- Recent developments favour a shift to a more constructive view of European credit

- European credit losses are nearing levels seen in the Eurozone Crisis, so risks are well-priced

- Energy security has been enhanced by a broadening pivot towards coal-fired power generation

- Periphery debt risks are also curbed with the ECB making clear its intent to limit fragmentation

- Policy-led developments should support an upturn in European IG and Crossover credit

Related insights_tr

Economic risks in Europe had undeniably risen after the outbreak of war in Ukraine, which had led to sanctions, supply chain disruptions, and a surge in energy prices. While we held a negative outlook on European credit due to such worries in the immediate days after conflict broke out (see DBS Flash: Assessing the impact from Russian sanctions, 3 Mar 2022), we are now starting to see developments that should support a more constructive view on European HY credit.

First, losses in European Crossover credit indices since February are already approaching losses seen in the depth of the 2011 Eurozone debt crisis, when Portugal joined Greece and Ireland in receiving a bailout. Any Eurozone slowdown with moderately high inflation should still be less damaging to real corporate debt burdens compared to the 2011-2012 debt crisis episode. Second, we have also seen pragmatic turns in energy policy across several European countries this week. This should effectively negate tail risks stemming from any Russia-imposed constriction of gas supply, and prevent a further escalation in power costs. Last but not least, the ECB has now explicitly acknowledged the importance of circumscribing fragmentation in Eurozone debt markets. As such, risks of extreme peripheral spread widening should be contained. The current widening of European corporate HY spreads could thus be nearing an end, with carry now providing a sizeable buffer against the more uncertain growth outlook.

Slowdown risks are priced in vs previous crises

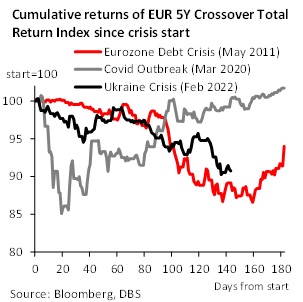

To understand if European credit markets have adequately priced in slowdown risks, we benchmark the cumulative return of the EUR 5Y Crossover CDS total return index against its performance during the Eurozone Debt Crisis in 2011, and the pandemic outbreak in 2020.

The EUR Crossover CDS index’s loss since Feb 22 has already touched 9%. This is larger than the 6% loss over 6M experienced in the Eurozone debt crisis (while the pandemic produced a 6M gain). The index’s current loss is also not too far from the maximum loss of 13.4% and 14.9% in the two earlier crises. Such large percentage losses were quite fleeting previously, persisting for less than 20 days. The CDS index sell-off in 2012 was also unusually extreme for a technical non-economic reason. There was a forced unwind of large CDS positions by a major US bank, which further exacerbated short-term market volatility. Assuming a similar credit loss experience as previous crises, we think the current widening in European CDS looks mature, and a turnaround could happen if developments become less negative.

Energy security is improving on policy shifts

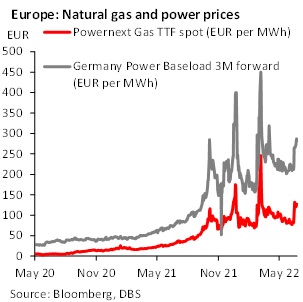

One positive development might be policy shifts that limit tail risks of spiralling energy costs. Europe’s dependence on Russian natural gas had grown in recent years, as environmental concerns led to a phasing out of coal generation capacity in favour of natural gas. Another feature is that the EU internal market for electricity sets the price of power to be equivalent to marginal cost. Marginal cost is set by the more expensive natural gas, even though coal provides a larger contribution to European power generation.

Following Russia’s incursion of Ukraine in February, tensions have only risen, with Russia having cut off gas deliveries to Poland, Bulgaria, Finland, the Netherlands, and Denmark. With alternative gas supply being difficult to source and expensive, the consequence of such Russian supply cuts is that both natural gas and power prices have doubled from their 2021 levels. The more elevated prices are and the longer they stay unchecked, the greater the risk it poses for European industry.

Now, European policy is starting to pivot away from Russian gas towards coal. While setting electricity prices to equal marginal cost is economically Pareto-optimal, having this price held hostage by Russian gas policy is the opposite of optimal. This week, Germany, Italy, the Netherlands, and Austria have all announced that they are preparing to resurrect/delay the retirement of old coal plants, or lift production caps on coal plants.

