Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

DXY languished between 103 and 103.5 in the past two days after the sell-off from 105.6 on Friday. The market is reluctant to bet big on downside surprises in today’s US CPI. Consensus sees headline inflation turning negative at -0.1% MoM in December from 0.1% in November but worry about core inflation rising to 0.3% from 0.2%. Last Friday, the US unemployment rate returned to its record low of 3.5%. At last month’s FOMC meeting, Fed Chair Jerome Powell explained that the tight labour market remains challenging to bring down inflation in non-housing related core services, which accounts for 55% of the PCE core deflator.

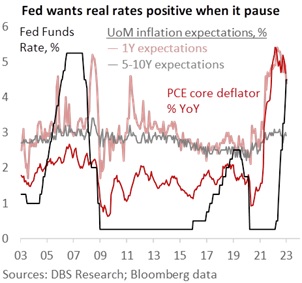

Although the market has priced in a smaller 25 bps hike at the FOMC meeting on 1 February, Fed officials kept the door open for a second 50 bps hike in case inflation surprised like the monthly jobs report. Three Fed Presidents – Patrick Harker (Philadelphia), James Bullard (St Louis), and Thomas Barkin (Richmond) – will speak after the CPI release today. They should stand by last month’s Summary of Economic Projections for the Fed Funds Rate to rise above 5% this year from 4.25-4.5% and push back the market’s bets for rate cuts later this year. Fed believes real rates need to turn positive and stay restrictive for longer to bring inflation down to its 2% target. Hence, pay attention to tomorrow’s University of Michigan’s inflation expectations data.

Beyond the US data, markets need to navigate the weaker global growth outlook this year. Next week, global recession fears will be high at the World Economic Forum in Davos, Switzerland, on 16-20 January. The IMF started the new year with a dire prediction that a third of the world economy would be in recession in 2023. The World Bank downgraded its 2023 global growth forecast to 1.7% from the 3% projected last June. The World Bank did not rule out a global recession on higher interest rates and escalating geopolitical tensions. Apart from persistent trade and tech tensions between the US and China, trading partners have accused the EU of protectionism over its carbon tax plan.

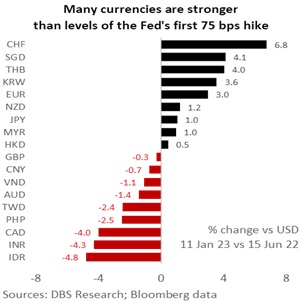

Like it or not, many currencies – CHF, THB, SGD, KRW, EUR, NZD, JPY, MYR, and HKD – are already stronger than levels seen at the Fed’s first 75 bps hike in June. Mindful that externally-dependant Asian currencies must pay attention to weaker exports, not just slowing inflation. Despite reopening hopes in China, CNY has retraced most of its August-November losses, with importers starting to pick up the greenback on the cheap. Considering laggards such as INR, PHP, and IDR might be viable.

Quote of the day

“Your desires and true beliefs have a way of playing blind man’s bluff. You must corner the inner facts.”

David Seabury

12 January in history

The first long-distance radio message was broadcast from the Eiffel Tower in Paris in 1908.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024