- Service sector reopening is expected to benefit Singapore

- China’s 3Q trend confirms the worst is behind the economy, but Covid path will be key

- Base effects will result in choppy readings in India, ….

- … while Indonesia benefits from positive terms of trade

- Key issues for 2H: commodity cycle direction, geopolitics, peak in US inflation, Fed rate hikes

Related insights_tr

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- HKD rates: HIBOR downtrend to ease 19 Apr 2024

Commentary: GDP Nowcasts –Diverging paths

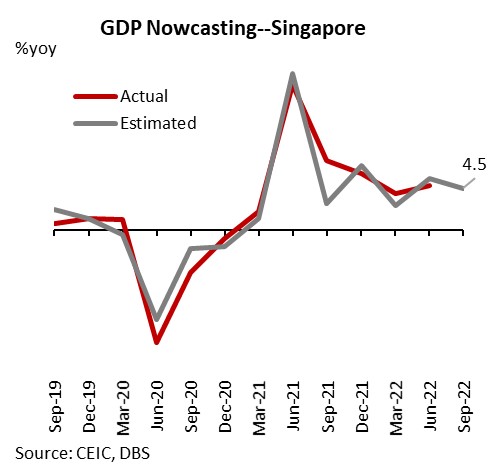

Updates to our proprietary GDP Nowcast models for Singapore, China, India, and Indonesia put the economies on divergent paths into mid-2022.

Singapore’s advance estimates for 2Q22 released earlier, ticked up to 4.8%yoy, but registered zero growth on sequential basis, likely due to spillover from a slowdown in China and tightening financial conditions. Our model points to a modest pullback in 3Q, with improving tourist arrivals and higher residential transactions providing relief to the service sector but offset by slowing retail sales and real credit growth.

China’s 3Q GDP Nowcast projection confirms the view that the worst is behind the economy. Most of the sub-indicators – industrial production, fixed asset investments, retail sales etc. – notched a modest rise from lows into 3Q but trend thereafter will be largely beholden to the evolving domestic pandemic situation. Rising unemployment, property market stress and a fading export boom will also limit the extent of buoyance in 2H22.

India’s growth path over the 2Q22 (1QFY23) and 3Q will be choppy, due to base effects. Headline growth will be in double-digits in 2Q, boosted by service sector reopening, higher exports, freight, and credit activity. Household real purchasing power is set to moderate on sticky inflation, via high food/ fuel costs and lower labour participation rate. 3Q growth will show a reverse-V, edging back towards the mid-6% handle.

Indonesia’s 2Q-3Q trend is likely to benefit from reopening boost, with activity unscathed by rising Covid cases this quarter. Favourable terms of trade due to high commodity prices has lent a significant boost to the external sector, with trickle down benefit to demand. Easier financial conditions and extension in energy subsidies has shielded household purchasing power, even as high food, unsubsidized fuel adjustments and VAT increase bite at the margin. Bank Indonesia continues to bide time, exhibited little urgency to join global and regional peers in tightening policy, as domestic considerations are given a higher weightage in the policy mix.

To read the full report, click here to Download the PDF.

Ma Tieying 馬鐵英, CFA

Senior Economist - Japan, South Korea, & Taiwan 經濟學家 - 日本, 南韓及台灣

[email protected]

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- HKD rates: HIBOR downtrend to ease 19 Apr 2024

Related insights_tr

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- HKD rates: HIBOR downtrend to ease 19 Apr 2024