Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Gold rallies on slowing CPI data. The past week (ended 11 November) was a significant milestone for bullion as it recorded its best weekly performance (+5.3%) since March 2020, and an impressive +8.9% gain from recent lows in November. This rally was driven primarily by cooler-than-expected US CPI data for the month of November (actual: +0.4% m/m, consensus: +0.6%; actual: +7.7% y/y, consensus: +7.9%), which raised hopes of slower rate hikes moving forward and provided a brief respite from dollar strength (the DXY index ceded 4.1% for the week). This puts gold’s YTD performance at -3.0% and firmly establishes it as one of the top-performing asset classes for the year thus far.

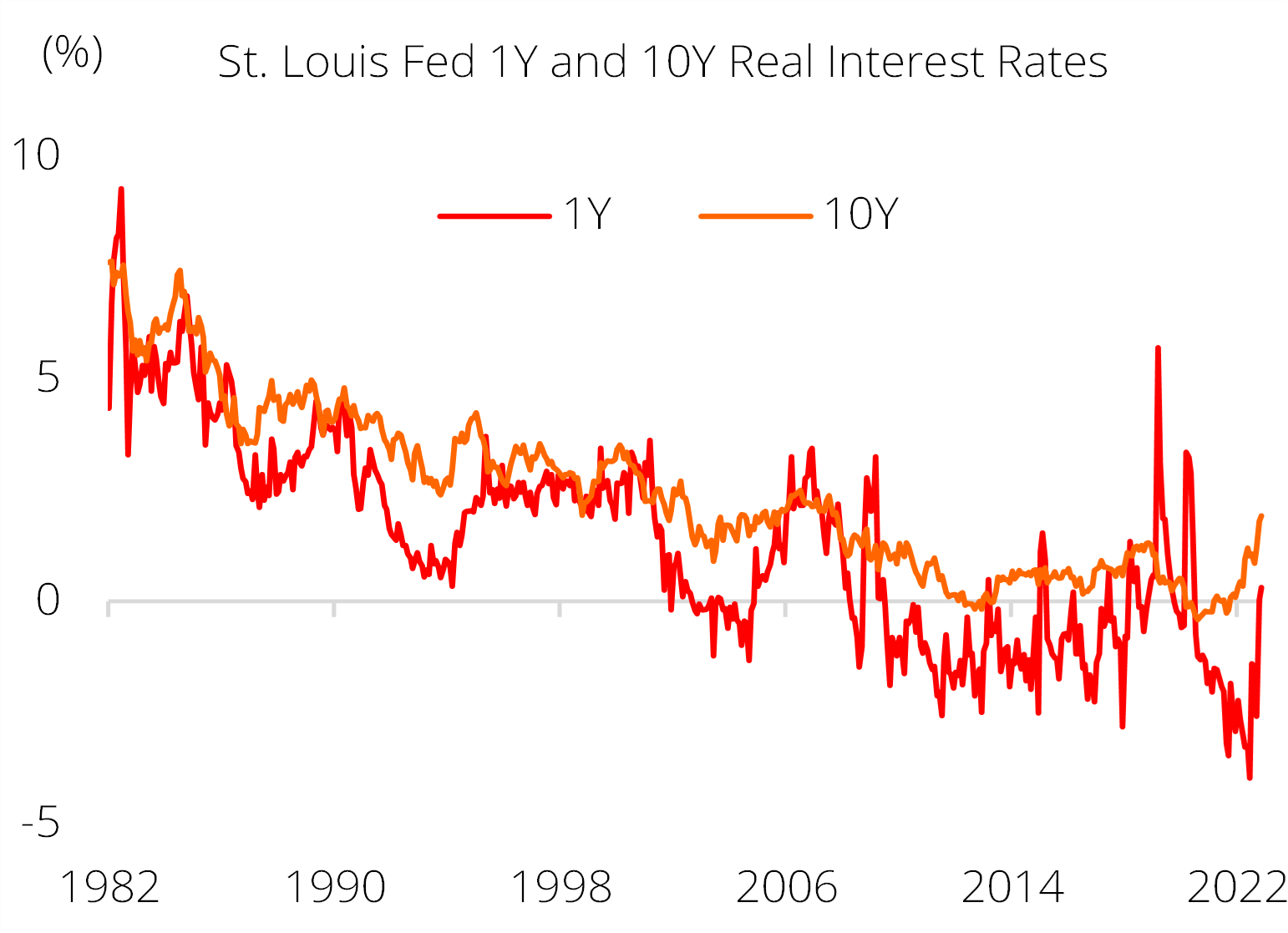

A victim of positive real rates. Notwithstanding the strong relative performance of gold this year, there are undeniable headwinds facing bullion, chief among which are positive real rates. As can be seen in Figure 2, the 1Y real interest rate has nudged its way into positive territory since June 2020 while the 10Y real interest rate sits almost at 2.0%. This has a significant impact on the attractiveness of gold since the latter is a non-interest-bearing asset. As we wade deeper into a new regime of higher interest rates and inflation rolls over, this dichotomy between interest-bearing and static assets will become increasingly important in determining how investors allocate their capital.

Glimmer(s) of hope. Positive real rates and dollar headwinds are big challenges for gold, but there are some bright spots for its nearer term outlook. While the timing of a Fed pivot remains uncertain, there are indications that the pace of rate hikes may slow. This should weaken the dollar and provide some reprieve for gold, which is often seen as an alternative currency to the greenback. Geopolitical uncertainty is another potential tailwind for the safe haven asset; political turmoil in the UK (which saw multiple key appointment holder changes), continued ambiguity surrounding China’s zero-Covid policy, and the persistence of conflict in Eastern Europe, could all potentially provide a short-term catalyst for gold. Central bank buying has also kept gold prices buoyant – global purchases in 3Q amounted to almost 400 tonnes, the single largest quarter of demand from this sector since 2000 and more than a 300% increase on a y/y basis.

Figure 1: Gold price vs DXY: YTD 2022

Source: Bloomberg, DBS

Figure 2: Real interest rates are turning positive

Source: Federal Reserve Bank of Cleveland, DBS

What does the future hold for gold? The superlative rally in November driven by slowing inflation suggests that investors are primarily concerned with one thing in the short-to-medium term, and that is the Fed pivot. With inflation data trending in the right direction, a turning point (whether a pause or full-on pivot) is on the horizon in 2023. This would see the dollar normalise and catalyse a positive re-rating for gold. But beyond the pivot, the backdrop of positive real rates does warrant a re-assessment of gold’s near-term attractiveness from a return perspective. Nonetheless, we remain constructive on gold as a portfolio risk diversifier given its low correlation with equities and bonds. Investors can gain exposure to gold via the following expressions: i) physical gold; ii) gold futures; iii) ETFs and managed funds on physical gold and gold mining equities; or iv) direct holdings in gold mining equities, which are essentially a leveraged expression of gold.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Related insights_tr

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024