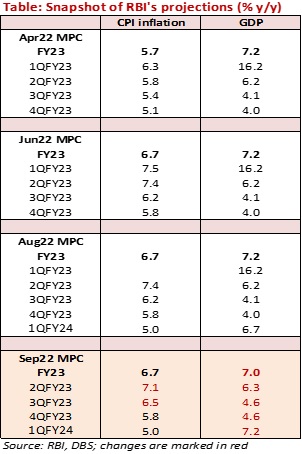

Factoring in the miss in 1QFY23 (2Q22) growth, full-year projection was trimmed to 7% from 7.2% earlier, but underlying momentum is expected to remain strong. Under aggregate supply, a) above normal rainfall and improving acreage; b) expanding industry and service sector activity; c) upbeat urban consumption on upcoming festivities and improving rural demand; d) gaining investment demand, bank credit besides rising non-oil non-gold imports which is seen as a proxy for private sector interests), but part of the gains is undone by softer outlook for exports.

Tone on inflation was cautious, even as slowing commodity prices provided some relief on imported price pressures. Fresh upside risks were cited from a) broadening out in food, especially cereal prices from wheat to rice in light of a fall in kharif paddy production; b) delayed withdrawal of monsoon and uneven spread which had driven up prices of perishables; c) adverse impact on inflation expectations; d) Indian basket crude oil price averaged ~US$ 104 per barrel in 1HFY23, which lent the RBI to retain its view that oil could average an elevated $100pb in 2HFY. The inflation forecast was kept unchanged at 6.7%.

Apr-Aug22 inflation has averaged 7.1% yoy and beyond a base-effect driven spurt in Sep22, we expect the headline to gradually moderate towards 5.5-5.7% by Mar23. Apr-Aug run-rate and our outlook for rest of the year prods us to adjust down our FY23 CPI inflation forecast to 6.6% from 6.8% earlier.

The central bank’s view on liquidity was also under close watch, after the banking system balance slipped into deficit on advance tax payments and forex outflows this month. This led banks to tap the MSF window and repo operations by the RBI to infuse liquidity. This mismatch was put to temporary factors, and liquidity enhancing measures were absent. In view of the moderation in surplus liquidity, the 28-day VRRR was merged with the fortnightly 14-day main auction.

While there is a likelihood that the squeeze on liquidity will prevail on upcoming festive demand and pick-up in credit growth, the central bank is of the view that seasonal pickup in government spending and drawdown of excess CRR and SLR from banks is expected to help in 2H. Variable repo operations look likely to be the preferred route rather than a permanent injection. At the same time, onus will be on banks to make deposit rates more attractive to better balance their liquidity needs. Rise in short-term (91-Day Tbill, commercial papers, certificate of deposits etc.) was also a fallout as the central bank prefers to keep the weighted average call rate (WACR) i.e., operating target of monetary policy close to the repo rate.

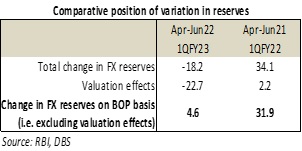

In light of depreciation pressures on the currency, the RBI reiterated that intervention efforts were only to curb excessive volatility ad anchor expectations. Favourable measures of FX reserve adequacy were cited (including short term external debt, net IIP, debt financing etc.) to highlight that the current stock was appropriate, and we concur. It was added that about 67% of the decline in reserves during the current financial year was due to valuation changes arising from an appreciating US dollar and higher US bond yields, rather than purely outright intervention.

Policy outlook

In response to the aggressive rate tightening cycle by the US Fed, regional central banks have stepped-up tightening efforts. The RBI MPC’s hawkish policy squares with shifting uncertainties, which leaves the door open for further hikes in rest of fiscal year.

Notwithstanding the modest cut in the full-year growth projection, commentary underscored the MPC’s confidence on recovery dynamics, which provides the elbow room to stay focused on price stability. We expect intervention efforts in the rupee to continue but stay opportunistic, and not directed at reversing the currency’s direction in midst of a broader dollar bull run. Markets has already priced in significant scale of policy tightening.

We expect the repo rate to be raised to 6.5% by end of the fiscal year (35bp in Dec22 and 25bp in Feb23), up from 6.25% earlier. Subject to the evolving US Fed view and domestic inflation trajectory, there is a risk that the next move might also be of a larger 50bp quantum (we assign a 40% probability).

