- Oil prices, which have languished for much of 1Q23 found some reprieve in a moderating interest rate outlook amid banking sector woes in the West

- Further price support came by way of surprise cuts by OPEC+ of 1.15mmbpd starting May 2023

- On the demand side, China’s reopening is a major tailwind and will continue to provide support for oil prices

- DBS forecasts Brent crude oil price to average USD85-90 for 2023

- We remain constructive on European oil majors as they continue to benefit from elevated oil prices

Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024

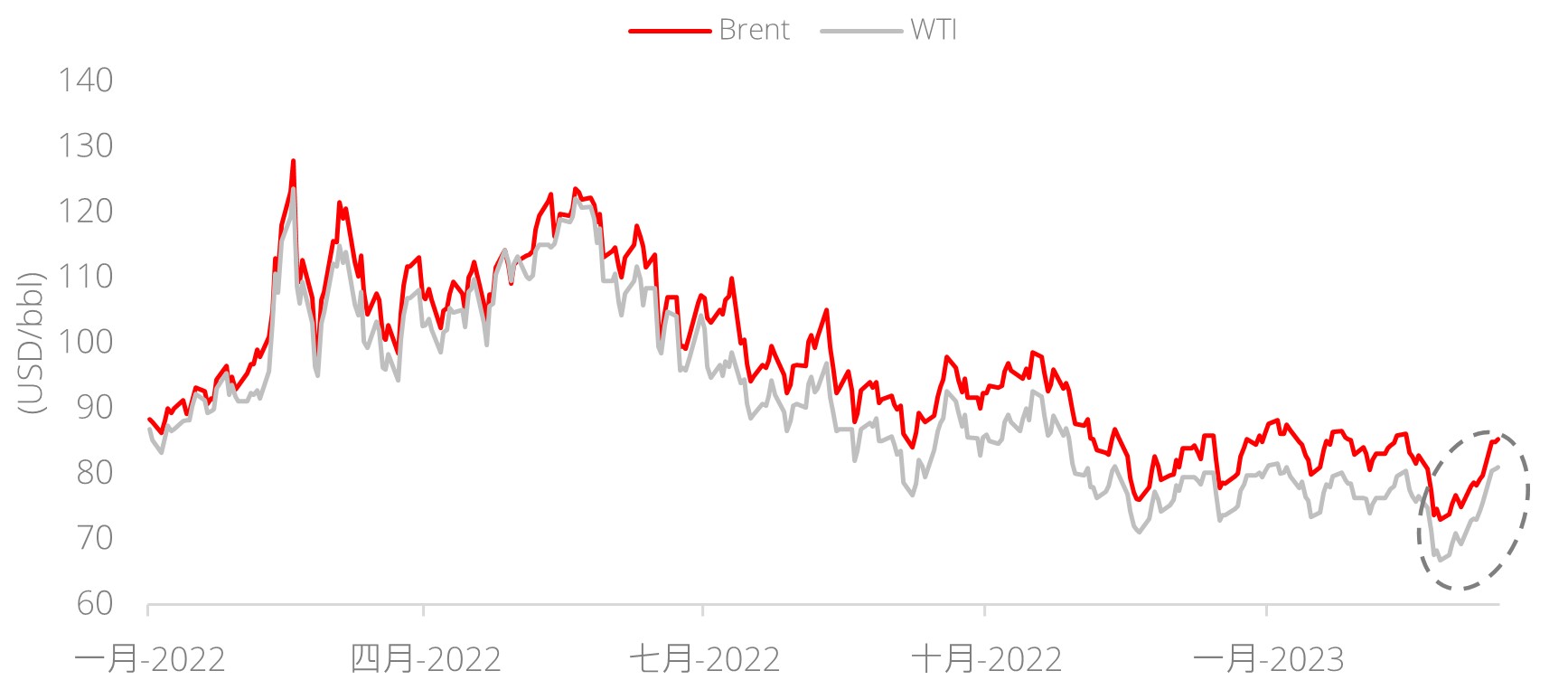

A positive change in narrative for oil prices. Oil languished for much of the first quarter, with Brent and WTI briefly dipping below USD70 and USD60 per barrel respectively earlier in March, driven by turmoil in the US and Europe banking sectors and corresponding worries of recession and falling demand for energy. This risk-off sentiment, however, did not last long; with financial system risks now seemingly ringfenced by regulators, investors wasted no time in finding a silver lining in the form of a moderating interest rate outlook. Futures markets have now shaved terminal rates by some 75-100 bps and are now pricing 70 bps of cuts (from peak) by the end of the year, and a cumulative 200 bps of cuts by end-2024. This alleviated some of the demand concerns around energy and lifted oil prices.

OPEC+ to cut production by 1.15mmpd starting May 2023. This turnaround in prices was further supported when OPEC+ announced a surprise production cut of 1.15mmpd on 3 April, sending WTI and Brent prices up 6% on the same day, to c.USD80/bbl and c.USD85/bbl respectively. These additional cuts came on the back of a headline reduction of 2.0mmbpd last October, bringing the total volume of OPEC+ cuts since last year to 3.15mmbpd, or roughly 3.1% of global demand according to OPEC+ estimates.

