- Credit markets face three macro headwinds in the post-pandemic environment

- A hawkish Fed is pushing spreads wider and may restrict refinancing access for HY credit

- Geopolitical risks remain a wild card, posing elevated uncertainty in Europe

- More fiscal scrutiny by debt investors could pose challenges for EM credit

- Asian USD credit spreads had been resilient, but volatility could rise

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Navigating post-pandemic markets

The pandemic may be over, but scars remain. Debt accumulated by sovereigns and corporates alike have not dissipated with the pandemic. Expansionary fiscal and monetary policy have lingering effects, contributing to elevated inflation across many economies. As such, they pose challenges to monetary and fiscal credibility, with profound implications for credit markets. Negative market reactions to the overtly hawkish Fed, as well as to the UK’s mini-budget last week, underscore these.

An unambiguously hawkish Fed

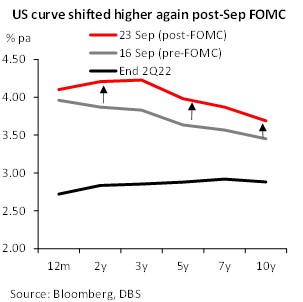

One of the most important post-pandemic shifts is the Fed’s policy stance. In its September FOMC meeting, the Fed gave its most hawkish policy guidance in recent memory. Not only were projections of the terminal rate revised higher to near 5%, but Powell’s tone had hardened significantly. He acknowledged for the first time that prospects of a soft landing are diminishing. This may be a tacit admission that inflation had become so entrenched that the Fed could be forced to stay on a tightening path even if growth slows significantly. Faced with a more hawkish Fed stance to restrict growth, US yields have repriced higher across the curve, and credit spreads have also widened across US markets.

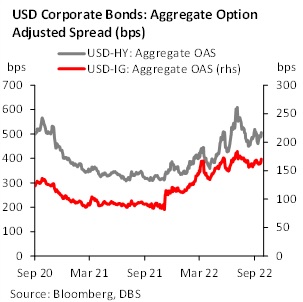

In rates, the US 2y, 5y, and 10y yields jumped by between 23-35 bps compared to the previous week. Credit assets were doubly hit by rising rates and higher spreads. The US IG and HY average OAS have widened by 6bps and 12bps respectively post-FOMC. For US IG bonds, spreads are now closing towards their July peaks, which mark a significant tightening of credit conditions given the large proportion of IG bonds in US credit.

Fed’s repercussions on global rates and credit

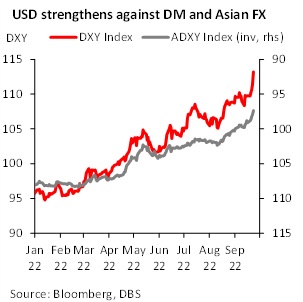

Given the size and hegemony of US capital markets, soaring US rates have spillovers beyond US borders, intensifying portfolio outflows and currency depreciation for the rest of the world. Post-FOMC, the USD has strengthened even more across the board, with the DXY index rising by 3.1% and Asian currencies (proxied by the ADXY index) falling by 1.8% for the week. The implications of rising rates and a rising USD on EM USD debt servicing are clearly negative.

To mitigate against sustained USD strength and capital outflows, global central banks are under pressure to partially track Fed policy, setting policy tighter than it would otherwise be. Consequently, a concerted wave of rate hikes across both DMs and EMs is now underway, and this global policy tightening trend will continue as long as the Fed pushes rates higher. Markets now expect the ECB and BOE to hike by over 230bps and 350bps respectively over the next 12 months while in Asia, RBI and BoK are also seen by markets to enact over 130bps of rate hikes.

Concerted global rate increases, a reversal of loose liquidity conditions, and a Fed-induced slowdown are set to raise volatility in credit markets. Geopolitics and supply chain disruptions add further to the cocktail of risks. Highly leveraged firms could enter a more difficult environment for refinancing, as soaring interest costs and a coming slowdown in revenues spur a repricing of default risks. This may mark a transition in regime from the previous period of low defaults backstopped by accommodative policy to a new regime with higher default risks due to restrictive policy.

