- A mix of high inflation and rising interest rates is likely to dampen US demand

- The war in Ukraine is casting a dark and long shadow on Europe

- China’s struggles with the pandemic look unlikely to abate soon

- In Asia, economic re-opening, resumption of tourism, and still-strong exports demand are pluses

- But high inflation and rates/FX/flows volatility are creating challenges

Related insights

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024

Commentary: Slowdown everywhere

Macro shocks are numerous these days; from energy and food price spike to China’s Covid struggles, and from concerns over the war in Ukraine to US Fed rate hikes, the global economy has a tough 2022 in progress.

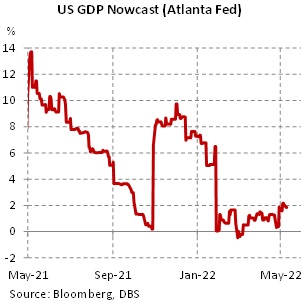

In the US, with the US Fed signalling sustained rate hikes, an economic slowdown is looming. Higher interest rates would hurt demand for autos and homes and refinancing, and they would also raise the cost of capital for fixed asset investment. Retails sales and housing data are strong presently, but we’re afraid that there is only downside from here onward. On fixed capital formation, Atlanta Fed’s Nowcast is already picking up a decline in domestic investment. We expect inflation to peak this quarter, but the level of prices will remain uncomfortably high through the course of this year, leading to a weakening of household and business sentiments. Our current forecast of 3% growth for the year has mounting downsides, unfortunately. In the absence of any visible positive catalysts, the risk around our forecast is asymmetrically weighed to the downside.

Meanwhile, in the Eurozone, fallout from the war in Ukraine and possible disruption in energy supply loom large. We note that there are offsets in the making, from a rise in public expenditure (on defence) and securing alternative sources of oil and gas (from the US and Qatar), but the outlook is grim, nonetheless. A prolonged period of security risks and sustained high inflation look likely, casting a heavy shadow on private consumption and investment. Our Euro area GDP growth forecasts of 2.2% likely has even greater downside risks than the US forecast.

Back here in Asia, China’s outlook, with its pandemic struggles, darkens by the day. Short of breakthrough with vaccines and anti-virals, we see few alternatives to the restrictions on movement currently in place. It is clear that the authorities see the public health risk way too great, given the relatively low levels of effective vaccinations, to just live with the virus. Hence the lockdowns will continue, dragging down employment and production. Our Nowcast model is tracking 3.9% real GDP growth in Q2, but the risk is that it could be much lower (perhaps down to 2%) if the lockdowns persist through June.

Our GDP Nowcasting models are presently tracking India at 3.3%, Indonesia at 4.8%, and Singapore at 4.3%. Economic re-opening, resumption of tourism, and still resilient export demand underpin our somewhat constructive prognosis. But inflation is clear and present in most places, and a slowdown in the West will readily translate into a weakening of exports demand. Add to this ongoing capital flow and currency market volatility, Asia has difficulties galore as well.

To read the full report, click here to Download the PDF.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024

Related insights

- Singapore Equity Picks18 Apr 2024

- Crypto Digest: Here comes Bitcoin “halving”18 Apr 2024

- Expedia Group Inc18 Apr 2024