- Bank Indonesia left the benchmark policy interest rate unchanged

- Pace of incremental hikes in the reserve requirement ratio will be hastened

- Authorities have room to bide time as a higher subsidy budget contains imminent inflationary risks

- Implications for forecasts: We retain our expectation for moderate rate hikes from 3Q

- ….to preserve attractiveness of local bonds and rupiah in the face of a hawkish US Fed

Related insights_tr

Bank Indonesia on hold

Decision: Bank Indonesia left the key benchmark rate unchanged at 3.5% on May 24, matching consensus and our forecast, and defying expectations of a small minority backing a hike. Instead, the authorities resorted to the well-telegraphed increase in the reserve requirement ratio (RRR), which stands to rise to 6% in Jun22, 7.5% in Jul and 9% in Sep for conventional lenders, faster than the pace announced in Jan22 (RRR was to rise to 6.5% by Sep22), to absorb liquidity in a non-disruptive fashion. The reserve ratio hike will potentially withdraw IDR110trn ($7.5bn) of liquidity from the banking system, in addition to IDR200trn in the first round of the RRR hike. Banks will be provided with part relief on the scale of RRR increase upon fulfilling preset lending requirements to priority sectors.

Economic assessment: Key economic assumptions were held unchanged including growth at 4.5-5.3% for the year, and current account deficit at -0.5-1.3% of GDP. 2022 inflation is seen at slightly higher than 4% but expected to return to the 2-4% range by 2023. BI plans to coordinate measures with the government to manage inflation, noting the favorable impact of a higher subsidy budget on inflation. Commentary struck a cautious note on global growth, inflation, financial conditions, and spillover risks by way of slowing flows to EM countries. BI expects US Fed to hike by 250bp in 2022 and 50bp in 2023. This was accompanied by expectations of resilience in domestic recovery, loan pick-up (Apr’s 9.1%yoy, fastest since mid-2019) and limited rupiah depreciation compared to regional currencies.

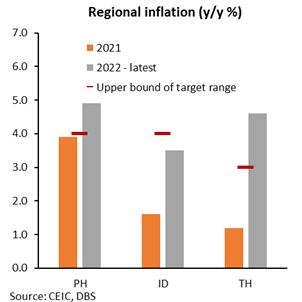

Outlook: The central bank’s monthly survey points to May inflation remaining elevated at 3.53% yoy (+0.38% mom) vs Apr’s 3.5%, driven by higher air fares, food (vegetables, protein sources including egg and meat) and pass through of non-subsidized fuel costs. While this is likely to underpin the inflation trend, the government’s recent decision to increase the subsidy budget (details below) and by extension, contain energy costs, partly dampens pipeline risks to the price trajectory. Add to this was the decision to lift the ban on palm oil, capping cooking oil prices.

Concurrently, rupiah depreciation has been less than regional peers, which lowered the urgency for Bank Indonesia to normalise policy, despite hawkish overtures by counterparts i.e., Malaysia and Philippines in recent sessions. Notably, inflation was high in the latter two countries, breaching the target in Philippines in the latest reading.

Signs of an imminent shift towards hikes was largely absent, premised on expectations that inflationary risks might briefly rise but return to trend thereafter and market conditions were not disruptive to the currency’s direction.

BI meets next in the third week of June, ahead of which the US Fed would have delivered its second consecutive 50bp hike, totaling +100bp in 2Q22. The domestic price trend is also likely to stay exposed to the vagaries of imported price pressures, price distortions in food commodities and pass through of higher input costs by producers, besides demand restoration. With inflation likely to stay sticky in the higher end of the BI target range, soft rupiah, and favourable growth dynamics, we expect a gradual shift towards hikes to begin in 3Q22 to preserve the attractiveness of local bonds and currency in the face of a hawkish US Fed hike cycle.

Subsidy rationalization vs fiscal costs

Rising global energy prices had spurred calls for a rationalization in Indonesia’s fuel subsidies and reduction in price controls (Indonesia: Fuel prices, subsidies, and inflation – balancing act).

