- The RBI delivers a back-to-back 50bp hike, taking the repo rate back to its pre-Covid level

- GDP and inflation forecasts were held unchanged

- Growth resilience provides room to maintain a hawkish bent

- Liquidity conditions have tightened, just as credit growth cycle takes off

- We take stock of the southwest monsoon

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024

For the full report with charts, tables and illustrations, please download the pdf file

RBI frontloads rate hikes

Decision

The Reserve Bank of India monetary policy committee (MPC) voted unanimously for a second back-to-back 50bp hike, taking the repo rate to 5.4%, back to Oct19 levels. This leaves the Standing Deposit Facility (SDF) rate at 5.15%, with the Marginal Standing Facility/ Bank rate at 5.65%. Policy guidance reiterated the stance in June, which was to stay “focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth”. The rate move, in essence, takes the policy out of emergency mode and to more normalised levels. The scale of hike was unanimous, with one member expressing reservations on the policy guidance.

Economic assessment

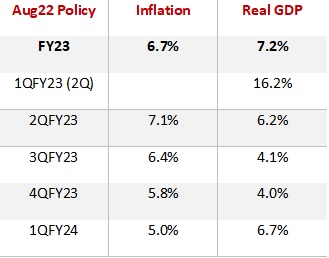

The central bank was sanguine on this year’s growth prospects, saying that recovery was broadening out, with the policy focus squarely on inflation. To back optimism on growth, indicators such as: a) consumer durables output, passenger traffic, and sale of passenger vehicles were a backstop for urban demand, but rural indicators were mixed; b) services sector was turning a corner; c) pick up in capacity utilisation in the manufacturing sector, now back above its long-run average, was viewed as a signal of better investment activity, besides PMIs and higher capital goods output, were highlighted. The FY23 growth forecast was maintained at 7.2% yoy (DBSf 7.0%) – see table for quarterly breakdown – with 1QFY24 (2Q23) pegged at 6.7% yoy.

The tone of inflation assessment was cautious emphasizing the ‘unacceptable’ and uncomfortable prevailing levels, as the Governor highlighted the risk that sustained high inflation could destabilise inflation expectations and harm growth in the medium term. While the recent correction in commodity prices was acknowledged, policymakers see considerable uncertainty on the policy horizon, even as the global demand outlook was weakening. Risks cited were: a) weak rupee adding to imported inflation pressures; b) shortfall in paddy sowing due to an uneven monsoon (we discuss this in detail in the next section); c) remnant pass through of higher costs by producers. Building in an assumption of a normal monsoon and average crude oil price (Indian basket) of $105bp, the FY23 inflation projection was retained at 6.7%. with 1QFY24 (2Q23) inflation pegged at 5%, suggesting a return to the 4% inflation target is distant.

RBI projections

Source: RBI, DBS

Outlook

Marking a departure from practise, the central bank also discussed the health of the external balances in the policy statement but maintained that the scale of rupee depreciation was much more contained than the regional peers and selected reserve currencies (see our note).

On policy, the central bank reinforced its emphasis on price stability by a back-to-back 50bp hike, to prevent sustained high inflation from unhinging inflationary expectations and hurting medium-term growth. Resilience in growth indicators also provided the headroom to retain a hawkish bias as the central bank is focused on dialling back the previously held accommodative stance. Considering Friday’s move takes the repo rate back to 3Q19 levels, the tightening move has unwound the accommodative rate moves undertaken during the pandemic and thereby prevailing levels are unlikely to disrupt the post-pandemic growth path significantly.

Policy guidance highlighted it was premature to go easy on the inflation fight as the trajectory is beholden to fluid global commodity cycle, remnant passthrough pressures from high input costs and recent rupee depreciation will might lower the net beneficial impact of softer imported pressures.

In our view, this necessitates the monetary policy committee to continue to incrementally tighten policy in rest of FY23. We maintain our call for at least another 75bp hikes by Mar23, subject to inflation nearing its peak in 3Q22 (2QFY23) and gradually easing below 6% in the Mar23 quarter.

Tighter liquidity conditions, deposit growth lags credit demand

Domestic liquidity has tightened in recent weeks, with the banking system surplus down at INR2trn. Put differently, average daily absorptions under the Liquidity Adjustment Facility (LAF) (both SDF and variable rate reverse repo auctions), eased to INR 3.8trn in Jun-Jul22 from INR 6.7trn in Apr-May, with reduction in the surplus put to tax and capital outflows, which had pushed up money market rates past the repo rate. Backing the RBI’s stated stance that liquidity moves will be two-way, a variable rate repo auction was conducted worth INR 500bn in late-July, to alleviate stress on cash conditions.

