- Our strategy focused on high quality equities is bearing fruit as the segment outperformed by 6.6% pts YTD

- Expect the flight to quality to persist as portfolio allocators navigate twin macro headwinds of earnings and economic slowdown

- Smaller companies without the benefits of economies of scale will face headwinds from higher cost of capital, as the era of cheap money comes to an end

- Flight to quality has translated to sharp disparity in performance; Technology and Financials registered respective outperformance of 26.0% and 23.5% YTD over their respective small-cap peers

- Maintain our strategy of sticking to quality plays across equities and bonds given attractive risk-reward

Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024

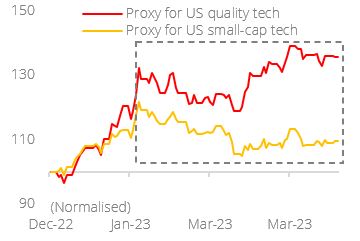

Pivot to quality plays bearing fruit. Faced with rising recession risks, sticky inflation, and corporate margin compression, we advised investors to stick with high quality equities at the start of the year. Our strategy is bearing fruit. Quality plays (as proxied by S&P 500 Quality index) has outperformed US small caps by 6.6% pts year-to-date (YTD) and we expect this momentum to continue as portfolio allocators are confronted with the following macro headwinds in the coming months:

- US earnings recession is on the rise with earnings forecast deteriorating further to

-3.7% y/y in Mar-23 (vs. -1.5% in Feb-23 and average of +18.9% y/y in 2022). - US ISM manufacturing fell further into contractionary territory at 46.3 in Mar-23 (vs. 47.7 in Feb-23 and average of 53.5 in 2022); a sub-50 reading suggests that manufacturing activities are in contraction mode.

- According to Bloomberg Economics, the probability of a US recession over the next six months has surged from 11.5% in Dec-22 to 99.9% in Feb-23.

The persistence of macro challenges is expected to underpin the “flight to quality”, thus translating to broad bifurcation in performance across sectors.

The Haves & the Have-nots: Bifurcating sectoral performance as era of cheap money comes to an end. As the Fed keeps monetary policy tight and the cost of capital stays elevated, smaller companies without the benefits of economies of scale will face substantial challenges in navigating an environment where the era of cheap money has come to an end. The market recognises the new reality and this explains the disparity in performance between quality plays and smaller caps in the Technology and Financials space:

- US Technology: US technology quality plays (as proxied by NYSE FANG+) rallied 35.6% YTD and this translates to an outperformance of 26.0% pts over US small-cap technology plays (as proxied by Russell 2000 Technology).

- US Financials: US financials quality plays (as proxied by S&P 500 Banks) fell 7.4% YTD and this translates to an outperformance of 23.5% pts YTD over US small-cap banking plays which plunged 30.9% (as proxied by S&P 500 Regional Banks).

Bottom-up anecdotal evidence reinforces our view. Despite the fiasco ravaging smaller regional banks in the US, it is however an oasis of calm among the larger quality banks and the ongoing earnings season attests to this. For instance:

- Citigroup (C US): Citigroup reported EPS of USD2.19 in 1Q23 and the exclusion of divestment gains from its India consumer business translates to an EPS of USD1.86 – both of which are higher than Bloomberg consensus forecast of USD1.645. Rising rates boosted net interest income (NII) across the board while the US Personal banking segment also registered strong loan growth.

- JP Morgan (JPM US): JP Morgan reported EPS of USD4.1 in 1Q23 (vs. Bloomberg consensus of USD3.345). NII soared on the back of higher rates.

Stick to quality across equities and bonds. The acute pullback in financial markets last year has thrown up fresh opportunities across the risk spectrum. But we maintain our strategy of sticking to quality plays across equities and bonds given attractive risk-reward in this space.

Figure 1: Quality tech outperformance

Source: Bloomberg, DBS

Figure 2: Quality banks outperformance

Source: Bloomberg, DBS

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024

Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024