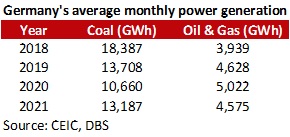

For Germany, Economics and Climate Minister Habeck has confirmed that Berlin will return 4.3GW of hard-coal capacity and 1.9GW of lignite capacity that are held in reserves, assuming parliamentary approval is granted in July. Another 2.6GW of hard-coal capacity that was scheduled for closure will also be returned to the market. Assuming that the newly added reserve coal plants are utilized at 60% capacity, they could add an additional 2700GWh per month of power generation. This is enough to offset a 60% reduction in Germany’s oil and gas power generation, based on 2021 average monthly production of 4500GWh. Italy, Europe’s second largest gas importer, has also struck deals to diversify its supply of natural gas.

What would be the impact on power prices? Gas is still likely to remain the marginal cost driver of power costs without falling demand, but there is now increased capacity to insure against surprise gas disruptions, minimising risks of an excessive surge in gas and power prices. A sustained easing of electricity prices will require a further increase in global coal supply and generating capacity across Europe, which is challenging to attain but not impossible with further policy shifts.

Of course, it is regrettable that Europe is returning to greater coal dependence. Still, there is a trade-off to be managed between short-term economic and energy security versus long-term climate security. Importantly, Germany has maintained that it remains committed to phasing out coal completely by 2030. Europe’s policy pivot is quite simply to buy time for energy transition plans to be redrawn, given the watershed change in geopolitics, and the need for a sustained economic response to military coercion of a functional democracy.

ECB support arrests periphery spread widening

Another risk for European credit lies in the periphery sovereign debt, with the ECB ending asset purchases and preparing to raise rates in Q3. Dominating market concerns is the sharp rise in 10Y Italian BTP yields towards 4%, and a resultant large 200bps spread over the 10Y German Bund. In response, Italian financial credit has seen a sharp sell-off, as markets fret over the sovereign-banks nexus of risks again.

With Italian sovereign debt to GDP sitting at 150% of GDP, if average interest cost rise to 3.50% slowly as new debt replaces old debt, this could result in a 5.8% financing deficit-to-GDP, and lead to market questioning of debt sustainability. On a headline basis, Italy’s sovereign debt-to-GDP ratio is unquestionably higher relative to levels in 2011. But the real question is not whether Italy’s debt is vulnerable, but whether the ECB and European policymakers could and would take necessary steps to provide support, even as monetary policy is tightened.

To answer this question, it is important to recognise that much has changed in Europe since the 2011 debt crisis, and mostly for the better. The introduction of the European Stability Mechanism (ESM) in 2012 means that funds are readily available for bond purchases and financial assistance to European states. While there is still no fiscal union, partial debt mutualization has been achieved in 2020, with EUR750bn of joint debt to be used for funding a pandemic recovery package. Thus, fiscal resources are ample and usable for interventions today, unlike in 2011.

As for Italy in particular, the political environment has also improved compared to 2011. Italy is now led by a highly competent technocratic PM, ex-ECB President Draghi. The country’s political configuration is also at its most stable in years, with Draghi enjoying broad support from both left-wing and right-wing parties alike. As such, the outlook for structural reforms in Italy looks more concrete than under Berlusconi back in 2011, even if debt-to-GDP ratios are higher. EU support is ultimately a political decision, and Italy under PM Draghi is quite likely to enjoy the confidence of both EU leaders and ECB policymakers.

Indeed, a pre-emptive action by the ECB has already taken place, with an ad-hoc policy meeting held on 15 June to pledge action against resurgent fragmentation risks. It is an acknowledgment of concerns over the rising spreads of peripheral bonds, and also an affirmation of policy intent to tackle it. Given limited guidance beyond flexible reinvestments of the maturing PEPP portfolio, markets are still unsure if ECB triggers for bond market interventions could be too strict. Nevertheless, the ECB has unofficially drawn a cap on periphery spreads, and it is unlikely for spreads to widen back to mid-June levels without a deterioration in either geopolitical or economic circumstances.

To speculate on a possible support mechanism, we may draw on the experience of late 2011. LTROs could be circumscribed to banks located in the peripheral economies that are facing wider than justifiable spreads. Such operations are aligned with the ECB’s mandate to limit fragmentation in credit markets and improve policy transmission. Favourable regulatory and collateral treatment for sovereign bonds should incentivise banks to accumulate peripheral bonds with wide spreads using the additional liquidity, helping to reduce fragmentation.

Banking on an upturn

Given elevated spreads for slowdown risks in European credit, improving energy security, and a highly supportive ECB towards peripheral bonds, European credit looks to offer an attractive risk-reward. European IG and Crossover credit may see an upturn, given the meaningful policy shifts that have now occurred.

To read the full report, click here to Download the PDF.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

Explore more

E & S FlashThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.