- US/Eurozone: August’s labour report is in the spotlight as a key determinant for the Fed’s September rate cut; Bayou's confidence vote on austerity has ignited political uncertainty in France

- India: A steep US 50% tariff imposition on Indian goods is forcing immediate, broad-based mitigation from authorities as future tariff evolution remains highly opaque

- South Korea: BOK maintained its 2.50% base rate as expected, signalling caution over the buoyant property market's exacerbation of high household debt

Related insights

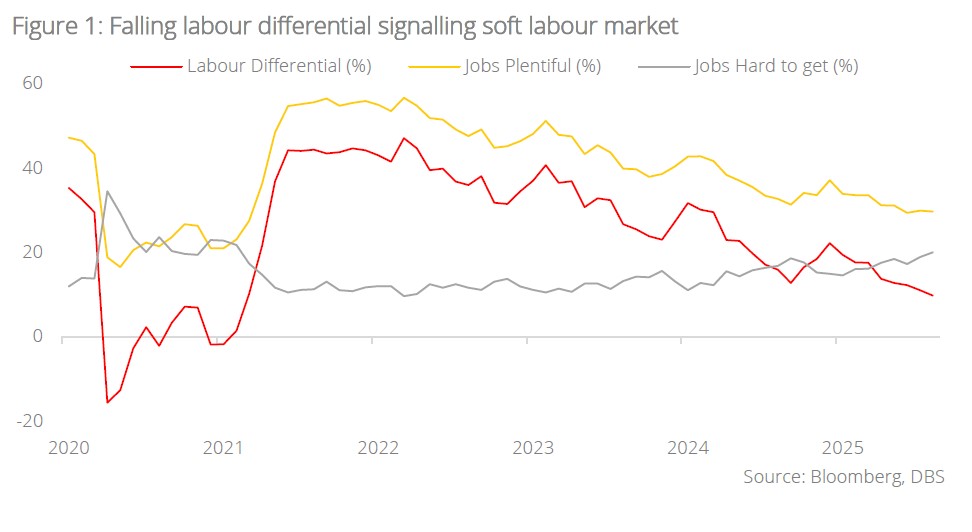

US/Eurozone: August’s US labour data in focus, France’s political uncertainty deepens. August’s labour report, due on 5 Sep, became a focal point for the market as Powell’s Jackson Hole speech last week opened the door for the FOMC’s September rate cut thanks to a softening labour market. The consensus anticipates August’s nonfarm payroll to stay below 100k for a fourth straight month and the unemployment rate to rise to 4.3% from July’s 4.2%.

Recent Conference Board reports showed that the share of consumers that feel jobs were hard to get reached 20% in August—its highest since Feb 2021. The share of jobs considered plentiful slipped to 29.7% in August from 29.9% in July. The labour differential (i.e. the difference between the two and a good predictor for unemployment rate) fell to 9.7% in August from July’s 11%.

While inflation remains another concern for the US market, PCE inflation due on 29 Sep is expected to show headline inflation slowing to 0.2% m/m in July from 0.3% in June, while core holds steady at 0.3%. Even if PCE inflation numbers turn out hot, we doubt the market would be dissuaded from pricing in a September cut.

Trump faces challenges surrounding his legal capacity to fire Fed Governor Lisa Cook. Former Fed Vice Chair Lael Brainard warned that Trump’s political manoeuvrings to gain the majority in the seven-member Board of Governors could lead to the removal of 12 Fed district presidents whose terms are up for renewal in Feb 2026. US Treasury Secretary Scott Bessent plans to start interviewing candidates for Powell’s successor in September, well before his term ends in May 2026, which is viewed as another escalated effort to remove Powell early or force his resignation.

Shifting to Europe, French political uncertainty rose after Prime Minister Francois Bayou’s call for a confidence vote on 8 Sep for his unpopular austerity package for 2026. The far-right and left-wing oppositions are united in their dissent with protests and strikes planned soon after the vote. Suppose the vote fails and government falls, President Emmanuel Macron will likely resist calling another snap election, following the poor outcome at the last one in Jun-Jul 2024, opting instead for a new prime minister. While this does not alleviate the political deadlock in France, the Eurozone economic outlook for 2025-2026 has become more positive compared to 2024, notwithstanding Trump’s tariffs.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.