- Internationalisation of the Chinese currency is slated to follow an unconventional path.

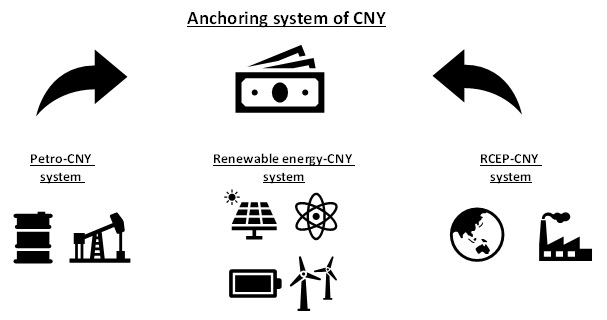

- We outline 3 anchoring pillars: (1) Petro-CNY, (2) Renewable Energy-CNY, and (3) RCEP-CNY.

- In short, this is a PRET anchoring system.

- P stands for Petro, RE for Renewable Energy, and T for trade within RCEP.

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Building up the Anchoring Foundation for RMB internationalisation

Is there sufficient investment demand for RMB dovetailing to full capital account liberalisation? Many argue that it is not in the interest of Beijing to give up control of capital flows. But China’s plan, in our view, is to build an alternate RMB based system coexisting with the present USD system at her own pace with respect to the suitability/viability of political institutions. It is important to understand (1) the design of the scheme at the geo-strategic level; and (2) the anchoring plan of the RMB at the execution level.

The Grand Scheme

The wealth of China in the past two decades stemmed from accession to the WTO, pursuing relentless exports excellence, which resulted in persistent current account surpluses, intervention in the currency market, which subsequently resulted in sizeable accumulation of foreign reserves. Such proceeds allowed Beijing to write off the debts of Bank of China and China Construction Bank before getting them listed publicly. Accumulation of trade surplus over time also led to RMB appreciation for 10 consecutive years, which in turn ramped up domestic property prices and charged up wealth. Per capital income advanced rapidly.

The leadership acknowledges the merits of globalisation and reiterates strong commitment to free trade. As of end last year, foreigners owned USD3.6trn in direct investments and USD2.2trn in portfolio investments in China. Also, according to the Financial Stability board, four out of the world’s “most systematically important” banks are Chinese.

China is keen to build an alternate system for her own economic benefits and risk diversification purpose, particularly the hedge against geopolitical risks. The presence of such system does not preclude her participation in the existing system.

Execution of the CNY Anchoring Plan

China understands well the benefits of anchoring RMB to real commodities, as ongoing economic development needs resources; adoption of such anchor aligns ideologically with the prevailing thesis of “Common Prosperity”, which discourages spending beyond the means and encourages even income distribution.

We think that the RMB would eventually anchor to commodities/physical goods for diversification purposes: (1) Petro-RMB system with Russia/Saudi Arabia and OPEC, (2) Renewable energy-RMB system with Latin America, and (3) RCEP-RMB system in Asia. Establishment of each building bloc aims at creating local demand for RMB over time based on mutually beneficial terms.

Petro-CNY System

China is the world’s largest net oil importer. In 2021, 25% of oil export from Saudi Arabia went to China; Saudi Arabia now tops as China’s number one oil exporter. Should some of these trades be denominated in CNY? It is driven primarily by change of international relations and the need to diversify risks. China is investing in military system, nuclear plants, and smart cities in Saudi Arabia. If this ground-breaking agenda eventually develops, it will facilitate RMB internationalisation.

Such possibility was remote four years ago, but the ongoing development of Russia-Ukraine war probably aggravated growing impetus to diversify the concentration risk of USD in Russia and China’s reserves to hedge against geopolitical risks.

Russia is attempting to accept only Ruble for oil/natural gas transaction settlements, thereby effectively anchoring the currency to real commodities. Given the heavy oil/gas dependence of EU on Russia alongside absence of Ruble in EU, they may need to purchase Ruble from the Russian central bank. Last week, the Russia announced cutting gas supply to Poland if the payment is not being settled in Ruble. Gas price surged 20% accordingly and the USD/RUB saw a rebound.