Figure 1: Oil price surged after OPEC+ announced cuts

Source: Preqin, DBS

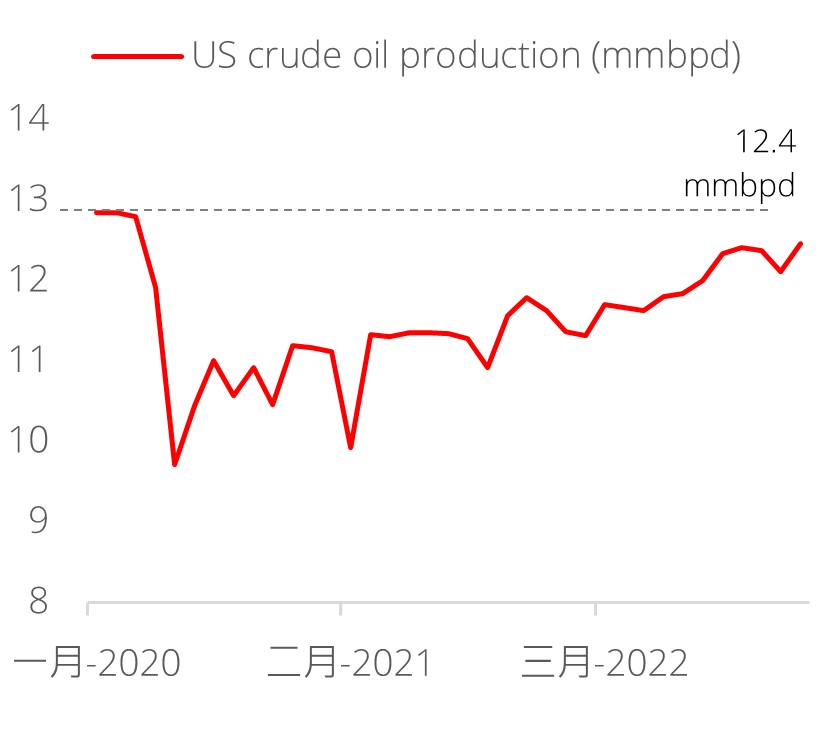

Spurred by stagnant US production and Russia production cuts. The cuts will be led by Saudi Arabia (0.5mmbpd), with UAE (144kbpd), Kuwait (128kbpd), Iraq (211kbpd), Algeria (48kbpd), and non-OPEC partners Kazakhstan (78kbpd) and Oman (40kbpd) also participating. We believe the decision to implement the latest round of cuts was spurred by Russia’s announcement that they would cut production by 0.5mmbpd earlier in March, as well as muted growth in US oil production over the past 6 months as that will allow OPEC+ to shore up oil prices without conceding market share.

Oil demand to remain supported by rebounding air travel and China’s reopening. In addition to supply-side factors, oil prices will also be supported on the demand side from growing international travel and China’s reopening. The International Energy Agency estimates that rebounding jet fuel use and a resurgent China will see global oil demand ramp up by a total 3.2mmbpd for 2023. China alone is set to contribute 0.8mmbpd of that increase. The easing of travel restrictions is set to boost China’s demand for oil by c.0.4 mmbpd while improving subway mobility on the domestic front (due to the abolishment of the health code and centralised quarantine practices) will boost consumption by another 0.4mmbpd. China has historically been the world’s second largest consumer of crude oil, accounting for c.15% of global demand, and the impact of its reopening should not be underestimated.

Source: Bloomberg, DBS

Figure 3: China oil demand to pick up post reopening

Source: US Energy Information Administration,

Bloomberg, DBS

Outlook for oil remains positive; reiterate constructive stance on European oil majors. While oil prices have experienced a significant run-up, we are cognizant that this price rally is still in its nascency. Furthermore, there are other factors such as inflation and interest rates that could alter the outlook of oil prices. However, if the latest round of supply cuts is fully and successfully implemented, they should have a bigger and more sustainable impact on oil prices compared to the headline 2.0mmbpd cuts announced last October. Having said that, DBS is revising up our forecasts for the Brent crude oil price average for 2023/24 by USD5/bbl to USD85-90/bbl and USD82-87/bbl, respectively. While such prices are not as high as what we have seen in 2022, they remain meaningfully above pre-Covid levels and will continue to benefit companies in the crude oil and energy sector. We maintain our constructive stance on European oil majors due to their attractive dividend yields and diversification of operations along the entire energy value chain. Investors can also express the upside potential of energy markets in their portfolios through sectoral ETFs and managed funds.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024

Related insights_tr

- StarHub24 Apr 2024

- DBS Stock Pulse: Seatrium – A respite from the weak YTD performance?24 Apr 2024

- Nanofilm Technologies International Ltd23 Apr 2024