- To counter high inflation, India’s government has undertaken relief measures

- A combination of export halt, duty concessions and excise cuts are being applied

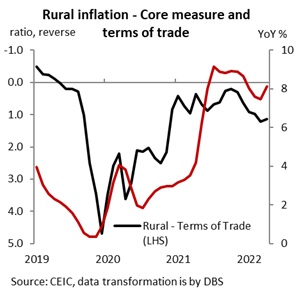

- Rural inflation terms-of-trade is under pressure

- These steps temper upside risks to our FY23 inflation projection

- The RBI- policy committee is likely to stay on the rate hike path

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- DBS Stock Pulse: Singapore Equity Picks – Scaling back further on REITs 18 Apr 2024

- ASEAN-6: Are the tourists back?17 Apr 2024

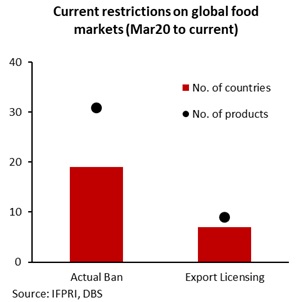

Amidst inflationary concerns globally and food security assuming priority, several countries have taken measures to ensure sufficient domestic stockpiles to help contain prices, and lower hardship amongst the populace. Globally, since the Ukraine crisis, about 16.9% of the share of global trade impacted (by calories) has faced some extent of food export restrictions, higher than in wake of the pandemic as well as 2007-08 crisis. Since Mar20, about 19 countries have imposed an actual ban, whilst seven have imposed export licensing (see chart), according to data from International Food Policy Research Institute.

On India’s end, owing to April CPI inflation hitting an eight-year high and WPI inflation rising by double digits for 13 consecutive months, the central government announced measures to tame inflation. We assess few recent steps and discuss its implications.

Government initiates inflation control steps

- Fuel tax cuts, good for inflation, but with fiscal costs

To partly offset the impact of high global energy commodities, the government announced few steps:

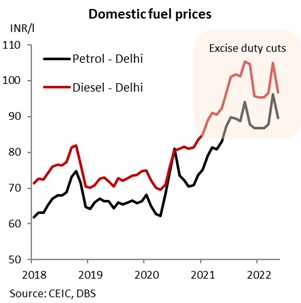

- Excise duties cut on petrol and diesel by INR 8/l and INR 6/l respectively, which the government estimates will lower final prices by INR9.5/l and INR7/l. The ~7-8% decline in retail prices will potentially lower inflation by 0.2-0.3% and is likely to reflect in June’s reading rather than May. Annual fiscal revenue loss will amount to INR1trn; building in the cut that was already built in FY23 Budgeted estimates and pro-rated for rest of FY, impact will be around INR700bn i.e., 0.3% of GDP, for rest of FY23). The centre called on the states to also lower the VAT rate to provide further relief on end prices

- Subsidy of INR 200/ LPG cylinder for residents under the cooking gas scheme for women under the poverty line. Total connections released under the PMUY scheme stood at 91.7mn this month

- Allocations to fertilizer subsidy will rise by INR1.1trn, on top of the budgeted INR1.05trn

- Import duty on coal slashed to 0%, besides on raw materials & intermediaries such as for plastic products, inputs of iron and steel, coking coal etc. have been cut to augment domestic supply. Concurrently export duty on iron ore, pig iron etc. has been raised

This fuel tax cut along with reductions in November 2021 effectively unwinds tax hikes undertaken between Mar20 to May20, which had taken centre’s excise tax to record highs. Steps over the weekend will carry a salutary 0.2-0.3% (direct and indirect) impact in the near-term (petrol has 2.2% and diesel 0.2% weightage in the CPI basket) and is likely to reflect from June CPI onwards.

If states follow with tax cuts, cumulative impact will be bigger. Maharashtra, Odisha, Rajasthan, and Kerala also lowered their ad-valorem tax rates, as of last evening. As a counter, we also note that any price adjustments by oil marketing companies (to clear under-recoveries as retail fuel prices have not been fully adjusted to reflect global prices) and further climb in global oil, might negate part of the impact of these tax reductions.

