- To assess the macro risk climate, we rank macro vulnerabilities across 25 key EM economies

- Compared to some large emerging market economies, Asian countries look fairly healthy

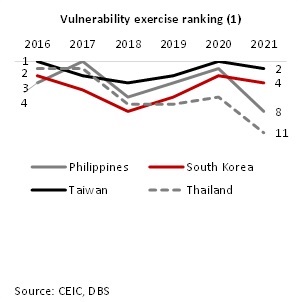

- Taiwan and South Korea have some of the best scores in the EM space

- Thailand and Philippines have downshifted somewhat from strong external positions

- China, India, Malaysia, and Indonesia fall in the middle of the EM vulnerability cohort

Related insights_tr

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- DBS Stock Pulse: Global technology - 2 major takeaways from ASML and TSMC’s latest results19 Apr 2024

Commentary: Rising rates; EM vulnerability

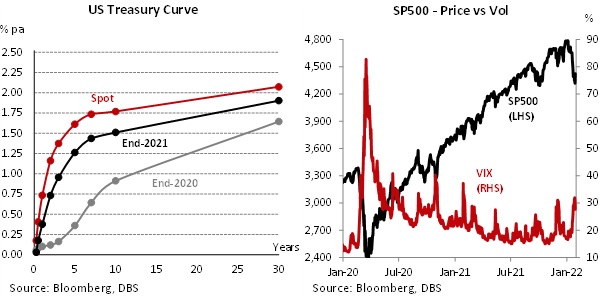

As the US Federal Reserve gears up for interest rate normalization, field curves have shifted in anticipation. The short end of the curve has steepened, the USD has been strengthening, and equity market volatility has risen considerably. For emerging market economies, the environment for fund raising, at the private or sovereign levels, has become challenging. Additionally, high commodity prices will compound the outlook for energy import-dependent economies.

Hence the year that was supposed to be about re-opening after prolonged pandemic-induced stringent measures, is likely going to be a challenging one for a number of emerging economies with inadequate external buffers against substantial funding needs. But which are these economies within a large cohort?

Last week we published the results of a comprehensive macro risk assessment exercise across 25 key emerging market economies (link here). Economies scoring poorly in this exercise run risks of disorderly currency depreciation, capital flow volatility, debt service difficulties, and broader financial and economic distress

Key indicators of analysis are foreign exchange reserves, fiscal balance, private and public sector debt, external (hard currency) debt, savings-investment balance, gross external funding requirement, and real exchange rate (REER). With the exception of REER, the vulnerabilities are assessed in simple ordering. If country A’s debt if higher than country B’s debt, A scores poorer than B.

As for REER, the comparison is a little more complex. If a country’s real exchange rate is 30% above trend, is it more vulnerable than a country which is facing a 30% undervaluation relative to trend? Both are large misalignments, and both come with associated risks. In the former case, the risk could be economic overheating, excess and unhedged borrowing, and excess capital inflows. In the latter case, the risk would include high imported inflation, loss of purchasing power, and external debt service difficulties. We deal with this issue by taking the absolute deviation of REER from long-term trend; this allows us to catch risks at the both end of the spectrum.

We examine the evolution of these indicators across time series and cross section data, which allows us to glean shifts in relative vulnerability

Key findings:

- In general, vulnerability indicators have worsened in EM in recent years, as both the cover for foreign obligations and fiscal position have slipped in many countries;

- Compared to some large emerging market economies, Asian countries look fairly healthy;

- Taiwan and South Korea have some of the best scores in the EM space

- Thailand and Philippines have downshifted somewhat from strong external positions

- China, India, Malaysia, and Indonesia fall in the middle of the EM vulnerability cohort; while there are other economies with worse fundamentals, a year of higher rates and likely volatility in capital markets will keep the policy makers of these four economies on their toes.

We also run the exercise with the data available for each year, going back to 2016. We find:

- South Korea and Taiwan have consistently led EM rankings;

- India, Indonesia, Malaysia have not moved much;

- Driven largely by massive debt build-up, both private and public,, China has slipped from #9 in 2016 to #14 in 2021;

- The pandemic has been harsh on the Philippines Thailand, as the former slipped from #3 in 2016 to #8 in 2021, while the latter slipped from #2 to #11 during the same period.

Macro vulnerabilities don’t emerge overnight; they build up steadily. Keeping track of them therefore does not warrant monitoring of high frequency data. In this exercise, we find that a wide array annual data provides the depth and breadth necessary to carry out such analysis. We plan to keep extending this annual exercise.

To read the full report, click here to Download the PDF.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights_tr

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- DBS Stock Pulse: Global technology - 2 major takeaways from ASML and TSMC’s latest results19 Apr 2024

Related insights_tr

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- DBS Stock Pulse: Global technology - 2 major takeaways from ASML and TSMC’s latest results19 Apr 2024