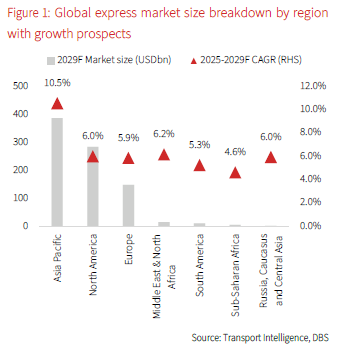

- Despite global trade headwinds, global express market is poised for a robust growth of 7.9% CAGR in 2025-2029F, with Asia Pacific as the key growth engine

- While UPS withheld guidance for a second straight quarter, FedEx reinstated FY26F guidance after posting its strongest revenue growth since the pandemic; Portfolio diversification and efficiency gains drive outperformance of Chinese peers

- Global logistics giants remain steadfast on enhancing profitability amid evolving trade dynamics, while prioritising capital returns

- Chinese peers to see brighter prospects ahead, as regulators’ strong opposition to “involutionary competition” paves the way for regional price hikes and a more rational market environment

Related insights

Strong growth trajectory with Asia Pacific serving as key engine. The International Monetary Fund (IMF)’s latest forecasts (as of Oct 2025), point to global GDP growth decelerating from 3.3% in 2024 to 3.2% and 3.1% in 2025F and 2026F, respectively. Similarly, the IMF has revised down its projected world trade volume growth to 2.9% in 2025-2026F (vs previous projection of 3.3% in Oct 2024), reflecting the impact of persistent trade restrictions.

Despite headwinds in the broader logistics market from the evolving global trade dynamics, the global express market is well-positioned to sustain robust growth. The sector is projected to grow at a 7.9% CAGR in 2025-2029F, following an elevated 8.8% y/y in 2025F. This momentum is primarily driven by the robust B2C segment, which is projected to grow at a substantial 10.8% CAGR (vs. a sluggish 2.5% CAGR for B2B segment). Notably, the Asia Pacific region is expected to serve as a key engine with a strong CAGR of 10.5% in 2025-2029F (vs. 6.0%/5.9% CAGRs from North America and Europe). The region is expected to consolidate its position as the largest contributor at 45% of global market by 2029F (vs. 33%/17% from North America and Europe).

Global logistics majors demonstrated divergent performance. UPS posted weaker-than-expected 2QFY25 results as operational challenges weighed on margins, prompting management to withhold guidance for a second straight quarter. In contrast, FedEx reported its strongest revenue growth since the pandemic and reinstated FY26F full-year guidance in Sep 2025, signalling improved visibility despite global trade uncertainty.

In China, competitive intensity remained elevated through 1HFY25 until regulatory intervention in Jul 2025 to curb aggressive price cutting. ZTO Express, which mainly targets the domestic e-commerce parcel market, came under pressure, posting softer 2QFY25 results with sharp gross margin contraction and lowering its FY25F parcel volume outlook. In contrast, SF Holding delivered record 1HFY25 net profit on the back of portfolio diversification and efficiency gains. J&T Global Express also benefited from a broader geographical footprint, gaining market share in 1HFY25 as EBITDA expansion in Southeast Asia and New Markets more than offset contraction in China.

Favour Chinese logistics players at this stage. Chinese logistics players appear better positioned to capture upside, while global peers’ disciplined focus on profitability and shareholder returns should help mitigate downside risk. Global leaders such as UPS and FedEx continue to prioritise revenue quality and cost efficiency, shifting towards higher-margin services and productivity gains. Their strong commitment to shareholder returns provides stability amid softer trade environment, with FedEx planning a 5% dividend increase in FY26, its fifth consecutive hike. UPS is also announcing a USD1.0bn share buyback alongside USD5.5bn in dividends.

In contrast, Chinese peers are benefiting from strong export momentum despite trade frictions, supported by successful trade diversification and robust cross-border e-commerce demand. Regulatory intervention since Jul 2025 is expected to gradually rein in excessive price competition, paving the way for a more rational market structure and a clearer path to margin recovery.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.