Related insights

Mea Culpa: Fed affirmed higher for longer stance. Fed Chair Jay Powell has in a congressional testimony warned that faster monetary tightening is necessary if incoming data comes in stronger than expected. The hawkish comments triggered a selloff in equities and sharp spike in the 2Y US Treasury yield. But wait, hold on. Didn’t the Fed Chair just opine in February that the “disinflationary process” had begun? A move which triggered hopes of a “goldilocks” environment for risk assets?

This is yet another case of the Fed flip-flopping and one shouldn’t be surprised anymore; you may recall how the central bank also previously pivoted from “Team Transitory” to “Team Structural”. Yesterday’s U-turn marks a continuation of this erratic pattern. The Fed’s apparent indecision on where inflation is heading can be attributed to the following factors:

§ The Fed’s monetary policy framework “Flexible Average Inflation Targeting (FAIT)” was designed to counter disinflationary pressure in an era where inflation fall short of the 2% target. But times have changed and clearly, the framework does not sufficiently address a post-pandemic world where aggregate demand supersedes aggregate supply.

§ Over dependency on incoming macro data which can be volatile, and this leading to short-termism on policy making.

Low likelihood of Fed abandoning 2% inflation goal. The Fed is essentially caught between a rock and a hard place now. With inflation hovering at 6.4%, attaining its 2% target will necessitate the central bank engineering a deep recession. A second, albeit radical, option right now, is for the Fed to abandon its 2% inflation target and push it higher to 3% (perhaps).

A 3% inflation target has its benefits. It brings policy rates further away from the zero lower bound (ZLB) and in turn, provides the central bank with greater ammunition to fight unemployment through rate cuts in the future.

But in reality, a more likely outcome is for the Fed to stay put and keep its inflation target at 2%. After all, changing a well-entrenched target will subject the Fed to credibility risks and we believe the central bank will not take that step.

Twin Headwinds: Rising cost of capital and rising margin pressure. Rising bond yields translate to higher costs of capital and this will be a significant headwind for companies that are highly leveraged. As we have recently highlighted in CIO Perspectives: Stay with Quality Amid Higher for Longer Rates (dated 23 Feb), the prevalence of sticky wages will translate to margin pressure for companies, particularly the more labour intensive ones. So, highly leveraged companies with thin operating margins should brace for volatility ahead.

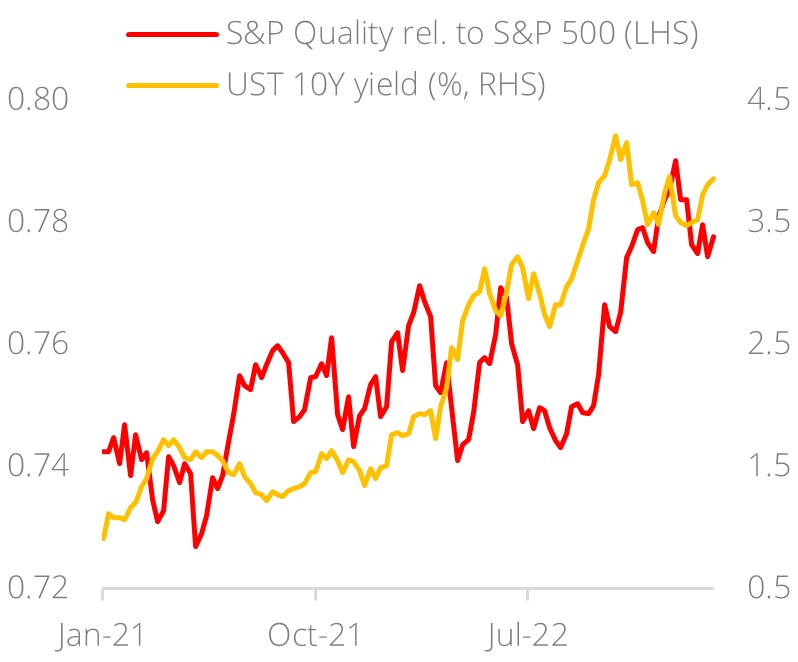

Quality Plays: An enduring strategy for challenging times. To navigate the challenging environment of persistent inflation and higher for longer policy rates, we reiterate our strategy of staying with “Quality Plays”. This is the year for bottom-up stocks selection, a year where selecting and staying with winners possessing strong corporate fundamentals will reap dividends. As Figure 1 shows, quality plays have been outperforming the broader market in a rising rates environment and we expect this momentum to persist.

Figure 1: "Quality Plays" outperformance

Source: Bloomberg, DBS

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.