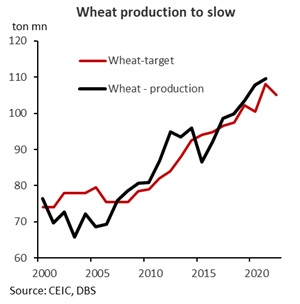

- Ban of wheat exports

India imposed an immediate ban (13 May) on wheat exports, triggered by a fall in production estimates as the standing crop was hurt by the ongoing heatwave, dubbed as early summer in states like Punjab, UP, Haryana.

Domestically, the initial production estimate of FY22 wheat at 111.32mmt was lowered to 105mmt, and lower than 109.6mmt n FY21.

According to the USDA, India was the eighth biggest exporter of wheat in the world, with shipments of 10mn tons in 20-21, compared to Russia (33mn) and EU (31mn). Ban in wheat exports boosted international prices at the margin, but a bigger role was played by geopolitical risks, and pockets of adverse weather as well as high energy prices.

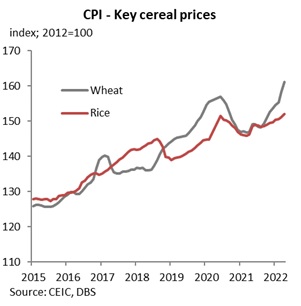

This ban is intended to calm domestic inflation (wheat has 2.56% weightage in the CPI basket) on higher local supply, although the salutary impact might be temporary. Wheat inflation has been rising on sequential and yoy terms for the past six months. Lower procurement of wheat supplies might increase demand for alternatives as rice, stoking cereal inflation. While this ban is indefinite, we note that India had imposed such a ban on wheat and non-basmati rice last in 2007 and 2008 respectively, to curb high domestic inflation and subsequently lifted it in 2011, but subject to pre-conditions.

- Others

Add to this, more measures are in the offing:

a) Sugar (1.13% weight in the CPI basket) exports will be added to the ‘restricted’ category from Jun22, and the ban will remain in place till Oct22. This move is intended to supplement domestic stocks and ensure price stability during the upcoming sugar season FY22 (Oct-Sep);

b) To combat a surge in prices of edible oil (refined oil i.e., sunflower, soyabean, saffola, etc. has a weight of 1.3% in the CPI basket) and disrupted palm oil availability, customs duty on imports of 2MMT each of crude soyabean oil & crude sunflower oil per year for two years has been lowered to 0%;

c) earlier in the year, import duty on lentils was cut to 0% for Australia and Canada, besides lowering duty on purchases from the US to 22% from 30% before. Cess on crude palm oil was also trimmed back in Feb22

These relief measures will partly offset the spillover of imported pressures and cap domestic prices, with a 10% drop in prices across few of these commodities to translate into a cumulative 0.5-0.6% impact on inflation. This lowers the scope of further upward adjustments to our FY23 inflation forecast of 6.4% yoy, as will watch developments closely. Persistent price pressures in essential segments for which demand is routinely inelastic i.e., food and fuel, could spur second round effects and entrench inflationary expectations.

Rural terms-of-trade mix

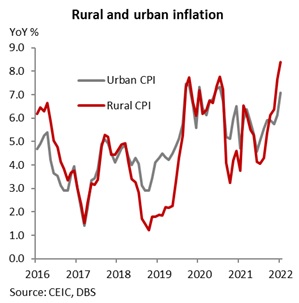

While aggregate inflation has been high, under the hood, rise in rural inflation has outpaced its urban counterpart.

The wedge likely reflects differing weight of sub-components in the inflation basket for instance, food has a higher weightage of 54% in the rural basket, but 36% for urban, while there is no housing component in the rural CPI. But the bigger reason for the divergence likely lies in the fuel component (7.9% weight in rural and 5.6% in urban) based on consumption patterns and the increasingly market-linked pricing of fossil fuels, kerosene and diesel, which offset routinely subdued price pressures in traditional fuel items like firewood and chips and dung cakes (RBI bulletin). While rising petrol/ diesel impinge on purchasing power in urban centres, electricity/ power tariff adjustments come with a considerable lag.