European uncertainty amid Russian aggression

Beyond monetary policy shifts, geopolitical risks have also risen dramatically post-pandemic, with European credit being most exposed. On top of contending with ECB’s upsized rate hikes, European credit investors must also weigh ongoing developments in the Russia-Ukraine war.

Putin had upped the ante with a partial mobilization of 300k reservists, the initiation of referenda for occupied Ukrainian provinces to join Russia, and a thinly veiled threat to use nuclear weapons. Russia embarking on a game of chicken suggests that risks of further escalation are now more likely. There is also a risk of internal turmoil in Russia. For European industries, Russian belligerence raises risks given their dependence on long-term contracts for Russian supply of commodities including aluminium and nickel. The abrupt disruption of gas supply to Europe shows that such supply chain risks can no longer be ignored.

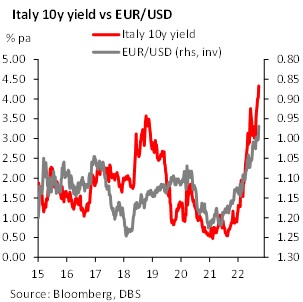

On top of Russia, political uncertainty also swirls in Italy. The country has elected a right-wing government led by the nationalistic Georgia Meloni, leader of Fratelli d’Italia. She had expressed a desire to re-negotiate with Brussels over Next Generation EU funding conditions. Anticipating post-election tensions, Italian-German bond spreads have widened back to 2020 levels, even with a new backstop by way of the ECB’s TPI (or Transmission Protection Instrument). A sharp Italian debt sell-off could reintroduce concerns over debt sustainability, weighing further on European credit.

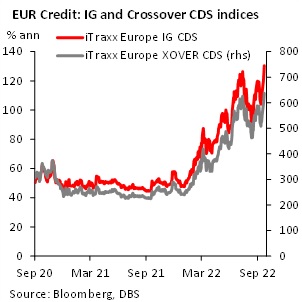

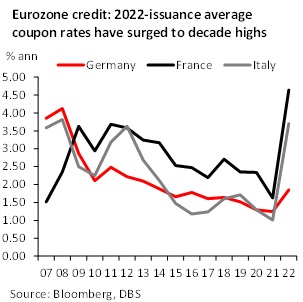

Amid these risks, European IG and Crossover CDS spreads have widened last week to 130bps and 637bps respectively, and now stand at their highest since early 2020. Spread levels do look attractive, given that historical European default rates had been below 2% since 2014. But prospective ECB rate hikes had already led to a surge in issuance costs to decade highs for French and Italian corporates. This could make refinancing increasingly difficult for zombie firms with earnings that are too low to service debt. Defaults are likely to pick up, and spreads may stay elevated for some time.

EMs’ fiscal trajectories face rising scrutiny

2022 has shown that monetary policy faces limits amid entrenched inflation. 2023 may well show that fiscal policy faces limits too from wary debt investors, as QE ends across most DMs. The recent sharp tumble in Gilts and GBP have shown how sensitive markets have become to blatant disregard for fiscal consolidation. The lesson is a sobering one: If a large, developed economy cannot hand-wave its fiscal responsibility, what are the chances that emerging economies are able to do so?

Possibly, sovereign debt investors’ scrutiny could increase amid elevated inflation and rising rates, posing a third risk for EM credit markets.

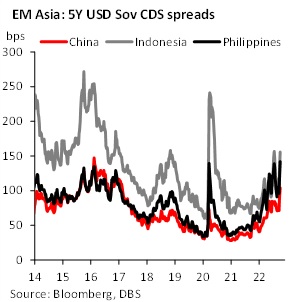

Sovereign 5y CDS spreads for Emerging Asia have been on a rising trend since the start of the year. This is driven by increased concerns of a China-led slowdown, and also fanned by rising US rates and the stronger USD. China and the Philippines have already seen CDS spreads exceeding their pandemic highs. For Indonesia, CDS spreads have been insulated by its strong commodity exports. However, softer commodity prices amid demand destruction could soon pose headwinds.

