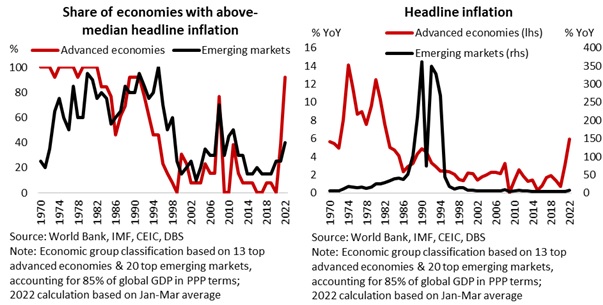

- The sharp spike is felt in a higher share of Advanced Economies vs Emerging Markets

- Global commodity prices are a key inflation driver, with bigger spikes from past oil supply shocks

- US and Europe inflation is higher than Asia due to weaker China and more stimulative policies

- Inflation worries rachet up Fed rate hikes

- Asia vigilant on inflation risks but lag normalisation due to growth balance

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Inflation has made a fast comeback from the subdued environment over the past couple of years. It is also proving to be more persistent and worrisome than the initial expectations of both policy makers and markets. The sharp inflation spike is most felt by Advanced Economies (AE) vs Emerging Markets (EM). AE central banks’ monetary policy rhetoric has thus switched significantly to extreme hawkishness and tightening in 2022 from peak dovishness during the pandemic.

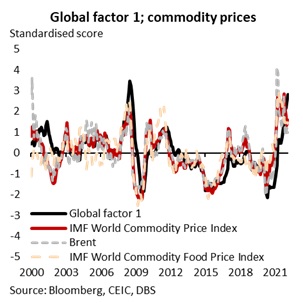

Global factors play an important role in driving inflation across economies. Our analysis shows that the variation in global inflation was primarily driven by two key global factors, based on our Principal Component Analysis (PCA) of headline inflation in the top 33 global economies from the year 2000 onwards (For more details, see ASEAN-5: Evaluating key inflation drivers). They explained 51% of the variance in headline inflation in the full cross-country sample. While the two factors are statistical constructs, we can link them to economic variables, which theory suggest may drive inflation.

We found that the first global factor fitted well with the movement of global commodity prices. It had a correlation of 0.67 with world commodity prices, 0.58 with Brent, and 0.54 with world food prices.

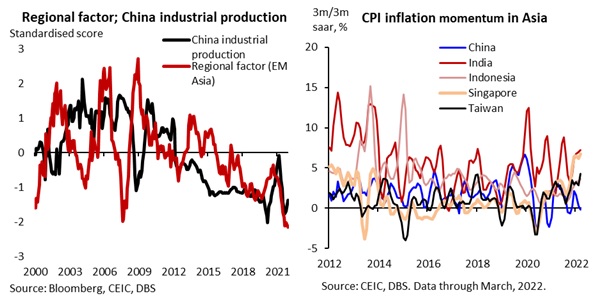

To also decipher the relatively muted inflation in Asia, we derived a regional factor that was driving inflation in the Asia by running another PCA on the various Asian economies’ inflation after filtering out the impact of the two global factors. The regional factor appeared to be related to China’s economic activity. Intuitively, China’s slowing growth has been a drag Asia’s growth and, by extension, demand as well. Asia’s headline inflation momentum analysis shows that the regional inflation backdrop has been dampened by cooling price pressures in China.

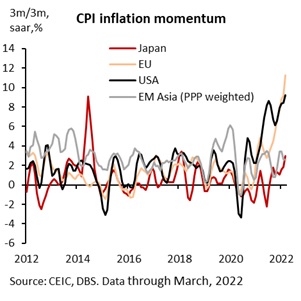

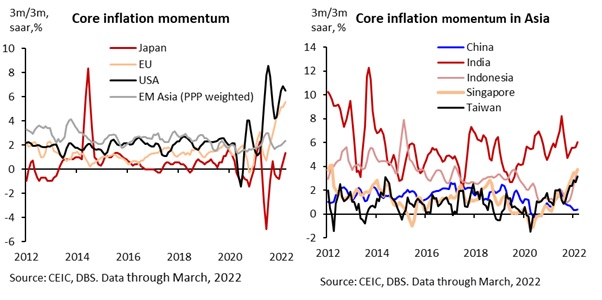

The pick-up in price pressure in the US and Europe is not just commodities and supply driven. Core inflation momentum (that excludes volatile food and energy price dynamics) in the US and Europe has also surged to multi-year highs. Underlying pressures for Japan and Asia are comparatively subdued. Japan’s core momentum has however turned positive after the steep drop in 2021. In Asia, China is moderating, while Indonesia, India, Singapore, and Taiwan have picked up, reflecting some underlying pressures.

To read the full report, click here to Download the PDF.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024