- Real GDP growth rose 5% yoy on higher consumption and positive net exports

- April CPI inflation rose 3.5% yoy, close to our forecast

- Resilient growth provides room to prioritise inflation

- Markets opened on the backfoot on catch-up action after a weeklong break

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024

Steady growth

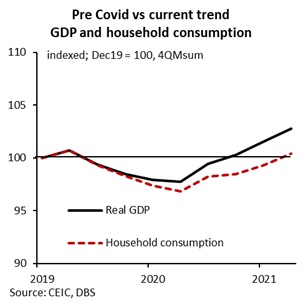

Indonesia’s economy expanded 5%yoy in 1Q22, vs 5% in 4Q21, partly propped by base effects. Real GDP growth had averaged 3.7% in 2021. On sequential basis, output contracted -1% nsa qoq vs 1.1% in the prior quarter. Headline growth (four quarter moving sum) has surpassed pre-pandemic levels, with household consumption also a shade higher.

Breakdown

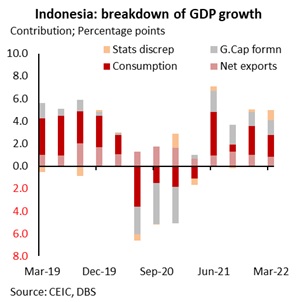

Under the hood, private consumption rose 4.3%yoy vs 3.6% in 4Q21, whilst government consumption shrank -7.7% vs +5.2% quarter before, slowing overall contribution of final consumption to headline growth – added 1.9ppt vs 2.5ppt in 4Q. Notwithstanding sequential deceleration due to temporary mobility restrictions in the first quarter, softer inflation, accommodative monetary conditions as well as benefits of a better faring trade, were supportive of demand.

Under investments, growth in fixed capital formation slowed but segments such as buildings & structures, as well as machines & equipment expanded on the year. Goods export and import growth slowed on the year, partly impacted by the temporary ban on key export item i.e. coal, but contribution of net exports held ground on terms of trade gains from higher commodity shipments.

Statistical discrepancy also added an one-off 0.9ppt to the headline and is likely to be adjusted down in subsqeunt readings.

Outlook

With a strong start to the year, growth is likely to average within the government and central bank’s forecasted range. A sharp fall in the Covid caseload has led to unwinding in local restrictions and removal of quarantine requirements for tourists. High frequency indicators like mobility, PMIs, confidence surveys, motorcycle sales etc., are in recovery mode. Government expenditure moderated in 1Q22 vs same quarter year ago, with a bigger subsidy outlay in 2022 likely to require reprioritization in spending heads.

Resilient demand on broader reopening, improving vaccination rates, open tourism borders and strong trade performance (non-oil commodities), will be key pillars of support. Our read of the ban on palm oil exports is that it is likely to be a temporary measure (~1-2months) until domestic prices correct, after which shipments could resume (less than a third of production is consumed locally). We maintain our GDP growth forecast of 4.8% yoy for the year, within BI’s projected range of 4.5-5.3%. Risks stem from a sharp moderation in global growth outlook, particularly as China faces growth headwinds from the punitive zero-covid strategy as well as US Fed adopts an aggressive policy tightening path.

Inflation top-of-mind risk

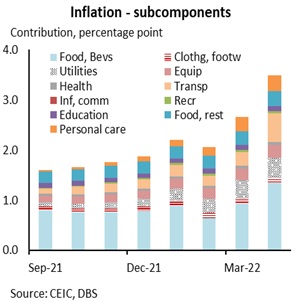

April inflation quickened to 3.5% yoy to levels last seen in 4Q17 vs 2.6% month before. Core inflation also rose to a two-year high of 2.6% vs 2.4% in Mar. This firm reading was a function of festive-led demand (Ramadan) as well as supply-side forces, including an increase in the value added tax rate and hikes in non-subsidised fuel/ gas products. Over 90% of the increase in headline CPI was on higher food and transportation costs, as shown in the chart below.

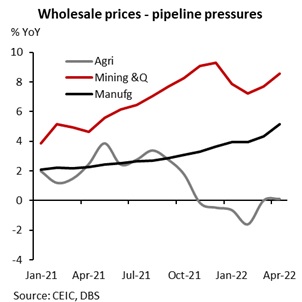

There are ample pipeline pressures as reflected by the WPI inflation trend, with mining and quarrying along with manufacturing product inflation to feed through completely to the retail channels.

In our note - Bank Indonesia stays on hold; we see inflation risks - we highlighted several risks to the price trajectory. Direction for inflation this year, to a large extent, hinges on the longevity of price controls and subsidies. Partial pass-through to domestic retail prices as well as second order effects and demand normalisation after the pandemic abates, will be key to the trajectory.

Implications for policy and markets

A strong growth print provides the headroom to policymakers to monitor price stability risks and financial markets amongst tightening global conditions. Bank Indonesia had emphasized earlier that it will look through first order effects of adjustments in subsidized fuel, instead react to structural inflationary pressures. Core inflation is also a key gauge under watch, which accelerated to a two-high in April. The BI might resort to another reserve requirement rate hike, before shifting its guidance and raising the benchmark rate. A hawkish shift in guidance in the second half is likely as core inflation strengthens further and domestic assets come under pressure from weak risk-uptake, even if partly mitigated by a strong trade account. Cumulative 75bp of hikes is likely this year. This compares to expectations that the US Fed may raise rates by another 175bps by end-22, according to our house view, besides quantitative tightening of their balance sheet.

Domestic financial markets were under pressure on Monday, as they reopened by a weeklong break. 10Y IDR yield (generic) jumped more than 25bp to above 7.25%. This comes after yields have maintained a steady upward beat this year, from 6.4% at the start of the year. 2Y rates have risen by more than 120bp YTD to 5.35% this month. The rupiah has faced some pressure off-late but is still amongst the better faring currencies in the region, down -2.0% YTD vs US$ compared to Taiwan Dollar -6.9% and Korean Won –6.7%.

To read the full report, click here to Download the PDF.

Topic

Explore more

E & S FlashThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024

Related insights_tr

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024