Related insights

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- Marriot International23 Apr 2024

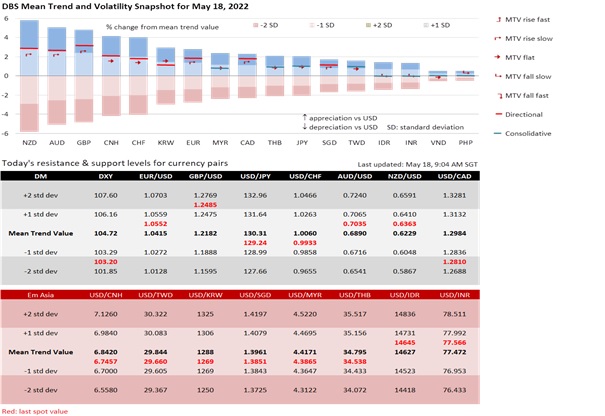

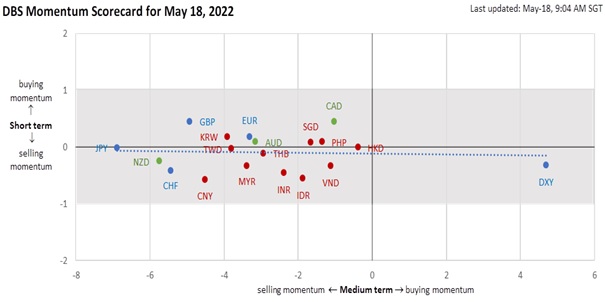

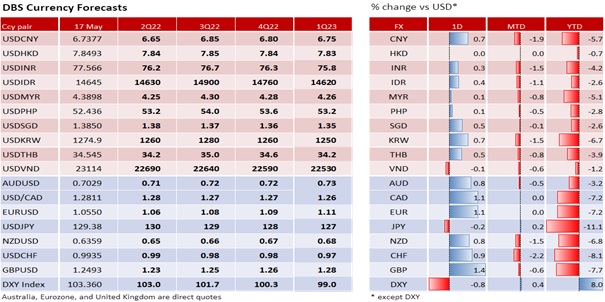

DXY depreciated 0.9% to 103.28 and returned its post-FOMC rally. Dow and S&P 500 rose 1.3% and 2.0% respectively. Investors were relieved that US advanced retail sales continued to expand in April amidst better-than-expected industrial production and capacity utilization. The Nasdaq Composite index rallied 2.8%, following through on the tech rally in Asia from Chinese Vice Premier Liu He’s support for digital platform companies, a sign that Beijing may ease its clampdown on tech companies. CNY recovered 0.7% to 6.7377 per USD from last Friday’s 6.7893, its worst level since September 2020. The US Treasury 10Y yield firmed 10.4 bps to 2.986% but stayed below 3%. Fed Chair Jerome Powell affirmed that the Fed would keep hiking, above neutral (or 2% to 3%) if necessary, to bring down US inflation. However, St Louis Fed President James Bullard assured that markets have already priced the two 50 bps hikes expected in June and July.

European currencies performed best on Tuesday. GBP, EUR and CHF appreciated by 1.4%, 1.1% and 0.9% respectively. Instead of contracting like the US economy, 1Q22 GDP expanded 0.8% QoQ sa in the UK and 0.3% in the Eurozone. GBP could push above 1.25 after recovering the losses after the Bank of England meeting on 5 May. Apart from positive 1Q22 GDP growth eroding the BOE’s recession risk scenario, today’s CPI inflation could come in lower-than-expected in April (9.1% YoY consensus vs 7.0% previous) and dampen its expectation for double-digit inflation in late 2022. Following BOE Chief Economist Huw Pill’s warning that rising rates might dampen the property sector, consensus expects growth in the house price index to slow to 9.9% YoY March from 10.9% in February. EUR is firm after closing at 1.0550, above 1.05 for the first time three sessions.Klaas Knot became the first European Central Bank official to call for a larger 50 bps hike if Eurozone inflation broadens. With the door open for the -0.50% deposit facility rate to turn positive earlier instead of late 2022, the EU 2Y bond yield surged by 24 bps to 0.377%, its highest level since November 2011. The ECB is widely expected to end net asset purchases and hike rates in July.

Commodity currencies improved with risk appetite.AUD appreciated 0.8% to 0.7030, its first close above 0.70 since 6 May. Today, Australia’s wage growth might beat the consensus to rise to 2.5% YoY in 1Q22 from 0.7% in 4Q22. More companies face pressure to offer higher wages to attract and retain staff in the tight labour market. NZD strengthened 0.8% to 0.6359. Next week, we expect the Reserve of New Zealand to lift the official cash rate by another 50 bps to 2% on 25 May. CAD appreciated less by 0.3% to 1.2811per USD but extended its appreciation below 1.30 for the third session. Like the US, today’s CPI inflation in Canada is expected to slow to 0.5% MoM in April from 1.4% in March. Higher US bond yields and the risk rally lifted USD/JPY by 0.2% to 129.38, but they were not enough to push it above 130. Emerging Asian currencies, especially the KRW, can recover as pressures abate for USD/JPY, USD/CNY and US bond yields to rise.

Quote of the day

“Everything is changing. People are taking their comedians seriously and the politicians as a joke.”

Will Rogers

18 May in history

India became the sixth nation to explode an atomic bomb in 1974.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- Marriot International23 Apr 2024

Related insights

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- Marriot International23 Apr 2024