Bond issuance for the 2H fiscal year trimmed

The government trimmed the bond borrowing program for 2H (Sep22-Mar23) of the fiscal year to INR 5.92trn, taking the full year total marginally lower to INR 14.21trn vs INR 14.31trn projected earlier. Besides INR 5.76trn in conventional bonds, the borrowing plan will also include the maiden INR160bn (~$2bn) sovereign green bonds. This tracks a push by other countries in the region, including Indonesia, and Singapore who have floated similar-natured government securities in the past, and likely to help India in setting a benchmark for such securities.

Index inclusion likely pushed back

In FTSE Russell's Country Classification Review Results released overnight, India has been retained on the watchlist for a potential upgrade to Market Accessibility Level ‘1’ and for consideration for inclusion in the FTSE Emerging Markets Government Bond Index (EMGBI). This marks a status quo since March 2021. In its press release, the index provider added that it was engaging actively with the index users as well as domestic market authorities regarding “ongoing market structure reforms, with a focus on securities that are available via the Fully Accessible Route channel”.

Expectations over inclusion of India’s government bonds in the JPM GBI-EM bond index had resurfaced recently (we discussed this here India: Optimism over bond index inclusion resurfaces). While little had materially changed on taxation, settlement rules, operational aspects, registration norms etc. since earlier in the year, a reweighting exercise in the JPM GBI EM index as well as signs that index providers had reached out to global investors/ fund houses to gauge interests, were behind the burst in expectations.

There are signs, however, that an announcement on this front might not be forthcoming this year. Reuters cited official sources saying that the debt index plan had been pushed back to next year, likely due to absence of ironing out in existing rules and restrictions. As we noted earlier, there is a broad acknowledgement by the authorities that an index inclusion carries strengths of diversification in the investor pool as well as introduction of more sticky foreign inflows. Nonetheless, wariness over distorting the level-playing field between domestic and foreign investors, has seen authorities maintain that notable change in the taxation regime – capital gains and withholding taxes on investments into debt securities – is unlikely. At the same time, the intention to allow provide rupee securities on the clearing platform, Euroclear is seen as a sufficient but not necessary pre-requisite for inclusion, mirroring the stance that China and Indonesia have taken. Delay in the inclusion plans saw bonds and rupee trim gains this week, with sombre risk sentiments and bid dollar likely to surface as dominant drivers of the markets price action.

Current account deficit widens in 2Q22

Apr-Jun22 (1QFY23/ 2Q22) current account deficit widened to -$23.9bn vs surplus of $6bn same time last year, marking the highest gap since 2013. As a % of GDP that amounted to -2.8% vs 0.9% last year and 1.5% previous quarter. The breakdown showed: a) bulk of the gap was due to significant widening of the merchandise trade deficit to $68.6bn from $30.7bn in 2Q21; b) net services receipts increased owing to higher computer and business service exports. Remittances also notched an increase of 22.6%. Net outgo on the income account, primarily reflecting payments of investment income, increased to $9.3bn vs $7.5bn. The financial account benefited from higher FDI inflows ($13.6bn vs $11.6bn in 2Q21), but portfolio outflows overwhelmed at -$14.6bn vs inflows of $0.4bn last year. Net ECBs witnessed outflows, likely due to adverse global rate movements, whilst non-resident deposits thinned. Overall BOP to the reserves fell to $4.6bn vs $31.9bn last year, diverging from the direction of reserves on valuation effects. Basic BOP deficit (current account + FDI) widened to -$15.9bn vs -$5.4bn in 2Q21.

For the year, current account math is in a soft spot. Encouragingly, monthly average exports have risen a strong 16% during Apr-Aug22 vs comparable period year ago, but was outpaced a sharp rise in commodity prices, particularly energy, has led to a 46% jump in average imports in the period. As a result, the trade deficit has more than doubled on average in the first five months of FY23. Factoring in the year-to-date run rate on trade deficit, the full-year goods trade deficit balance is expected to add up to -$300-$320bn vs FY22’s -$190bn. Service trade balance has maintained a strong trend and pulling overall invisibles and goods trade balance together, FY23 current account deficit is likely to top US$100bn, taking the balance to -3.7 to -3.9% of GDP from -1.2% year before.

To read the full report, click here to Download the PDF.

Topic

Explore more

E & S FlashThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024