Shares of Russia’s exports (inflow) and imports (outflow) settled by currencies other than RUB, USD, and EUR increased from 1.7% and 2.2% in 2013 to 7.1% and 27.1% in 2021 respectively. Although share of EUR is rising for Russia’s export settlement, China and Russia will increase the usage of RMB moving forward given the EU’s imposition of various sanctions over Russia.

Enlargement of the PETRO-CNY system will take time. 80% of Saudi Arabia’s oil transactions are settled in USD and the respective local currency, riyal, is also pegged to the USD. However, the proactiveness of the Saudi Arabia participating in this system is a strategic step forward for China. The natural forces to speed up the development of an alternate system is substantial. China will likely leverage on prevailing geopolitical climate to sharpen the strategic focus and execute logistics orderly.

Renewable Energy-CNY System

The next building bloc is around Latin America. The strategy here is to boost local demand for RMB, but China must firstly invest in real economies that are deemed beneficial to the long-term betterment of her partners. As investments pour in, alongside imports of tools from China for these mega projects, it creates the condition for persuading local governments to settle some of them in RMB.

As part of the Belt and Road Initiative (BRI), China has diversified its investments in energy markets in Latin America, increasingly in renewable energy on top of oil/gas and copper/coal/uranium. China has spent more than USD244bn on energy projects worldwide since 2000, a quarter of that in Latin America. Just for Argentina alone, China invested some USD5.7bn in energy projects including nuclear, wind farm and hydroelectric dams in Argentina since 2000. More than 15% of Chinese investment went to renewables between 2000 and 2020. Large hydropower projects such as the Cóndor Cliff and Barrancosa dams financed by the China Development Bank (CDB) in Argentina, the planned Rosita hydropower project in Bolivia, financed by the Export–Import Bank of China (Exim) are key examples.

As far as solar energy is concerned, the EXIM bank financed Cauchari Solar Park in Jujuy Province of Argentina at a low funding cost of 3%, (one of the largest solar farms in the world) with 1.2 million solar panels and total costs amounting to USD551mn. These panels are all imported from China, with companies such as Huawei helps turning power from solar panels into useable current. ZTE also supplied fiber optic telecommunications systems and surveillance cameras for the solar project. These types of engagement boost China’s manufacturing exports of photovoltaic equipment, wind turbines, lithium-ion batteries, advanced low-carbon technologies, and equipment for geothermal power plants.

Chinese companies are also constructing and developing renewable energy projects. China Three Gorges, a state-owned power company, has expanded its footprint in the construction of hydropower projects in Bolivia, Ecuador, and Peru. Likewise, the Power Construction Corporation has a significant presence developing and constructing hydropower and non-conventional renewable projects from Cuba to Chile. In Central and South America, PowerChina has 57 projects under construction, with a prevailing value of around USD10bn.

China also plays a pivotal role in the extraction and refinement of lithium in Argentina, which accounts for 16% of global output and 9% of global reserves. The Lithium Triangle of Argentina, Bolivia, and Chile, which collectively makes up more than half of the world’s lithium, is crucial element for batteries production especially for electrical vehicles and military applications. Elsewhere, Beijing also invested roughly USD4.5bn in lithium production in Mexico.

Given renewable energy resources in most Latin American countries are in remote areas, it requires lengthening extension of electricity transmission lines. Hence, China’s investment in Latin America also extends into the distribution of electricity by acquiring local companies. In Brazil, State Grid Corp of China supplies electricity to more than 10 million homes. Argentina also announced in February China would finance about USD24bn in electricity related infrastructure projects.

This lays a strong foundation for China to persuade Latin America over time to use RMB for settlement of importing manufacturing items for these mega renewable projects. If participating countries could benefit holistically as time goes by, Beijing should then proceed persuading them to accept RMB for local investment purposes.

There are historical legacies complicating the agenda despite tremendous investment inflow and deepening trade integration: (1) some Latin American currencies are indexed to the USD due to hyper-inflationary experiences of the past, (2) companies handling commodity exports (including agricultural commodities) have strong ties to the US and settled in USD.

