Related insights

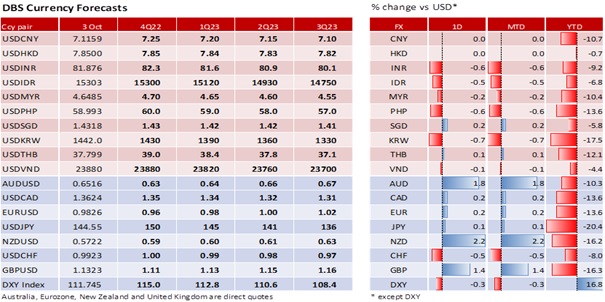

GBP appreciated 1.4% to 1.1323 after the Truss government dropped a plan to scrap the 45% top income tax rate on the highest earners. Only a week ago, the GBP plunged to a new record low of 1.0350 on 26 September. The pound’s recovery was fuelled initially by the Bank of England’s Gilt buying programme to 14 October (aimed at averting a full-blown pension crisis) and later by its hint for a jumbo rate hike at its next meeting on 3 November. However, it is premature to conclude that the worst is over. Although the 10Y Gilt yield eased to 3.964%, it held around the levels of the mini-budget announcement on 23 September. So was the GBP.

Last Friday, Standard and Poor’s downgraded UK’s debt rating outlook to “negative” from “stable”. Chancellor Kwasi Kwarteng still needs to explain how the government will fund the remaining GBP43bn package of tax cuts. BBC reported that the details could arrive later this month instead of 23 November, and possibly lead to another Tory rebellion over cuts in public spending. According to Reuters, Moody’s considered the tax cuts as credit negative and may conduct a formal review on 21 October. However, Prime Minister Liz Truss attributed the market turmoil to poor communication, still brushing aside the criticisms of the policy. If markets view the U-turn on the tax cut as throwing a bone to the dogs, selling pressures will resume.

AUD was one of chief beneficiaries of the relief rally, appreciating 1.8% to 0.6516, its highest close since 23 September. However, AUD has yet to break above last week’s trading range between 0.6363 and 0.6550. Today, we see the Reserve Bank of Australia lifting the cash rate target by 50 bps to 2.85%, above the 2.5% neutral rate. The Australian Bureau of Statistics reported that CPI inflation eased to 6.8% YoY in August from 7% YoY in July. Taken together, inflation in 3Q22 will be higher than the 6.1% average in 2Q22 and well above the 2-3% target range. The labour market is tight despite the higher unemployment rate to 3.5% in August from its 50-year low of 3.4% in July. To ease labour shortages, the government lifted the ceiling on permanent migration to 195k from 165k this financial year.

Australia’s real GDP growth improved to 3.6% YoY in 2Q22 from 3.3% in 1Q22. However, the OECD does not expect the global slowdown to spare the Australian economy; it forecasts growth halving to 2% in 2023 from 4.1% this year. Fearing a global recession, Treasurer Jim Chalmers ruled out returning to a budget surplus over the next three years to the next election in 2025. Chalmers will present the Budget on 25 October after conferring with his counterparts at the G20 meetings of finance ministers and central bankers on 12 October. Chalmers is mindful of the market’s warning from UK’s mini-budget crisis to align government and central bank policy. His challenge will be to provide relief to the cost-of-living crisis with an economic dividend that does not add to inflationary pressures.

Quote of the day

“To succeed in life, you need three things: a wishbone, a backbone and a funny bone.”

Reba McEntire

4 October in history

Dutch mathematician Christian Huygens patented the pocket watch in 1675.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.