- Domestic drivers play a dominant part in Indonesia’s inflation outlook, according to our study

- Headline and core inflation have begun to drift up

- Rally in global oil prices raises the risk of an adjustment in subsidised fuel …

- ….to lower pressure on the fiscal books

- A partial pass through is likely

Related insights

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- Marriot International23 Apr 2024

A surge in global commodity prices, particularly crude oil, is a risk for regional inflation and fiscal trajectory. For Indonesia, rising commodities have been a mixed blessing, raising export earnings and government revenues (Indonesia: Resilient growth provides room to prioritise inflation), but adding to fiscal costs to maintain price controls as well as subsidies, besides stoking inflationary pressures.

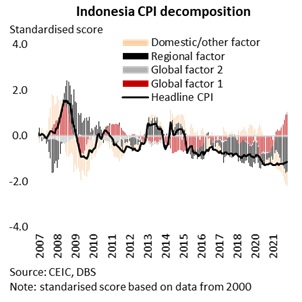

We carried out a Principal Component Analysis (PCA) to decipher the main drivers of headline consumer price inflation in ASEAN-5 (Indonesia, Malaysia, Philippines, Thailand, and Vietnam), which was outlined in ASEAN-5: Evaluating key inflation drivers. Fitting this model for Indonesia shows that whilst global factors (commodities) matter for inflation what matters more are domestic catalysts. Imported price inflation has picked up, but administrative measures and price controls have only allowed for partial pass through.

Fuel price adjustments in the offing?

After keeping retail fuel prices unchanged through the pandemic, indications are that prices of subsidized fuel might be raised to lower the burden on state finances.

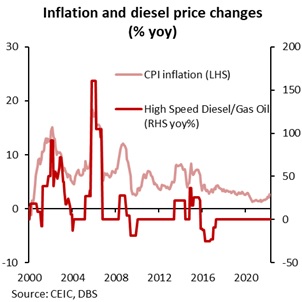

Price of the Indonesian crude basket has risen to an average of $99.4bl between Jan-Apr22, compared to $68.5bl in 2021, +45% on the year.

In the face of widening gulf between domestic and international prices, state-owned Pertamina adjusted prices of three non-subsidised, high-grade fuel variants - Pertamax Turbo, Dexlite and Pertamina Dex. Thereafter, price of unsubsidized Pertamax was raised by ~39% to IDR12500 from April, with these fuel types accounting for 16% of total consumption[1], and rest of the subsidized fuels. By contrast, commonly used subsidized variants Pertalite (90) and Premium (88) which account for over 80% of consumption, have been kept unchanged for the past three years.

Official hesitation to allow complete pass-through is understandable based on past experiences as price adjustments resulted in a sharp rise in fuel prices, pushing inflation up, weighing on bonds and necessitating swift tightening moves by the BI.

In 2001, the government hiked prices by 12% after an unsuccessful attempt the year before, followed by a 22% increase in 2003, part of which had to be rolled back following protests and violence against the move[2]. As subsidies continued to climb, retail prices were hiked sharply twice in 2005 (diesel up 27% in Mar and 105% in Oct), which drove inflation to six-year highs, notwithstanding cash support for low-income households. Notwithstanding a surge in global oil in 2007, domestic prices were held unchanged but yawning gap led the authorities to hike by nearly 29% in mid-2008.

The debate over the timing of price adjustments persisted in the next decade. A window to lower subsidies presented itself in 2014 when global oil prices were easing. Tapping that window, Indonesia raised its gasoline and diesel prices by nearly 40% in November 2014. In early-2015, the government announced plans to remove subsidies on gasoline and introduced flexibility in diesel, where in domestic prices would be allowed to fluctuate with a fixed gap of IDR1000 vs international prices.

The commonly used/ subsidized gasoline, gas, and diesel variants as well as electricity tariffs for low-income households have been kept unchanged in past 2-3 years. Based on the weights of these fuel variants, every 10% increase in gasoline and diesel is likely to add 0.4percentage points to inflation, with the cumulative impact to be magnified through other product categories. The aggregate energy index (fuel and transportation) carries 18.2% weight in the inflation basket. An increase in retail subsidized fuel to extend beyond first-order effects to feed into other components namely food (more than a quarter of the basket), logistics etc.

The government’s subsidy policy will be a key factor affecting inflation this year. There is a likelihood that subsidized prices are raised in Jun or 3Q22, with the scale of impact to hinge on the magnitude of increase. Our current forecast of 3.6% yoy doesn’t factor in any increase in subsidized fuel, with a 10% increase in petroleum, gasoline, and gas to raise our projection to 4.2-4.3% and that of 25%, close to 5.5%.