Dousing expectations of price hikes in fuel subsidies, the Finance Ministry raised allocation towards subsidies last week. This underscores wariness over piling additional pressure on consumers’ purchasing power and to cap inflationary concerns. Total expenditure for 2022 was revised up to an estimated IDR 3106trn, up IDR 392bn from the earlier projection. This increase factors in a 56% jump in energy subsidies to IDR 208.9trn i.e., 0.4% of GDP jump. Add to this, compensation to state-owned oil company PT Pertamina and state utility PT Perusahaan Listrik Negara will also surge to IDR 293.5trn. Plans to raise power tariffs for consumers who use 3,000V and higher is under consideration.

Detrimental impact on the fiscal math is partly negated by a projected 2.3% of GDP boost from revenues from natural resources. State revenue assumption has, accordingly, been revised up to IDR 2226trn vs IDR 1846trn estimated earlier. Other changes in budgeted numbers include a) oil price adjusted to $95-$105/bl vs $63/bl before; b) yield of the benchmark 10Y seen higher at 6.85%-8.42% this year and USDIDR at 14,300-14,700.

Netting off the two, 2022 fiscal deficit is expected to widen to -4.5% of GDP vs -4.0% indicative and -4.9% budgeted target. Deferment in the decision to lower subsidies and hence, retaining administered prices will delay projected consolidation towards -3.0% of GDP deficit limit in 2023. Capped domestic fuel prices provide more headroom to Bank Indonesia to keep rates unchanged in the near-term, yet the currency is likely to stay under pressure from widening ID-US rate differentials and a bid greenback.

Palm oil ban eases, but hurdles remain

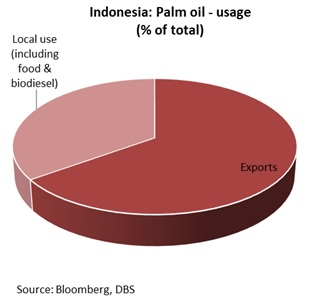

The Indonesian government revoked the ban on palm oil exports, which has been place since April 28, replacing that with domestic sales quota for cooking oil. This is intended to backstop local supplies and cap prices, after local farmers protested the measure on rising surplus stocks. Indonesia accounts for over 60% of global production.

Domestically, a third of the output is consumed by way of the food sector, biodiesel etc., whilst the rest are exported. With the sector being amongst the best export earners for the economy, distortions in the trade policy might affect this year’s trade surplus buffer.

Hinging on commodities, current account to register a small surplus this year

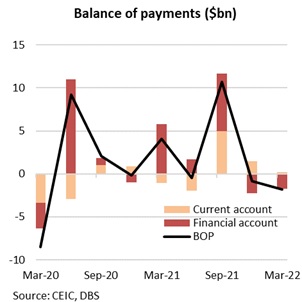

1Q22 current account (CA) registered a small surplus of $0.2mn (0.07% of GDP) vs $1.5bn (0.5%) in 4Q21. While the goods trade surplus was steady at $11.1bn vs 2021 quarterly average of $10.9bn, an increase in services account deficit on account of outbound travel, including religious/ pilgrimage travel as well as lower remittances contributed to the smaller CA surplus. On the other end, even as direct investment flows held up, portfolio outflows continued for a second consecutive quarter, albeit slowing from 4Q21.

Mar22 balance of payments deficit widened to -$1.8bn, more than doubling from quarter before. Q2 math is likely to witness a softer financial account, whilst commodity-led export gains support the goods trade balance. The temporary palm oil export ban is likely to hurt May’s trade balance, with its cessation to bode well for June. In all, we still hold out for a small CA surplus this year, of around 0.4% of GDP. Risks to this view stem from a potential pullback in commodity prices and/ moves to curb shipments of key commodity segments to keep local prices in check.

To read the full report, click here to Download the PDF.

Topic

Explore more

E & S FlashThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.