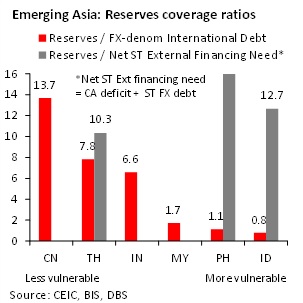

Rising USD rates and sovereign CDS spreads underscore the need to enhance fiscal credibility going forward for EM Asia. This is particularly so for Indonesia and Philippines, where FX debt have risen and the FX reserve coverage of such debt has fallen below 1.2 times, down from over 1.7 times in 2013. The silver lining is that much of this foreign currency debt has long-term maturity, so short-term external debt remains manageable.

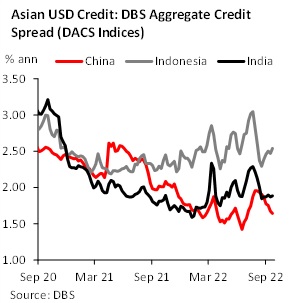

Asian USD credit stays resilient…

Even though USD rates and CDS spreads have risen this year, Asian USD credit have held up well. Our aggregate spread measures for Asian USD credit, the DACS indices, have mostly consolidated at around late 2021 levels.

China’s property credit distress had not resulted in any contagion for the rest of the Chinese credit market, given increased infrastructure stimulus and low non-property NPLs. Adequate policy space for fiscal and monetary support is one factor that is supporting China USD credit, even as most DM credit spreads widen. For India and Indonesia, USD credit spreads have shown more volatility amid USD strength and a hawkish Fed. Still, a recovery in domestic growth has also underpinned sentiment. However, a slowdown in regional growth may again trigger a widening in spreads.

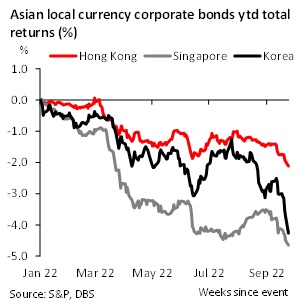

…but local currency credit sees divergence

Local currency credit showed a divergence in performance within Asia. For currencies where rates are more correlated to USD rates, such as the HKD, SGD, and KRW, their local currency corporate bonds have seen negative returns on a year-to-date basis that are between -2.1% to -4.6%. Carry is not sufficient to negate the negative hit from rising rates for such credit.

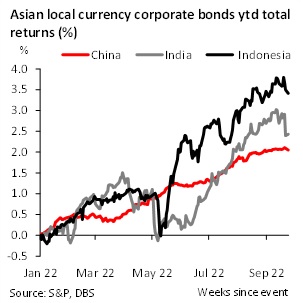

On the other hand, RMB, INR, and IDR local currency corporate bonds have registered year-to-date gains that range from 2.0% to 3.4%. China onshore RMB credit was helped by declining RMB rates, with the PBoC lowering its MLF and LPR rates to support growth. For INR and IDR credit, higher carry help to limit duration headwinds, while local rates also saw a smaller increase compared to USD rates. New defaults in 2022 are also almost negligible for India and Indonesia, supporting credit returns given their higher spreads compared to more developed Asian peers.

Watchful of policy-markets interplay

In conclusion, hawkish central banks, geopolitical tensions, and EM debt vulnerabilities are hurdles for credit markets to overcome. But this does not imply a finality to outcomes. Policymakers have room to calibrate polices and achieve a balance that will both reinforce credibility and limit distress for corporates amid post-pandemic headwinds.

To read the full report, click here to Download the PDF.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

GENERAL DISCLOSURE/DISCLAIMER (Credit)

This report is prepared by DBS Bank Ltd. This report is solely intended for the clients of DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd, its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBS Bank Ltd.

