Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

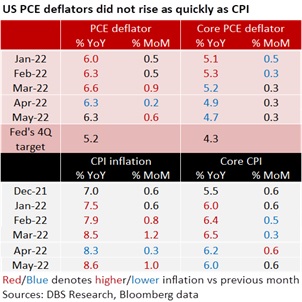

US PCE core deflator slowed the third straight month from February’s high of 5.3% YoY to 4.7% in May, on track to meet the Fed’s forecast of 4.3% for 4Q22. In month-on-month terms, core inflation did not rise to the 0.4% consensus and held at the same 0.3% for the fourth month. However, the headline PCE deflator made little progress towards the Fed’s 5.2% target. Apart from holding at 6.3% YoY for the second month in May, headline inflation hastened from 0.2% MoM in April to 0.6% in May. Overall, the numbers were consistent with the Fed’s commitment to frontload hikes to 3.50% this year.

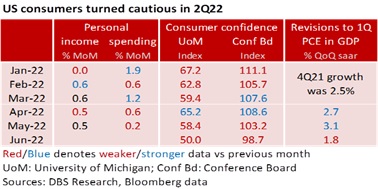

However, attention is on this morning’s headlines everywhere – the S&P fell 20.6% YTD to post its worst first 1H sell-off in 50 years. Investors struggled with the Fed’s determination to walk a tightrope i.e., frontloading outsized rate hikes to cool inflation without tipping into a US recession. The focus in the US Treasury market also shifted from high inflation and rising rates to how they are hurting consumer confidence and spending, the largest contributor to US GDP. Although US bond yields spiked to 3.50% into the 75 bps hike in mid-June, the 10Y yield headed south to 3% (2Y was below 3% at 2.95%) by the end of 1H22. Yesterday, it was clear that the market was spooked more by the disappointing personal spending than some Fed officials calling for another 75 bps hike on 27 July.

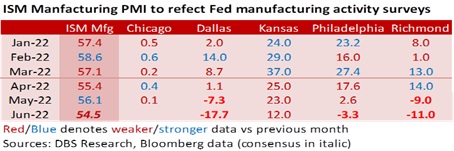

Today, expect the US ISM manufacturing PMI to disappoint. Given the deterioration in the Fed’s manufacturing indices, consensus might be too optimistic in predicting a modest slowdown to 54.5 in June from 56.1 in May. Apart from lower averages in 2Q, three of the five Fed districts reported negative readings. Markets see the consumer spending and private investment that the Fed relies on for hikes weakening. It did not help that the Atlanta Fed GDPNow Index also turned negative at -1.0 on 30 June, keeping US recession fears alive.

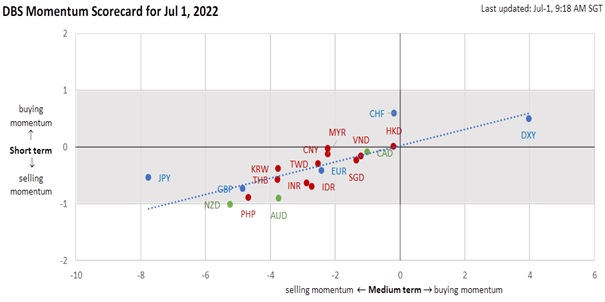

After posting its strongest 1H rally (9.4%) in 12 years, we believe DXY will weaken with US fundamentals in 2H. The last time DXY appreciated around 10% was in 1H 2010; it subsequently depreciated 8% in 2H.

Quote of the day

“Things are never so bad they can’t be made worse.”

Humphrey Bogart

1 July in history

Albert Einstein introduced his theory of special relativity E=MC2 in 1905

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024