Related insights

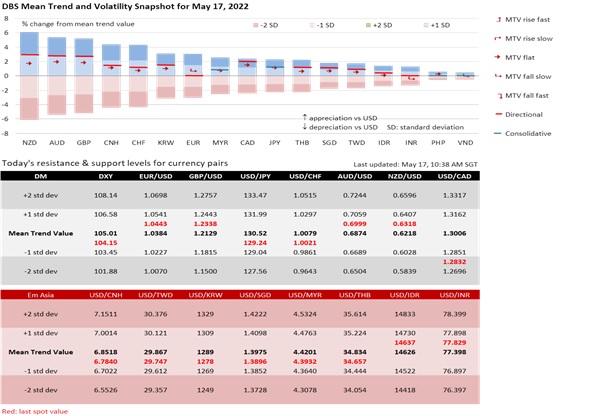

DXY is correcting lower after hitting a 20-year high of 104.85 on 12 May. The US Treasury 10Y yield peaked at 3.127% on 6 May, two days after the Fed delivered the first of the three 50 bps hikes telegraphed. The 10Y yield has returned below 3% since 10 May on doubts that the Fed can rein in elevated inflation with a soft landing. The US economy is one quarter away from a technical recession. Advanced GDP contracted by an annualized 1.4% QoQ in 1Q22, weighed down by record trade deficits from the USD’s strength. Not surprisingly, Fed Chair Jerome Powell conceded last week that factors outside the Fed’s control, such as the global slowdown and geopolitical risks, could tip the US economy into recession.

GBP might have bottomed at a two-year low of 1.2202 on 12 May, the day UK GDP bested US GDP with a preliminary 0.8% QoQ sa expansion in 1Q22 and eased UK recession worries raised at the Bank of England’s meeting a week earlier. Stagflation worries might wane again on the 18 May if CPI inflation comes in lower-than-expected in April (9% YoY consensus vs 7% in March) and plays down the BOE’s double-digit inflation warning. We noted GBP did not close below 1.20 after the Brexit referendum in June 2016 except for a week during the Covid-19 outbreak in March 2020.

The factors responsible for the EUR sell-off have waned. EUR might have bottomed at 1.0350 on 13 May. The European Central Bank no longer resists pressure to join the Fed and other central banks in normalizing monetary policy to address elevated inflation. At its meeting on 9 June, the governing council will unanimously agree to end net asset purchase and start rate hikes in July to turn the -0.50% deposit facility rate positive by end-2022. Also, expect more officials to join ECB member Francois Villeroy de Galhau in warning that EUR weakness poses a challenge to its price stability goal. ECB President Christine Lagarde will be speaking today, followed by Vice President Luis de Guindos tomorrow.

Like the UK, consensus expects today’s Eurozone GDP to beat US GDP by expanding in 1Q22 at the same 0.2% QoQ sa (5% YoY) pace as 4Q21. Yesterday, the European Commission did not forecast a recession on the Russia-Ukraine crisis; it downgraded this year’s growth forecast to 2.7% from its previous 4% estimate in February. Last week, the EU sent out guidelines allowing economic operators to keep buying Russian oil and gas without breaching sanctions. As witnessed in 2015-2016, EUR parity can end up so near and yet so far, with EUR consolidating in a 1.05-1.15 range again.

AUD could consolidate between 0.69 and 0.71 after bottoming at 0.6830 on 12 May. On 18 May, consensus expects the wage price index to increase by 2.5% YoY in 1Q22 from 2.3% in 4Q21. More companies face pressure to offer higher wages to attract and retain staff. Although the IMF downgraded its 2022 world growth forecast to 3.6% in April from its 4.4% estimate in January, it upgraded Australia’s growth to 4.2% from 4.1% on higher commodity prices and the reopening of its economy. On 19 May, expect the unemployment rate to fall to 3.9% in April from 4% in March, with the Reserve Bank of Australia expecting the jobless rate to remain in the “low threes” into June 2024. With CPI inflation holding above the 2% to 3% target next year, RBA will want rates to normalize at 2.50%.

Quote of the day

“Everything popular is wrong.”

Oscar Wilde

17 May in history

Alaska became a US territory in 1884.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.