The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents (collectively, the “DBS Group”) have not conducted due diligence on any of the companies, verified any information or sources or taken into account any other factors which we may consider to be relevant or appropriate in preparing the research. Accordingly, we do not make any representation or warranty as to the accuracy, completeness or correctness of the research set out in this report. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate independent legal or financial advice. The DBS Group accepts no liability whatsoever for any direct, indirect and/or consequential loss (including any claims for loss of profit) arising from any use of and/or reliance upon this document and/or further communication given in relation to this document. This document is not to be construed as an offer or a solicitation of an offer to buy or sell any securities. The DBS Group, along with its affiliates and/or persons associated with any of them may from time to time have interests in the securities mentioned in this document. The DBS Group, may have positions in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking services for these companies.

Any valuations, opinions, estimates, forecasts, ratings or risk assessments herein constitutes a judgment as of the date of this report, and there can be no assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments. The information in this document is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed, it may not contain all material information concerning the company (or companies) referred to in this report and the DBS Group is under no obligation to update the information in this report.

This publication has not been reviewed or authorized by any regulatory authority in Singapore, Hong Kong or elsewhere. There is no planned schedule or frequency for updating research publication relating to any issuer.

The valuations, opinions, estimates, forecasts, ratings or risk assessments described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. It can be expected that one or more of the estimates on which the valuations, opinions, estimates, forecasts, ratings or risk assessments were based will not materialize or will vary significantly from actual results. Therefore, the inclusion of the valuations, opinions, estimates, forecasts, ratings or risk assessments described herein IS NOT TO BE RELIED UPON as a representation and/or warranty by the DBS Group (and/or any persons associated with the aforesaid entities), that:

(a) such valuations, opinions, estimates, forecasts, ratings or risk assessments or their underlying assumptions will be achieved, and

(b) there is any assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments stated therein.

Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets.

Any assumptions made in this report that refers to commodities, are for the purposes of making forecasts for the company (or companies) mentioned herein. They are not to be construed as recommendations to trade in the physical commodity or in the futures contract relating to the commodity referred to in this report.

Headwinds from a hawkish Fed and fiscal concerns September 28, 2022

Page 10

ANALYST CERTIFICATION

The research analyst(s) primarily responsible for the content of this research report, in part or in whole, certifies that the views about the companies and their securities expressed in this report accurately reflect his/her personal views. The analyst(s) also certifies that no part of his/her compensation was, is, or will be, directly or indirectly, related to specific recommendations or views expressed in the report. The research analyst (s) primarily responsible for the content of this research report, in part or in whole, certifies that he or his associate1 does not serve as an officer of the issuer or the new listing applicant (which includes in the case of a real estate investment trust, an officer of the management company of the real estate investment trust; and in the case of any other entity, an officer or its equivalent counterparty of the entity who is responsible for the management of the issuer or the new listing applicant) and the research analyst(s) primarily responsible for the content of this research report or his associate does not have financial interests2 in relation to an issuer or a new listing applicant that the analyst reviews. DBS Group has procedures in place to eliminate, avoid and manage any potential conflicts of interests that may arise in connection with the production of research reports. The research analyst(s) responsible for this report operates as part of a separate and independent team to the investment banking function of the DBS Group and procedures are in place to ensure that confidential information held by either the research or investment banking function is handled appropriately. There is no direct link of DBS Group's compensation to any specific investment banking function of the DBS Group.

1 An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

2 Financial interest is defined as interests that are commonly known financial interest, such as investment in the securities in respect of an issuer or a new listing applicant, or financial accommodation arrangement between the issuer or the new listing applicant and the firm or analysis. This term does not include commercial lending conducted at arm's length, or investments in any collective investment scheme other than an issuer or new listing applicant notwithstanding the fact that the scheme has investments in securities in respect of an issuer or a new listing applicant.

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024