Fiscal revenues: boon and bane

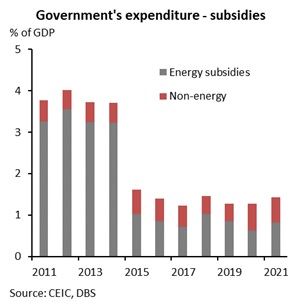

High energy prices have put pressure on Indonesia’s fiscal budget and books of state-owned electricity companies in the past, with fuel/ gas/ electricity subsidies amounting to a fifth of total government expenditure in 2013-2014. Besides ad-hoc price increases as discussed in the section above, the government had also set out to reform the subsidy policy.

In the past decade, subsidies were mostly directed at petroleum (RON88/Premium i.e., gasoline, kerosene, and diesel), 3kg LPG and electricity[3]. In January 2015, fuel in the central Indonesia zone was lifted, and fixed subsidy was set on diesel. Subsequently, gasoline and electricity prices for large businesses/ industrial as well as medium to high residential consumers was reformed to align with market prices. Relief was extended to lower income households by maintaining subsidies on commonly used fuel variants, e.g., RON88 and Premium, for instance. A regular price monitoring mechanism was also introduced. As a result, energy subsidy as a % of GDP fell from 3.2% of GDP in Dec 2014 to 0.8% average between 2017-2019.

Last year, realized total subsidy was 40% higher than budgeted and 24% above 2020 allocation. The 2022 Budget assumes a 15% drop in total subsidy to IDR207trn, of which energy including electricity is at IDR134trn vs IDR140trn last year. Add to this, state owned oil firm Pertamina also needs to be compensated for losses (sells below market prices). In contrast to a budgeted fall in subsidy, global oil prices have moved in the other direction. The 2022 State budget assumed the Indonesia Crude Price at $63bl and the current prevailing level is 45% higher at Jan-Apr22 average of $99.4bl.

In 1Q22, total subsidies are up 80% yoy, of which towards energy has risen by 55% yoy. Add to this is compensation due to PT Pertamina amounted to IDR49.5trn in 2020 of which IDR15.9trn is pending alongside IDR68.5trn for 2021[4], which might be much higher than the budgeted IDR140trn in 2022, according to industry watchers. Assuming a 20% increase in total subsidies alongside higher compensation towards the state-owned oil player, a cumulative headroom for 0.4% of GDP will be required of this year’s math to keep within the -4.85% target.

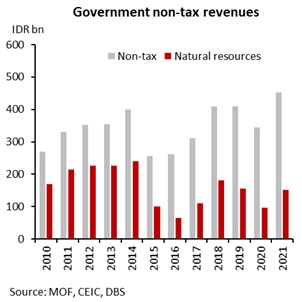

Encouragingly, the commodity price windfall also benefits the government by an increase in revenues from natural resources, which doubled in 1Q22 vs year back. These revenues made a third of non-tax revenues and 10% of total revenues. Of the key sub-segments, oil made up half, gas 25% and general mining 22% of the total earnings in 2020.

This might help to cover half of an increase in subsidy, beyond which two choices lie – either to adjust prices of subsidised fuel or reprioritise existing spending heads to create headroom for higher subsidy spending. The latter carries risks for growth, as the economy will require additional engines for recovery beyond the reopening boost, which will lose momentum in second half of the year. Our view is therefore that fuel prices might be partly adjusted in June/ 3Q22. Assuming partial adjustment in fuel prices, 2022 fiscal deficit is likely to narrow to -4.5% of GDP vs targeted -4.85%.

For monetary policy, a strong growth print provides the headroom to policymakers to monitor price stability risks and financial markets amongst tightening global conditions. Bank Indonesia had emphasized earlier that it will look through first order effects of adjustments in subsidized fuel, instead react to structural inflationary pressures. Core inflation is also a key gauge under watch, which accelerated to a two-high in April. The BI might resort to another reserve requirement rate hike, before shifting its guidance and raising the benchmark rate.

A hawkish shift in guidance is likely to June/July, which will be followed up by rate hikes. As core inflation strengthens further and domestic assets come under pressure from weak risk-uptake, even if partly mitigated by a strong trade account, we expect a cumulative 75bp of hikes is likely this year. This compares to expectations that the US Fed may raise rates by another 175bps by end-22, according to our house view, besides quantitative tightening of their balance sheet. Regional central banks have also begun to tighten monetary policy, including the recent unexpected move by BNM and RBI and back-to-back moves by Singapore’s MAS.

[1] Jakarta Post

[2] Reuters

[3] OECD

[4] CNBC

To read the full report, click here to Download the PDF.

Topic

Explore more

E & S FocusThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- Marriot International23 Apr 2024

Related insights

- Nanofilm Technologies International Ltd23 Apr 2024

- Digital Core REIT23 Apr 2024

- Marriot International23 Apr 2024