Related insights

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- HKD rates: HIBOR downtrend to ease 19 Apr 2024

DXY did not deviate from 102, keeping to a tight 101.6 to 102.4 range for a second session. The “hawkish” FOMC minutes did not wean the US Treasury 2Y and 10Y yields from 2.50% and 2.75% respectively. The minutes affirmed the Fed’s decision to “expeditiously” return the Fed Funds Rate into the 2-3% neutral range with three 50 bps hikes in May, June and July. Although consensus was lacking on the hiking pace (50 bps, 25 bps or pause) at the September meeting, the odds are high for slower GDP growth and higher unemployment rate outlooks in the Summary of Economic Projections. Overall, investors were hopeful that the Fed might not risk a US recession to fight inflation. Dow, S&P 500 and Nasdaq Composite rose 0.6%, 1.0% and 1.5% respectively. Today, consensus is looking for a modest upward adjustment in US’s 1Q22 GDP growth to -1.3% QoQ saar from its advanced estimate of -1.4%. Pay attention to initial jobless claims which have stayed above 200k in the past two out of three weeks. These numbers will not eclipse tomorrow’s PCE deflators for signs of a nascent peak in US inflation.

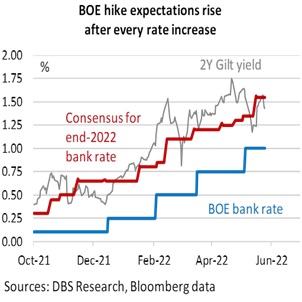

GBP to push above 1.2470-1.2600 range towards 1.28. The Bank of England sees the need to keep hiking because of elevated inflation but recession worries have kept the pace to 25 bps. Although consensus predicts two more 25 bps hikes to 1.50% this year, it has also been moving up with the 2Y Gilt yield after each BOE meeting. Like other central banks, we see the bank rate rising above the 2% inflation target.

CNY depreciated by 0.6% to 6.6931, closing lower from its open for the first time in a week. Premier Li Keqiang warned that China’s economy might contract in 2Q22. The prospect was affirmed by the 4.5% YoY decline in Singapore’s exports to China in April, its first contraction since July 2020, from the disruptions caused by the Covid lockdowns. Real GDP growth slowed to 1.3% QoQ sa in 1Q22 from 1.6% in 4Q21. On 20 May, the central bank (PBOC) lowered the 5Y loan prime rate by 15 bps to 4.60%. Although a weaker CNY is considered positive for exports, China Inc is more concerned about the US and EU economies slowing on the Russia- Ukraine crisis. It also associates a weaker CNY with higher imported costs. For now, we do not see USD/CNY rising to the 7 levels seen during the US-China trade war. The Biden administration is considering lowering US tariffs on Chinese imports which US Trade Representative General Counsel Greta Peisch said might take months to reach a decision.

Quote of the day

“Once we accept our limits, we go beyond them.”

Albert Einstein

26 May in history

Dow Jones Index was born in 1896.

Topic

Explore more

E & S Macro StrategyThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- HKD rates: HIBOR downtrend to ease 19 Apr 2024

Related insights

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

- HKD rates: HIBOR downtrend to ease 19 Apr 2024