China would focus on renewable energy related transactions be settled in RMB as they are tied up with real investment pouring into the local economy. The eventual success of this path also hinges on China’s willingness to permit debt roll-over, when needed. If this strategy is successful, the RMB could anchor to renewable energy.

RCEP-CNY system

China has already started prompting the RCEP bloc to use RMB for settlements. In spite of China’s geographical proximity to most fellow members, the challenges are also the most daunting because: (1) Japan, Korea, New Zealand and Australia have strong relationship with the US; (2) Japan also wants to promote the use of Japanese yen as settlement currency; (3) there are territory disputes between China and some ASEAN countries in South China Sea. At this juncture, the best strategy thus is to focus on deepening trade integration with RCEP members.

The overall strategy is to let local governments to develop their own strategies with top-down guidance and support from central government. The common goals amongst provinces are:

(1) to focus on increasing merchandise trade especially goods in electronics and agriculture. For example, Yunnan in agricultural products, Shananxi in parts for auto and planes, and Fujian in engineering machinery and ships/boats etc. For Guangdong, agricultural exports to / imports from RCEP members accounted for 24% and 34% of total exports / imports with RCEP countries respectively. They are encouraged to utilise RCEP rules-of-origin provisions to gain tariff reductions. For 1Q, imports from RCEP countries through Huangpu Custom saved RMB8.11mn tariff

(2) Enterprises are encouraged to import more ICs and semiconductors from Japan to replace imports from the US and the EU. 88% of China products heading to Japan under RCEP will be subject to zero tariff.

(3) Local governments are encouraged to set up industrial parks in RCEP countries to drive more cooperation platforms to create stable regional supply value chain. For instance, Guangxi will upgrade twin parks in China and Malaysia, and build new park in Vietnam.

(4) Provinces are encouraged to provide a range of supporting services covering protection of intellectual property rights and establishments of dispute resolution mechanisms.

The central government shall then provide more benefits to attract investment from Japan and South Korea in high-technology areas. Beijing will probably stand firm behind provincial plans to build twin industrial parks alongside RCEP themed expo/summit. The goal is to effectively leverage RCEP platform to create higher inter-dependence amongst members especially for Japan and Korea given their relative importance in high end electronics supply chain. On the other hand, ASEAN has already surpassed EU and US as China’s biggest trade partner. As trade volume grows between China and fellow members, especially when they start building up trade surplus, it would then be easier for Beijing to lobby RMB settlement in a gradual manner.

Indonesia is a good starting point. China and Indonesia started the LCS – Local Currency Settlement since 3Q last year. During China’s coal shortage in 4Q21, Indonesian coal was the major substitute of imports of Australia and the LCS was commenced in such perfect timing.

Conclusions

The world should not underestimate the progress of RMB internationalisation. China has done considerable groundwork and momentum is progressing to her favour given the Russo-Ukrainian war game-changed the prevailing geopolitical climate. In order to safeguard such positive momentum, China will likely emphasize more on inclusive economic benefits with partners particularly within the RCEP bloc to build firmer trust. Investment grandeur must find way to filter through the system to cradle local specialists and improve communications with local governments. One of the key successful elements of China in Latin America is the strategy of engaging local governments involvement right at the beginning in energy projects endorsed by the head of state. This will improve project sustainability. Next is to improve the accountability of protecting the local environment and to distribute investments/loan assistance more evenly amongst members.

The execution of anchoring RMB is a big feat. The three prime building blocs are all here: (1) Petro-CNY amongst oil exporting countries, (2) Alternative Energy-CNY in Latin America, and (3) RCEP-CNY in Asia. Thus, the CNY will always anchor to real commodity in the future. This is consistent with the common prosperity thesis to prevent over expansion of capital.

Maximising survival span is more important than amassing wealth in an uneven manner for China. Constructing an alternate monetary system using RMB as settlement currency is thus essential. Before that happen, a well-executed anchoring plan for CNY substantiates the very foundation of this new system.

To read the full report, click here to Download the PDF.

To unsubscribe, please clickhere.

Topic

Explore more

E & S FlashThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024