Concurrently, the gap between credit and deposit growth continues to widen. July loan growth rose 14% yoy, as compared to the sub-9% pace in deposits, with the resultant spread at over 550bp. This has raised concerns that a slow deposit growth might stymie lenders’ ability to meet credit demand, just as the cycle takes off. While the transmission to banks’ interest rates, has hastened with the introduction of external benchmark-based pricing of loans in October 2019, deposit rates are yet to be repriced actively.

Part of this divergence is down to: a) discretion of banks; b) higher transmission of repo rate hikes onto lending rates, as loans are increasingly shifting to external benchmarks; b) CRR hike earlier in the year contributed to the liquidity tightness. This growing divergence is likely to necessitate a repricing in deposit rates in the coming weeks, with a start witnessed in increase in term rates in recent weeks.

Crucial southwest monsoon

India’s mid-year southwest monsoon plays an important role in determining the health of the summer (kharif) crop, which makes up half of the annual food grain output. The sector employs half of the economy’s workforce and accounted for 18% of GDP in FY21.

In its June projection, the India Meteorological Department (IMD) forecasted rainfall to be at 103% of the long period average (LPA), which stoked expectations of a third consecutive bumper kharif crop this season. This follows two years of surplus rainfall followed by a small shortfall in 2021.

How are things shaping up yet far?

June to September witness bulk of the precipitation. Monsoon had a slow start to the year but caught momentum in July, turning a deficit to a surplus late last month.

As of August 3, the southwest monsoon was 6% higher than the LPA, with the pace improving after a slow start, even as the spread is uneven. Central India and South peninsula are 11% and 33% > LPA, Northwest a small surplus of +2% whilst East/ Northeast (-14%) experiences a shortfall. Besides strength of the rainfall, its spatial and geographical spread will also influence the crop sowing trends.

Catch-up in rains has prompted an increase in area brought under sowing activity but lost momentum in the second half of July.

As of 29 July, total area sown is marginally lower than comparable period last year, with acreage differing abouts various crop groups. Sowing lags in rice but is faring well in pulses, cereals, and oilseeds. Area under rice/paddy was 13% below last year’s, due to poor rains in the central and eastern belts i.e., UP, Bihar, Jharkhand, Odisha etc. Coarse grains, cotton, sugarcane, and pulses are broadly on track.

Mid-year southwest monsoons are crucial for India’s farm sector, especially the kharif crop as well as remnant impact for the rabi (winter) crop owing to reservoir levels and moisture content in the soil.

Encouragingly, prevailing levels of water in the country’s 143 reservoirs is at 57% of its total live storage capacity, which amounts to 119% of the live storage of corresponding period of last year and 139% of storage of average of last ten years. Secondly, resilience to rainfall shortages has improved compared to the 90s as gross irrigated area as % of cropped area has risen to over 50%, compared to below 35% in early-90s. That said, access to irrigation is not uniform across states.

For inflation, a normal monsoon will help keep a lid on food inflation in the coming months, however, a sharp correction is unlikely. Prices of agri inputs i.e., fertilisers, animal feed, fuel etc. have risen sharply, putting a floor below prices of farm produce. Separately, a RBI study shows that the correlation between the precipitation index and components of food inflation was highest in vegetables, which could surface in the short-term or with a lag. The impact on non-perishable cereals was lower given the option of buffer stocks/ supply management systems that are often put in place.

Here too few concerns have surfaced. A heatwave earlier in the year hurt wheat output, resulting in lower stocks with the centre amidst tight global supply. This suggests that the usual fallback option of either releasing buffer stocks to tame prices or stepped-up imports might be insufficient to fully offset supply shortfall in selected foodgrains. Meanwhile, market players have already started to factor in a potential shortfall in the paddy crop, pushing up wholesale prices. A silver lining is that the central pool has ample stocks of rice i.e., 134% of buffer and strategic stock requirements[1] as of early-July. A sharper shortfall in kharif sowing activity may, however, impact the trend adversely. Rice has a weightage of 4.8% in the CPI inflation basket (0.4ppt under public distribution scheme and 4.4ppt by other sources) and wheat has 2.8% (0.2ppt and 2.6ppt respectively).

On a broader note, climate change-led changes in weather patterns – ranging from heatwaves to drought or excess rainfall, pose fresh risks to the farm sector output and productivity.

To read the full report, click here to Download the PDF.

Topic

Explore more

E & S FlashThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024