Better returns on food (especially rural-farm) is outweighed by high/ sticky non-food inflation, putting the rural terms of trade under pressure.

Agri input prices are also on the rise – by way of higher diesel, feedstock costs and fertilisers, paving the way for a higher minimum support price for upcoming crop seasons. High inflation has also had a dampening impact on real rural wage growth, with strength of upcoming southwest monsoon – spatial and geographical spread – under close watch.

Implications on the fiscal math

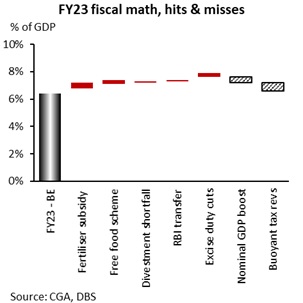

Few of these inflation relief measures carry fiscal costs. Recent developments point to an increase in spending demands, which is likely to narrow the revenue-side cushion.

Budgeted FY23 expenditure faces upside risks from additional subsidies i.e., higher food subsidy outlay on the food grain distribution scheme which stands extended till Sep23 (0.3% of GDP), and fertilizer to offset a sharp rise in farm input costs (0.4%). Under revenues, divestment run-rate is running at a weaker-than-budgeted pace i.e., assuming shortfall by a third (0.1% of GDP), lower RBI divided transfer (0.1%) and the weekend’s excise duty cuts (pro-rated for rest of FY23 at 0.3%).

While these additional spending requirements add up to a little over 1.1% of GDP, there are few offsets: by way of a higher nominal GDP assumption (+0.3%) and likelihood of higher tax revenues/buoyancy (+0.5-0.6%). Netting off the two ends, budgeted math will still require reprioritization in existing spending heads. Press reports suggest that expenditure might rise by another INR1trn (0.4% of GDP) on higher subsidy, extension of free food scheme and need to offset rising agri input prices. We expect the FY23 target to rise to -6.6% of GDP vs budgeted -6.4%, but narrower than -6.9% in FY22. Gross borrowing program for the year at INR14.3trn is unlikely to increased, with INR8.45trn due to be raised by Sep22 (first half FY). Any shortfall, according to government sources cited by the press might be met by tapping into the Consolidated Fund.

Unlikely to deter a hawkish RBI MPC

These announcements are unlikely to materially derail the RBI’s hike path. As highlighted in Minutes from the RBI’s intermeeting hike in May, the first goalpost would be to take the current 4.4% benchmark repo rate back to the pre-pandemic level of 5.15% by a 50bp hike in June and followed by +25bp in August (our base case). Next, is to narrow the prevailing negative real rates to neutral vs the 12month forward-looking inflation. Hence, we see the repo rate heading to 5.65% by end-2022.

The rupee is hovering at the middle of the Asia ex Japan pack vs the dollar, supported by sizeable foreign reserves stock (despite the 8% drop from record high; partly influenced by base effects) and net long RBI’s forward FX book of $65.7bn (Mar22), with more than 90% under the 1Y maturity bucket.

In face of financial market volatility, the central bank’s inclination is to curb volatility in the FX movements but not fight the trend, especially if depreciation pressures stem from a stronger dollar and is impacting the AXJ block. To that extent, foreign reserves are being put to their intended use.

Authorities will play a balancing act, as the cash reserve ratio hike, intervention to support the INR and FX swaps, are intended to soak liquidity, which in turn opens the door for open market operations to contain yields, without jeopardising the inflation outlook. In other words, dollar sales to neutralize one-sided depreciation in the currency will also create the legroom for liquidity-neutral open market operations. With bond supply likely to remain high in FY23, need for open market operation is back to the fore, as the borrowings demand-supply mismatch is likely to keep yields buoyant towards 7.6%.

To read the full report, click here to Download the PDF.

Topic

Explore more

E & S FocusThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- DBS Stock Pulse: Singapore Equity Picks – Scaling back further on REITs 18 Apr 2024

- ASEAN-6: Are the tourists back?17 Apr 2024

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- DBS Stock Pulse: Singapore Equity Picks – Scaling back further on REITs 18 Apr 2024

- ASEAN-6: Are the tourists back?17 Apr 2024